Definition and Purpose of Form 8840

Form 8840, also known as the Closer Connection Exception Statement for Aliens, is a tax form used by non-U.S. residents. It serves the purpose of declaring a closer connection to a foreign country, which is crucial for establishing a nonresident status in the United States. This designation affects how an individual's tax obligations are assessed, providing an alternative to the substantial presence test.

Importance of Nonresident Status

- The substantial presence test determines if an individual qualifies as a resident based on the number of days spent in the U.S.

- By using Form 8840, individuals can claim connections to another country, influencing residency status and potentially reducing U.S. tax liabilities.

Steps to Obtain the 2011 Form 8840

Retrieving the 2011 version of Form 8840 involves straightforward steps:

- Visit the IRS Website: The IRS provides downloadable forms and instructions, including historical versions.

- Request Through Mail: You can request a physical copy by calling the IRS directly.

- Utilize Tax Preparation Software: Some platforms may offer archived forms and allow electronic completion and submission.

- Professional Tax Services: Engaging a tax professional can provide access to historical forms and advice on their correct usage.

Completing the Form 8840: Key Steps

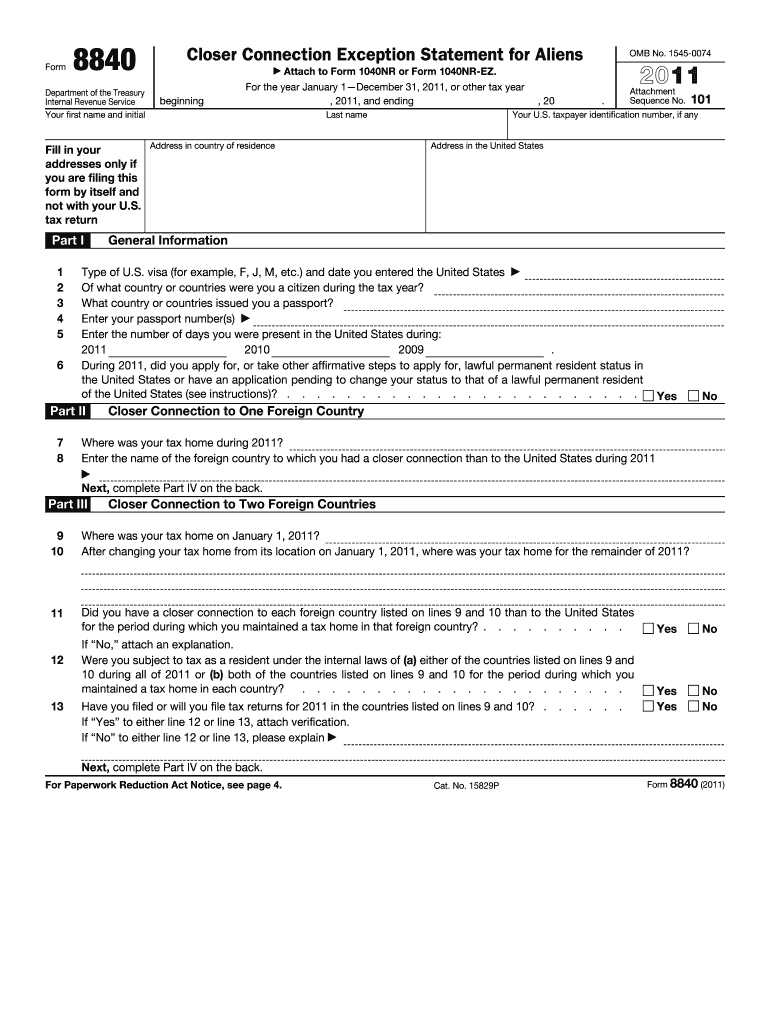

Section I: Personal Details

- Enter personal identification information such as name, taxpayer identification number (TIN), and address.

Section II: Substantial Presence Test

- Record the days present in the U.S. for the current and prior two years to evaluate if you meet the substantial presence test.

Section III: Closer Connection Information

- Answer questions detailing ties to a foreign country, such as government ties, family, and economic interests.

Detailed Documentation

- Attach any necessary documents that substantiate claims of stronger ties to a foreign country than the U.S.

Who Uses the 2011 Form 8840

Typical Users

Non-U.S. residents spending significant time in the U.S. who do not wish to be taxed as residents primarily use this form. This includes:

- International students attending U.S. institutions.

- Seasonal workers or tourists who have spent considerable time in the U.S.

- Retirees or self-employed individuals who split residence between the U.S. and another country.

IRS Guidelines on Form 8840

Clarity and Completeness

- Ensure all sections are filled out accurately and thoroughly to avoid processing delays.

- Follow the specific instructions accompanying the form, available on the IRS website.

Record Maintenance

- Keep a copy of the completed form and any supporting documentation for three years, as the IRS may request verification.

Filing Deadlines and Important Dates

- Typically, Form 8840 should be filed by June 15 of the following year if you qualify as a nonresident alien.

- Late filing could result in the inability to claim nonresident status, so timely submission is critical.

Penalties for Non-Compliance

Failing to submit Form 8840 when mandated can have significant repercussions, including:

- Potential reclassification as a U.S. resident for tax purposes, leading to additional tax liabilities.

- Retroactive penalties and interest on taxes that should have been declared as a resident tax obligation.

Digital Versus Paper Versions

Advantages of Digital Submission

- Immediate confirmation of receipt by the IRS.

- Reduced risk of postal delays or document misplacement.

- Easier archiving and retrieval for personal records.

Paper Submission Considerations

- Preferable for individuals lacking reliable internet access.

- Must be postmarked by the filing deadline to avoid penalties.

Examples of Using Form 8840

Scenario: International Consultant

An international consultant who temporarily resides in the U.S. for work projects can utilize Form 8840 to assert their closer connection to their home country, thereby benefiting from a favorable tax situation due to nonresident status.

Scenario: Visiting Academic

An academic on a temporary exchange program might spend several months at a U.S. institution annually. Form 8840 will help maintain their nonresident status, aligning with their intention not to transition into a U.S. taxpayer.

Each section of Form 8840 contributes to ensuring a fair and accurate assessment of an individual's tax obligations relative to their U.S. presence, serving both the taxpayer's interest and IRS compliance norms.