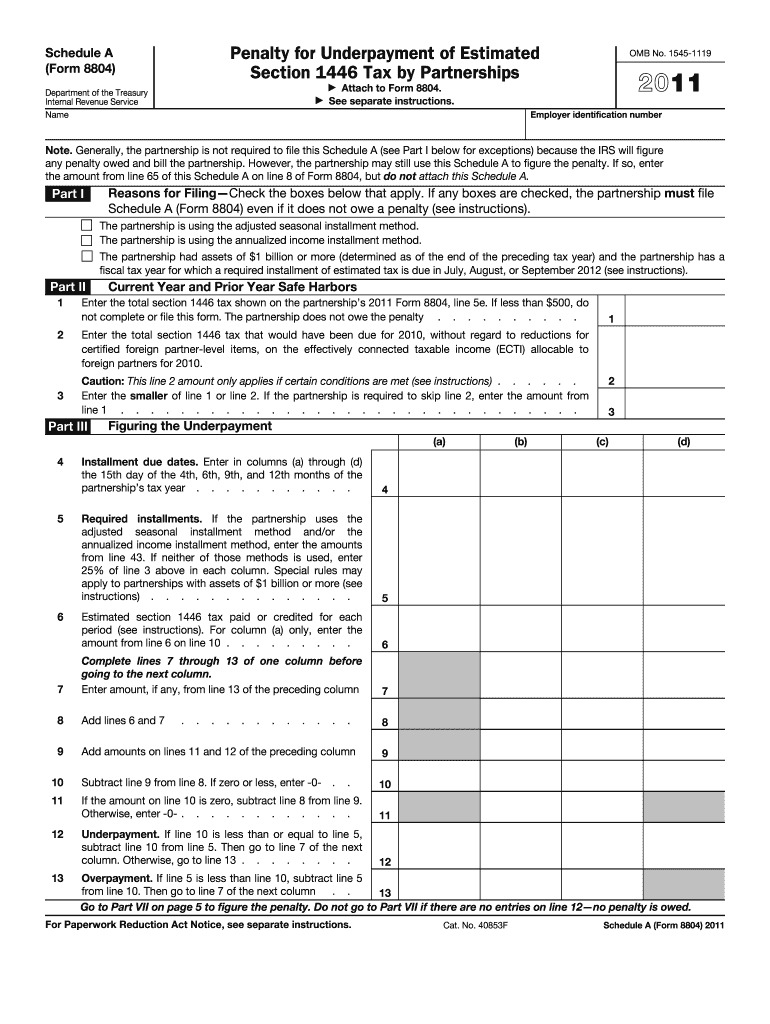

Understanding the 2011 Form 8804

The 2011 Form 8804 is a tax form used to report and calculate penalties for the underpayment of estimated Section 1446 tax by partnerships. This form is crucial for ensuring compliance with U.S. tax regulations. It serves as a schedule associated with the primary Form 1065, dedicated to partnership tax returns. The 2011 Form 8804 specifically addresses 2011 tax year obligations, making it essential for partnerships involved in withholding taxes for foreign partners.

Key elements of the form include the calculation of estimated tax payments, penalties for any underpayments, and the methods partnerships must use to meet tax payment obligations. By outlining these specifics, the form ensures that partnerships comply with federal tax requirements.

Steps to Complete the 2011 Form 8804

Completing the 2011 Form 8804 involves several steps. Partnerships need to gather relevant financial information from the fiscal year 2011. This includes total income, allowable deductions, and the specific amounts subject to Section 1446 tax withholding. Here is a general guideline for filling out this form:

- Gather Financial Information: Start by collecting all pertinent financial data for 2011, including gross income and deductions.

- Calculate Withholding Tax: Determine the amounts subjected to the Section 1446 withholding tax.

- Estimate Tax Payments: Use the estimated tax payment methods outlined on the form.

- Complete the Penalty Calculation: Enter information in sections related to underpayment calculations and penalties.

- Review the Form: Double-check all entries for accuracy before submission.

Legal Use of the 2011 Form 8804

The 2011 Form 8804 is used by partnerships for legal compliance with IRS tax obligations concerning foreign partners. Underpayment of this tax exposes partnerships to penalties and interest. Therefore, it is essential for partnerships to quarterly estimate their tax liabilities accurately.

It is also important to note the penalties for non-compliance. These can include fines or other sanctions imposed by the IRS. As a legal document, the form holds significance in demonstrating compliance with federal tax laws.

Who Typically Uses the 2011 Form 8804

This form is primarily used by partnerships that have foreign partners subject to U.S tax withholding under Section 1446. Such partnerships range from limited liability partnerships (LLPs) to general partnerships involved in various industries.

Partnerships with the following characteristics typically file the Form 8804:

- Foreign Income Sources: Significant portions of income from international operations or investments.

- Foreign Partners: At least one foreign partner necessitating withholding tax.

- Investment Partnerships: Those dealing with global investments requiring specific tax treatments.

Important Terms Related to the Form

To effectively use the 2011 Form 8804, understanding key terms is necessary:

- Section 1446 Tax: A withholding tax specific to income allocated to foreign partners.

- Estimated Tax Underpayment Penalty: A penalty incurred when estimated tax payments fall short of the actual tax liability.

- Safe Harbor Provisions: Rules that allow partnerships to avoid penalties under specific pre-set conditions.

These terms provide context, ensuring partnerships meet their regulatory obligations thoroughly.

Key Elements of the Form 8804

Focusing on the specific sections of the form, some of the key elements include:

- Income Allocations: Calculating income allocable to foreign partners.

- Penalty Workouts: Reviewing total penalties calculated for underpayments.

- Safe Harbor and Installments: Options provided to reduce penalties if certain conditions are met.

Each section of the form is intended to detail the partnership's financial activities relevant to the withholding tax, allowing for accurate tax calculations and payment.

IRS Guidelines

The IRS provides comprehensive guidelines for completing the Form 8804. These guidelines highlight the calculation methods, safe harbor provisions, and deadline compliance necessary to avoid penalties. It is critical for partnerships to study and apply these guidelines since misinterpretation may result in financial penalties or additional scrutiny from the IRS.

IRS guidelines also include detailed instructions on filling out each form section and provide examples illustrating common calculation scenarios.

Filing Deadlines and Important Dates

Partnerships must adhere to the IRS deadlines for filing the Form 8804 to avoid penalties. Generally, the form should be filed with the IRS along with the partnership's annual tax return. Key deadline details include:

- Quarterly Estimated Payments: Due four times a year, typically April 15, June 15, September 15, and January 15 of the following year.

- Annual Submission: Generally due on March 15 for calendar-year partnerships, unless extended.

Understanding these deadlines ensures timely compliance and avoids unnecessary penalties.

Software Compatibility and Submission Methods

In the modern digital age, partnerships may prefer digital submissions via compatible tax software programs such as TurboTax or QuickBooks. These platforms provide data import options, simplifying the task of filling out tax forms. They also generally ensure automatic updates with the latest tax regulations, minimizing risks of human errors in calculations.

When submitting the form, partnerships have multiple options:

- Online Submission: Via IRS e-file system through approved providers.

- Mail-In Option: Physical submission following IRS mailing instructions.

- In-Person Delivery: Direct handover at designated IRS locations, though less common.

Each method offers flexibility, enabling partnerships to choose the most convenient submission path.