Definition and Meaning

Form 1041-QFT, also known as the U.S. Income Tax Return for Qualified Funeral Trusts, is a tax form used by trustees to report income, deductions, gains, losses, and tax liabilities of qualified funeral trusts (QFTs) for the year 2011. A Qualified Funeral Trust is a specialized trust designed to manage funds set aside for covering the funeral expenses of an individual. This form helps ensure that the income generated by the trust is properly reported and taxed.

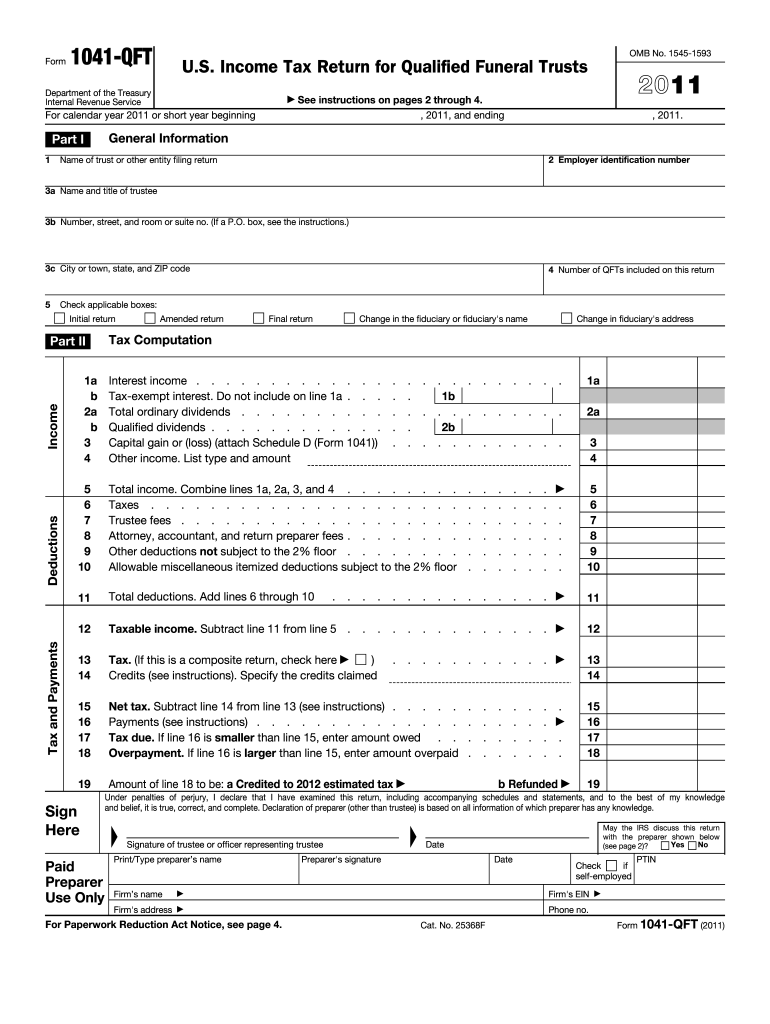

How to Use Form 1041-QFT for 2011

The primary use of Form 1041-QFT is to capture and report the financial activities of a qualified funeral trust throughout the tax year. Trustees must detail all income, deductions, gains, and losses pertaining to the trust. This information helps compute the overall tax liabilities of the QFT, ensuring compliance with IRS regulations. Besides financial reporting, using this form involves making specific elections for the trust to maintain its QFT status.

Steps to Complete the Form 1041-QFT for 2011

- Gather Required Documents: Before starting, collect all necessary financial statements, receipts, and prior year tax returns.

- Enter Trust Information: Begin by filling in the trust's name, address, and identifying numbers.

- Report Income: Include all sources of income earned by the trust during the tax year. This can include interest, dividends, and other relevant income.

- Calculate Deductions: Identify and deduct expenses related to the trust, such as trustee fees or legal expenses.

- Determine Tax Liability: Use the income and deductions to compute the net tax liability for the trust.

- Sign and Date: Trustees must sign and date the form, confirming the accuracy of the information provided.

- Submit the Form: File the completed form with the IRS either electronically or by mail, according to the instructions.

Who Typically Uses Form 1041-QFT for 2011

The form is predominantly used by trustees who manage qualified funeral trusts. These trusts are usually set up by funeral homes or cemeteries to manage pre-paid funeral arrangement funds. Trustees are responsible for ensuring these funds are utilized in compliance with legal guidelines. These entities are required to use Form 1041-QFT to report their financial activities transparently to the IRS.

IRS Guidelines for Form 1041-QFT

The IRS mandates that all income generated from the funeral trust be reported using Form 1041-QFT. Accurate reporting is critical to avoid any discrepancies or penalties. Trustees must adhere to the IRS regulations concerning deductible expenses and income reporting. The IRS offers detailed instructions for the form to guide trustees through the process of accurate and complete filings.

Filing Deadlines and Important Dates

For the tax year 2011, Form 1041-QFT should be filed by April 15, 2012. If that date falls on a weekend or holiday, the deadline is extended to the next business day. Trustees can file for an extension using Form 7004 if they require more time. It is crucial to meet these deadlines to avoid late filing penalties.

Required Documents for Form 1041-QFT

Trustees should have access to comprehensive financial records related to the funeral trust, including:

- Income statements

- Documentation of deductions or expenses

- Prior tax returns for comparative analysis

- Updated trust documentation or any amendments made during the tax year

Penalties for Non-Compliance

Failing to file Form 1041-QFT or withholding accurate information can result in penalties imposed by the IRS. Trustees may face financial penalties for late filing unless an approved extension is noted. Additionally, inaccuracies or fraudulent information may lead to further legal consequences. It is essential to ensure that all details are precise and submitted on time to avoid potential penalties.