Definition & Meaning

The 2008 Form 990 is an Internal Revenue Service (IRS) form used primarily by tax-exempt organizations, non-exempt charitable trusts, and section 527 political organizations to report information about their financial activities. It is a vital document that serves dual purposes: ensuring these organizations comply with federal tax laws and maintaining transparency about their operations. The form enables the IRS to evaluate an organization's activities and finances to safeguard the tax-exempt status.

Key Purposes

- Compliance Monitoring: Ensures adherence to IRS regulations.

- Transparency: Provides detailed public records of financial standings and operations.

- Operational Review: Assesses management and governance practices.

Steps to Complete the 2008 Form 990

Completing the 2008 Form 990 involves several steps, each requiring careful attention to detail.

-

Gather Necessary Information:

- Financial statements, including income, expenditure, and balance sheets.

- Details of major donors and fundraising events.

-

Fill Out Organizational Details:

- Include organization name, EIN, and address.

- Provide information on any changes to the governing documents.

-

Report Financial Information:

- Detail revenue categories such as contributions, grants, and program service revenue.

- Explain functional expenses: program service, management, and fundraising costs.

-

Outline Program Service Accomplishments:

- Describe significant accomplishments and how funds are utilized.

-

Provide Schedule Information:

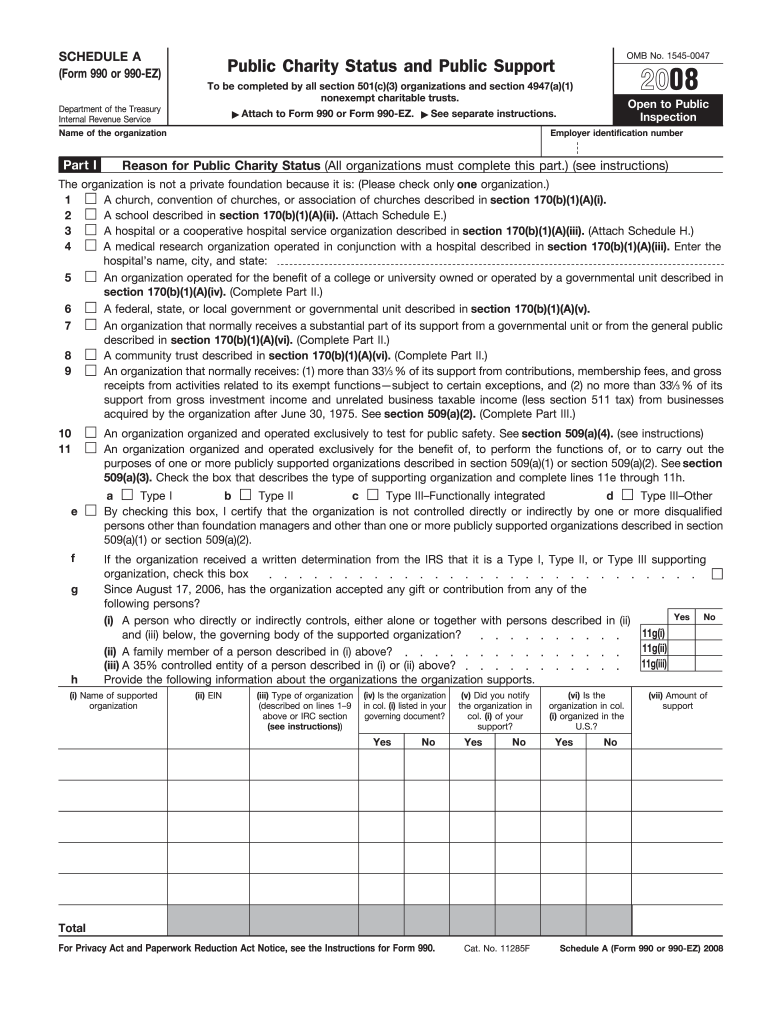

- Complete additional schedules as applicable (e.g., Schedule A for public charity status).

Tips for Accuracy

- Double-check all calculations.

- Be consistent in reporting figures across corresponding sections.

How to Obtain the 2008 Form 990

Obtaining the 2008 Form 990 is straightforward, with several accessible options for organizations.

- IRS Website: The form can be downloaded directly in PDF format from the IRS website.

- Mail Request: Organizations can request a physical copy by contacting the IRS.

Considerations

- Ensure the form version matches the corresponding tax year.

- Verify form availability for compatibility with digital tax preparation software.

Who Typically Uses the 2008 Form 990

The users of the 2008 Form 990 include a wide scope of tax-exempt entities. It caters to the specific reporting requirements of each organization type.

- Nonprofit Organizations: These may include educational institutions, charities, and cultural organizations.

- Section 501(c)(3) Entities: Organizations engaging in charitable, religious, or educational activities.

- Political Organizations: Groups organized under section 527 primarily for influencing elections.

Typical Filing Entities

- Museums

- Community foundations

- Health organizations

IRS Guidelines

The IRS provides detailed guidelines on how to correctly complete and file Form 990.

- Filing Instructions: The IRS instructions are comprehensive, covering each part of the form in detail.

- Amendments: Guidelines for amending previous submissions to correct errors.

Key Points

- Adherence to IRS guidelines is essential to avoid penalties.

- Verify all the latest updates on reporting and filing requirements from the IRS.

Penalties for Non-Compliance

Non-compliance with the filing requirements of the 2008 Form 990 can result in significant penalties.

- Daily Penalties: The IRS imposes monetary fines for late or incomplete submissions, depending on the organization's size.

- Loss of Tax-Exempt Status: Persistent failure to file Form 990 can lead to revocation of tax-exempt status.

Preventive Measures

- Implement a diligent filing calendar.

- Assign a responsible officer to oversee the timely submission.

Important Terms Related to 2008 Form 990

Understanding the specialized vocabulary associated with the Form 990 is crucial for accurate completion.

- EIN (Employer Identification Number): A unique identifier for tax purposes.

- Exempt Purpose: The mission and activities qualifying an organization for tax-exempt status.

- Fiscal Year: The 12-month period used for accounting purposes.

Clarifications

- These terms are defined in IRS publications for detailed reference.

- Ensures accurate and compliant form preparation.

Versions or Alternatives to the 2008 Form 990

Besides the standard Form 990, there are simplified versions tailored for smaller organizations.

- Form 990-EZ: A shorter version for organizations with gross receipts less than $200,000 and total assets under $500,000.

- Form 990-N (e-Postcard): For very small organizations with gross receipts under $50,000.

Strategic Use

- Choosing the correct form version can simplify reporting and reduce preparation time.

- Understand thresholds and eligibility to take advantage of simpler forms.