Definition & Meaning

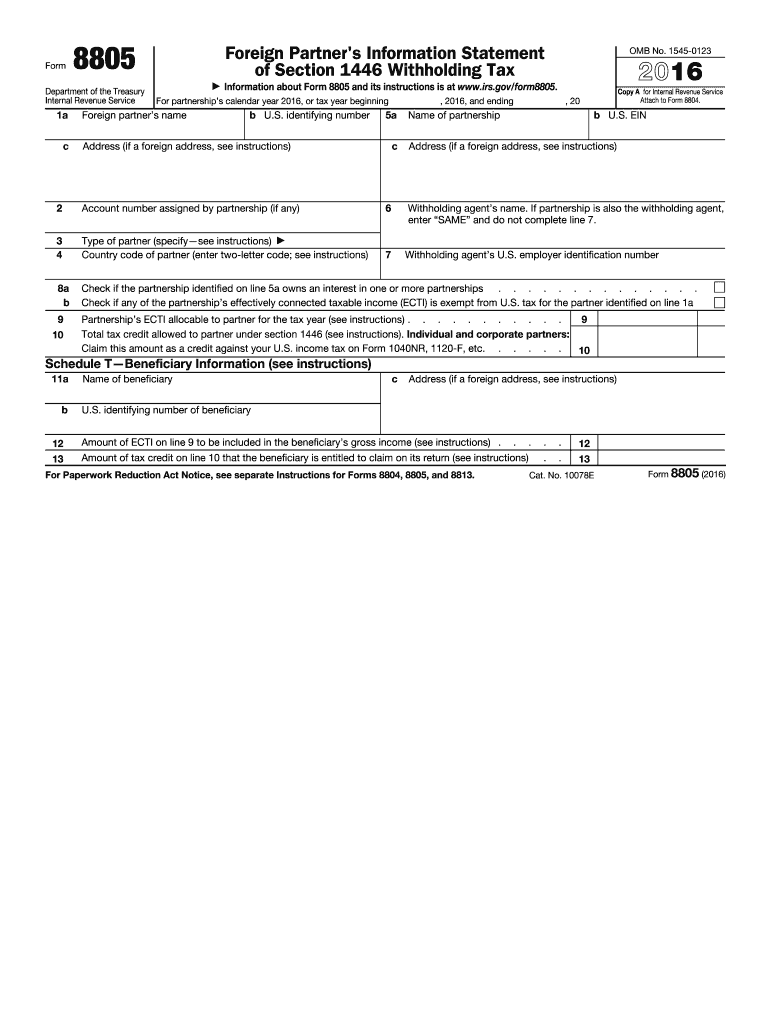

Form 8805 is a document issued by the IRS to report Section 1446 withholding tax details for foreign partners in a partnership during the 2016 tax year. This form highlights crucial particulars, including the foreign partner’s name, the U.S. identifying number, the partnership's effectively connected taxable income (ECTI), and applicable tax credits under section 1446. Its primary role is to facilitate compliance with U.S. tax obligations by detailing the withholding tax collected from foreign partners’ ECTI distributions.

Key Elements of the 2016 Form 8805

The 2016 Form 8805 consists of several critical sections designed to capture detailed information. These sections encompass:

- Foreign Partner Information: Includes the foreign partner’s name, address, and U.S. identifying number.

- Partnership Details: Specifies the partnership’s name, address, and employer identification number (EIN).

- Effectively Connected Taxable Income (ECTI): Outlines the total amount distributed to the foreign partner that is subject to withholding.

- Tax Calculations: Details the amount of tax withheld, framed within the context of the allowable tax credits.

- Copies and Distribution: Copy A is for the IRS, Copy B for the foreign partner’s records, Copy C is attached to the partner’s federal tax return, and Copy D stays with the withholding agent.

Steps to Complete the 2016 Form 8805

Completing Form 8805 involves several essential steps:

- Gather Information: Collect necessary details about the foreign partner and the partnership, including identification numbers and addresses.

- Calculate ECTI: Determine the partnership's effectively connected taxable income to be declared for the partner.

- Compute Tax Withholding: Calculate the withholding tax based on the ECTI and any applicable tax credits.

- Fill Out Form: Enter all relevant data in the specified fields, ensuring accuracy for both identification and financial figures.

- Distribute Copies: Ensure that all copies (A, B, C, D) are completed and distributed to their respective recipients, as outlined.

Who Typically Uses the 2016 Form 8805

Form 8805 is mainly utilized by partnerships with foreign partners subject to U.S. tax withholding. This includes:

- Domestic Partnerships: With foreign individual or corporate partners.

- Foreign Partnerships: Engaging in U.S. trade or business activities.

- Withholding Agents: Responsible for withholding tax on behalf of foreign partners. Partnerships are required to issue these forms to provide accurate records for both the IRS and the foreign partners.

Legal Use of the 2016 Form 8805

The legal obligation to use Form 8805 arises from the need to report and remit withholding taxes on ECTI distributed to foreign partners. It is mandated under Section 1446 of the Internal Revenue Code. The form ensures partnerships comply with tax laws, preventing legal penalties and fines for underreporting or failing to withhold the correct tax amounts.

IRS Guidelines

The IRS provides comprehensive guidelines for filling Form 8805. These instructions cover:

- Proper Identification: Ensuring IRS and taxpayer numbers are correct.

- Accurate Calculations: Details on how to determine ECTI and the associated tax withholdings.

- Form Distribution: Guidelines for maintaining records and ensuring all parties receive their respective copies. The IRS emphasizes accuracy in these submissions to prevent audit flags or compliance issues.

Filing Deadlines / Important Dates

Form 8805 must be filed with the IRS by the fifteenth day of the third month after the partnership tax year ends. Partnerships need to:

- Prepare early to meet deadlines.

- Ensure timely filing to avoid penalties. For 2016, partnerships aiming to avoid late payments would ensure submissions by the required dates, considering any applicable extensions.

Penalties for Non-Compliance

Failing to file Form 8805 correctly or on time can lead to financial penalties. Consequences may include:

- Monetary Penalties: Vary based on lateness and the intention behind non-compliance.

- Interest Accrual: On late payments related to withheld taxes. Ensuring accurate and timely filings helps partnerships avoid these disruptive financial impacts.

Examples of Using the 2016 Form 8805

Practical scenarios demonstrate Form 8805’s application:

- International Real Estate Partnerships: With foreign investors receiving rental income.

- Cross-Border Tech Startups: Distributing profit shares to non-U.S. partners, ensuring compliance with withholding obligations.

These cases illustrate the form’s role in ensuring transparency and accurate withholding tax compliance under U.S. law.