Definition & Meaning

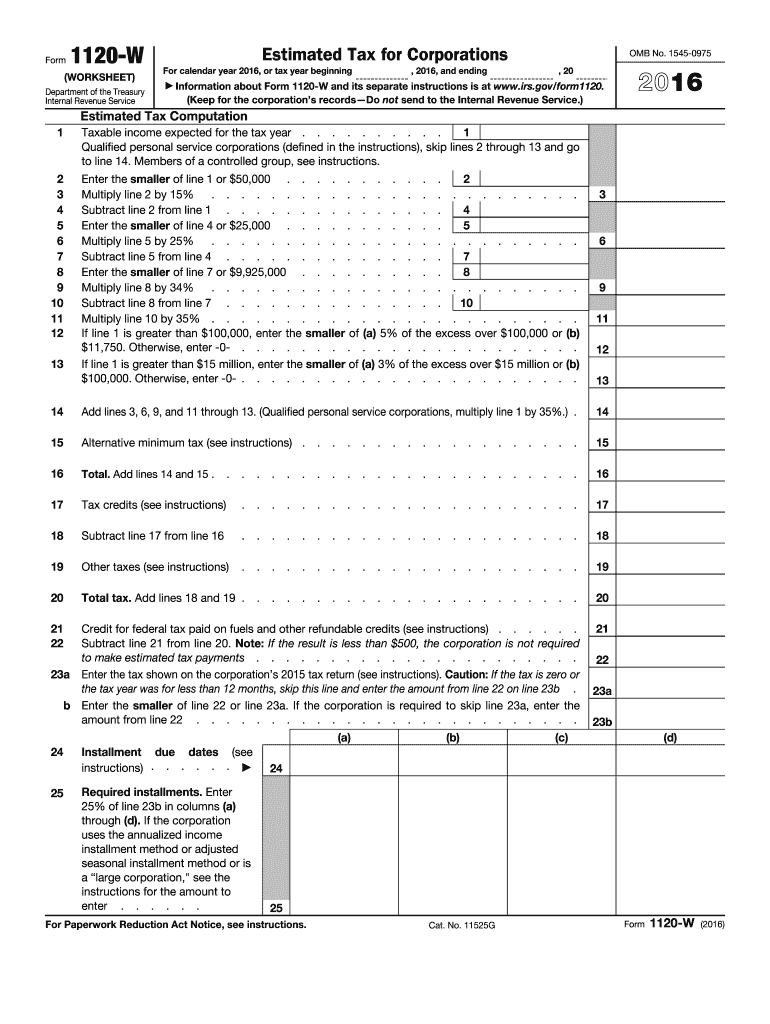

Form 1120-W is the Worksheet for the Internal Revenue Service that corporations in the United States use to calculate their estimated tax payments for the 2016 tax year. This form is essential for determining the estimated income tax a corporation owes, helping avoid underpayment penalties. It focuses on computing taxable income, understanding required installments, and addressing income variations throughout the year. The 1120-W includes specific sections for determining alternative minimum tax, which may be applicable to some corporate entities.

Steps to Complete the Form 1120-W 2016

To accurately complete form 1120-W for 2016, follow these steps:

- Gather financial documents: Collect all necessary financial records, including income statements, expense reports, and previous tax returns.

- Calculate expected taxable income: Use projected revenue and expense figures to estimate the corporation’s taxable income for the year.

- Compute estimated tax: Apply the corporate tax rate to the estimated taxable income to find the preliminary tax liability.

- Adjust for credits and other taxes: Include any applicable tax credits, such as foreign tax credit, and consider any additional taxes like the alternative minimum tax.

- Determine required installments: Divide the total estimated tax liability by four to ascertain the quarterly estimated tax payments.

- Review and finalize: Ensure all calculations align with IRS guidelines and adjust if necessary before finalizing.

How to Obtain the Form 1120-W 2016

Corporations can obtain form 1120-W for the 2016 tax year through several methods:

- IRS website: Access and download the form from the official IRS website. This is the most reliable and up-to-date source.

- Tax software: Many tax preparation software packages include forms like the 1120-W, which can be filled out digitally.

- Tax professionals: Certified accountants or tax preparers often provide the necessary forms and assistance in their completion.

Important Terms Related to Form 1120-W 2016

Understanding key terms is critical for accurately using form 1120-W:

- Taxable Income: The total income of a corporation subject to taxes after deductions and exemptions.

- Alternative Minimum Tax (AMT): A parallel tax system ensuring corporations with substantial income pay a minimum tax amount.

- Estimated Tax: The expected tax liability for a corporation, divided into quarterly payments to avoid penalties.

- Installments: Scheduled payments made throughout the fiscal year to cover anticipated tax obligations.

Key Elements of the Form 1120-W 2016

Form 1120-W encompasses several critical elements:

- Tax computation sections: Detailed lines that require inputs for taxable income, deductions, and credits.

- Installment calculations: Areas to determine quarterly payments, which are vital in managing cash flow and compliance.

- Instructions for filing: Clear guidelines on completing and maintaining records, ensuring corporations meet IRS requirements effectively.

IRS Guidelines for Completing Form 1120-W 2016

Adhering to IRS guidelines is crucial when utilizing form 1120-W:

- Keep accurate records: Corporations must maintain detailed financial documentation to substantiate calculations.

- Adhere to filing deadlines: Estimated tax payments are typically due in April, June, September, and January.

- Use correct figures: Employ accurate and up-to-date income projections to avoid underestimating tax liability and incurring penalties.

Filing Deadlines / Important Dates

Corporations should note the following deadlines for estimated tax payments:

- First installment: Due by April 15, 2016

- Second installment: Due by June 15, 2016

- Third installment: Due by September 15, 2016

- Fourth installment: Due by January 15, 2017

Timely payments help avoid interest and penalties.

Penalties for Non-Compliance

Failure to comply with IRS requirements regarding form 1120-W can result in penalties:

- Underpayment penalty: Imposed if quarterly estimated taxes are less than expected, typically a percentage of the underpaid amount.

- Late payment penalty: Applied to corporations that miss filing deadlines, accruing additional costs over time.

- Inaccurate reporting penalty: Levied for significant discrepancies between estimated and actual tax obligations, emphasizing the importance of precise calculations.

Business Entity Types That Benefit Most from Form 1120-W 2016

Corporations of varying structures benefit from utilizing form 1120-W:

- C Corporations: Large entities often with higher tax liabilities utilize this form to manage substantial tax obligations.

- S Corporations: Although S Corporations generally file different forms, those anticipating specific tax events might still reference the 1120-W.

- Multinational Corporations: Companies with international income that might be subject to foreign tax credits can use this worksheet to optimize tax strategies.