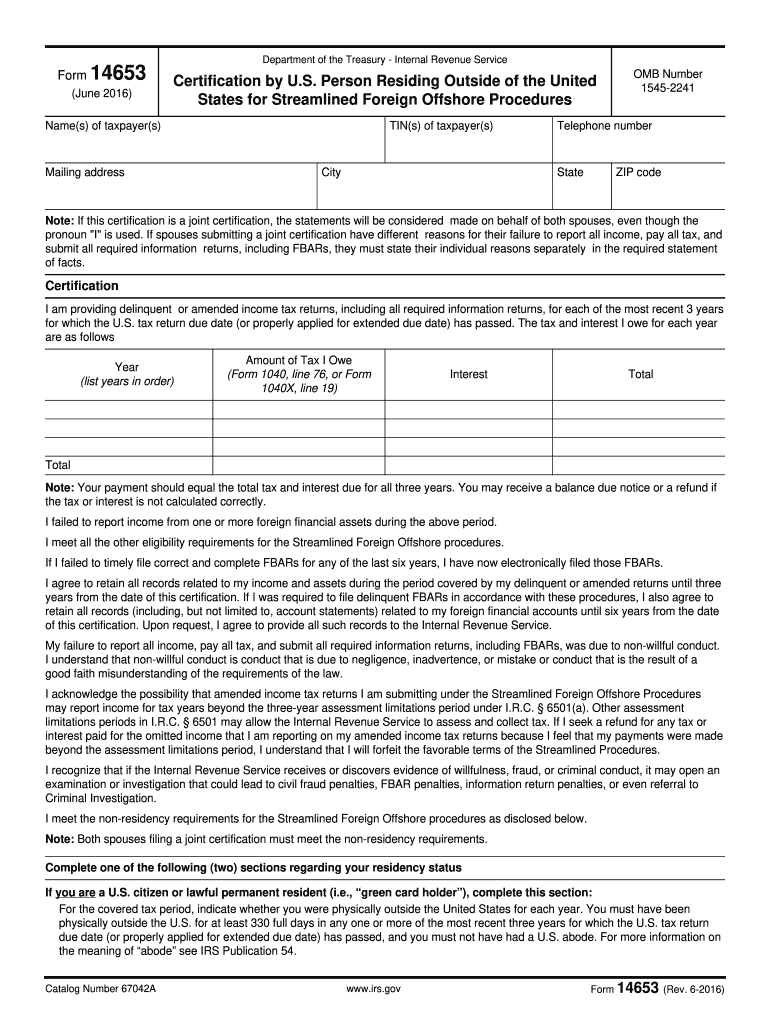

##Definition and Meaning of Form 14

Form 14653, issued by the IRS, is designed for U.S. persons residing outside the United States who wish to participate in the Streamlined Foreign Offshore Procedures. This form is pivotal for taxpayers needing to report delinquent or amended income tax returns due to non-willful conduct. It is essential for providing the IRS with detailed explanations of why income wasn’t reported and why information returns were not submitted on time. The form collects comprehensive personal and financial information specific to foreign financial accounts and assets.

##How to Use Form 14

Form 14653 provides a structured approach for taxpayers to explain their non-compliance with reporting requirements without facing severe penalties. The form requires detailed justifications and supporting documentation to confirm the non-willful nature of discrepancies. Using this form correctly involves assembling relevant records, including financial account statements, and completing all sections thoroughly to ensure compliance with IRS expectations.

- Identify Non-Willful Conduct: Clearly state the reasons for non-compliance and emphasize the lack of willful intent.

- Gather Supporting Documents: Include documents that verify financial accounts and any missed reporting obligations.

- Complete Required Sections: Ensure detailed, truthful entries in each section, as omissions can affect eligibility.

##Steps to Complete Form 14

Completing Form 14653 involves a series of specific steps aimed at providing clarity and full transparency to the IRS.

- Section by Section Completion:

- Provide personal information accurately, including social security number and address.

- Detail foreign financial accounts and provide explanations for non-compliance.

- Documentation and Evidence:

- Attach statements or records supporting your financial reporting history.

- Review and Proofread: Double-check all entries for accuracy and completeness before submission.

##Eligibility Criteria for Form 14

Eligibility for using Form 14653 hinges on specific criteria outlined for U.S. persons living outside the United States:

- Non-Willful Conduct: The primary criterion is that the taxpayer's failure to comply was due to non-willful conduct.

- Foreign Residency: The form is only applicable to U.S. persons residing outside the United States.

- Previous Filings: Account for prior tax return filings and submit any amendments necessary alongside the form.

##Required Documents for Form 14

Submitting Form 14653 requires several supporting documents:

- Previous Tax Returns: Provide copies of the last three years of filed tax returns with necessary amendments.

- Financial Account Statements: Include detailed statements for all foreign financial accounts held during the reporting period.

- Explanations and Justifications: Written documentation explaining why certain incomes or accounts were not previously reported.

##IRS Guidelines for Form 14

The IRS provides explicit guidelines for completing Form 14653:

- Adherence to Detailed Instructions: Follow IRS instructions carefully to minimize errors.

- Non-Willful Certification: Sign under penalties of perjury, affirming the non-willful nature of non-compliance.

- Maintain Transparency: The IRS mandates complete transparency and truthfulness in disclosures.

##Examples of Using Form 14

Examples provide practical insights into how different taxpayers might use Form 14653:

- Self-Employed Abroad: A freelancer based in Europe neglected to report certain offshore accounts. Form 14653 allows them to disclose this oversight and settle issues non-penally.

- Retired Abroad: A retired individual living in a foreign country realizes past tax filings omitted some foreign pension accounts, leading them to utilize Form 14653 to amend records.

##Penalties for Non-Compliance with Form 14653

Failing to comply with Form 14653 filing requirements can have severe consequences:

- Penalties for Inaccuracy: Not adhering strictly to the form's requirements or providing false information can lead to penalties.

- Neglecting to File: Failure to submit identified documentation may result in involvement in more significant penalties for tax misconduct.