Definition and Purpose of the Verification of Mortgage Form

The verification of mortgage form serves as an essential document used primarily by lenders, landlords, and other creditors to confirm an applicant's mortgage status. It provides a comprehensive overview of an individual's mortgage history, allowing prospective lenders to assess the applicant’s creditworthiness effectively. The form typically includes fields designated for both the lender and the creditor to fill in relevant details regarding the mortgage account, payment record, and outstanding balance.

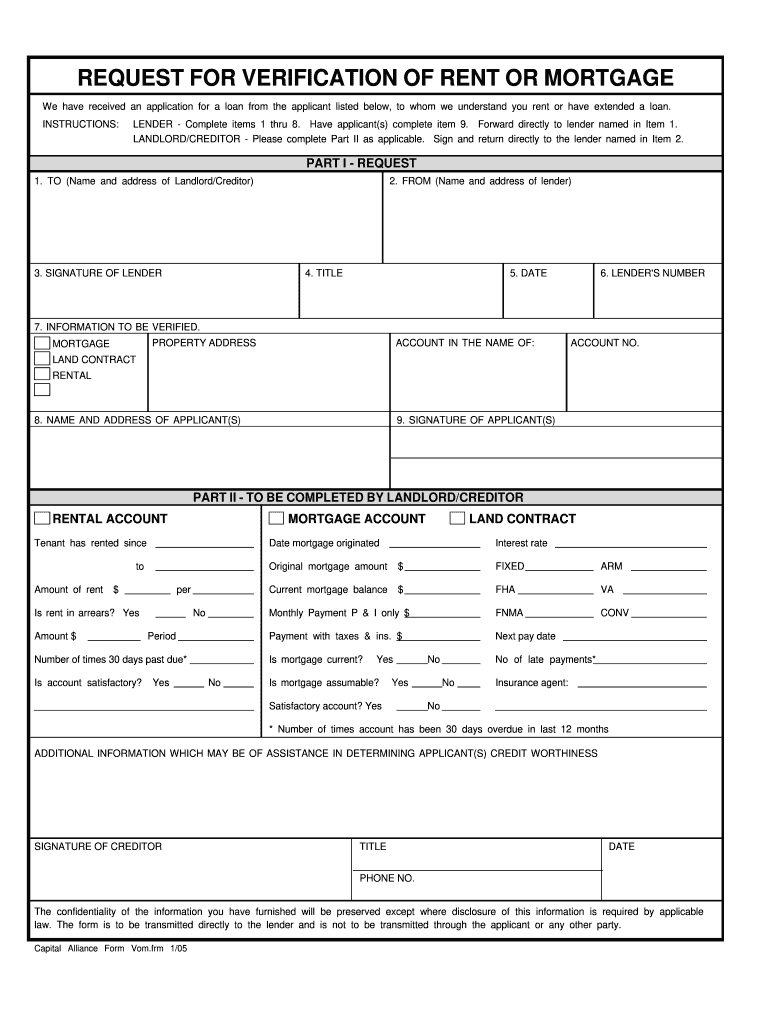

Key Components of the Form

- Personal Information: This section collects essential details about the mortgage holder, including name, address, and loan account number.

- Mortgage Account Details: Lenders must specify the type of mortgage, including the start date, loan amount, and payment history.

- Payment History: The form may require a detailed account of the borrower’s payment behavior, indicating any late payments or defaults.

- Confidentiality Notice: Ensures that all shared information remains private and encourages direct communication between the lender and creditor.

This form is not only crucial for lenders assessing risk but also for tenants seeking rental properties who may need to demonstrate financial stability to landlords.

How to Use the Verification of Mortgage Form

Utilizing the verification of mortgage form involves several key steps to ensure accuracy and compliance. Applicants must first complete their section before submitting it to their mortgage lender for verification.

Steps to Effectively Use the Form

- Obtain the Form: Request the verification of mortgage template from your lender or download it from a reputable site that offers free resources.

- Complete Personal Information: Fill in your name, current address, and any required identification numbers.

- Specify Loan Details: Accurately describe your mortgage account, including the original loan amount, current outstanding balance, and lender contact details.

- Submit for Verification: Send the completed form to your lender to fill in the remaining sections, ensuring they follow any specific submission instructions.

- Review and Submit: Once the lender completes the form, review it for accuracy before sending it to the interested party, often a landlord or potential lender.

Additional Tips

- Ensure due diligence by keeping copies of all submitted documents for your records.

- Communicate clearly with both your lender and any parties requiring the completed verification to facilitate prompt responses.

Who Typically Uses the Verification of Mortgage Form?

Various stakeholders utilize the verification of mortgage form, predominantly in the United States, to confirm the financial status of a borrower.

Primary Users of the Form Include:

- Lenders: Banks and mortgage companies use this form to obtain validation of an applicant's mortgage payments, determining the risk associated with the loan.

- Landlords: Property owners use the verification to assess a tenant’s financial habits, using it as a criterion for leasing decisions.

- Creditors: Any entity extending credit, such as personal loan providers or credit card companies, may require mortgage verification as part of their risk assessment.

- Mortgage Holders: Individuals seeking to refinance or obtain a new loan may need this verification to simplify the application process.

Understanding who utilizes this form can help applicants tailor their documentation for specific needs during the verification process.

Important Terms Related to the Verification of Mortgage Form

Familiarity with key terms associated with the verification of mortgage form is beneficial for accurate completion and understanding.

Key Terms and Their Meanings:

- Verification of Mortgage (VOM): A document that validates the status of a mortgage loan, providing crucial payment and account details.

- Default: This refers to the failure to meet the legal obligations of the mortgage, such as missing payments.

- Creditworthiness: The assessment of how likely an applicant is to repay their debts based on credit history and current financial status.

- Lender: The institution or individual that provides the mortgage to the borrower.

Additional Terminology

- Interest Rate: The cost of borrowing expressed as a percentage of the loan amount.

- Equity: The difference between the market value of a home and the amount still owed on the mortgage.

Understanding these terms is vital for applicants and parties involved to navigate the complexities of mortgage verification effectively.

Steps to Complete the Verification of Mortgage Form

Accurate completion of the verification of mortgage form is crucial for its acceptance and consideration by lenders or landlords.

Detailed Completion Process

- Read Instructions Carefully: Before starting, familiarize yourself with all the instructions on the form to avoid misunderstandings.

- Provide Accurate Information: Include your full name, address, and contact information. Ensure that the loan number is correctly stated, as inaccuracies can lead to delays.

- Detail Loan Information: Fill out specifics about your mortgage, like start date, total amount, and type of loan (fixed/variable).

- Add Payment History: Clearly document your history of payments, noting any instances of late payments or defaults.

- Final Review: Before submission, double-check all filled sections for accuracy and completeness.

Completing this form meticulously can significantly expedite the verification process and provide the necessary assurance to interested parties.