Definition and Meaning of Schedule EIC Form 1010

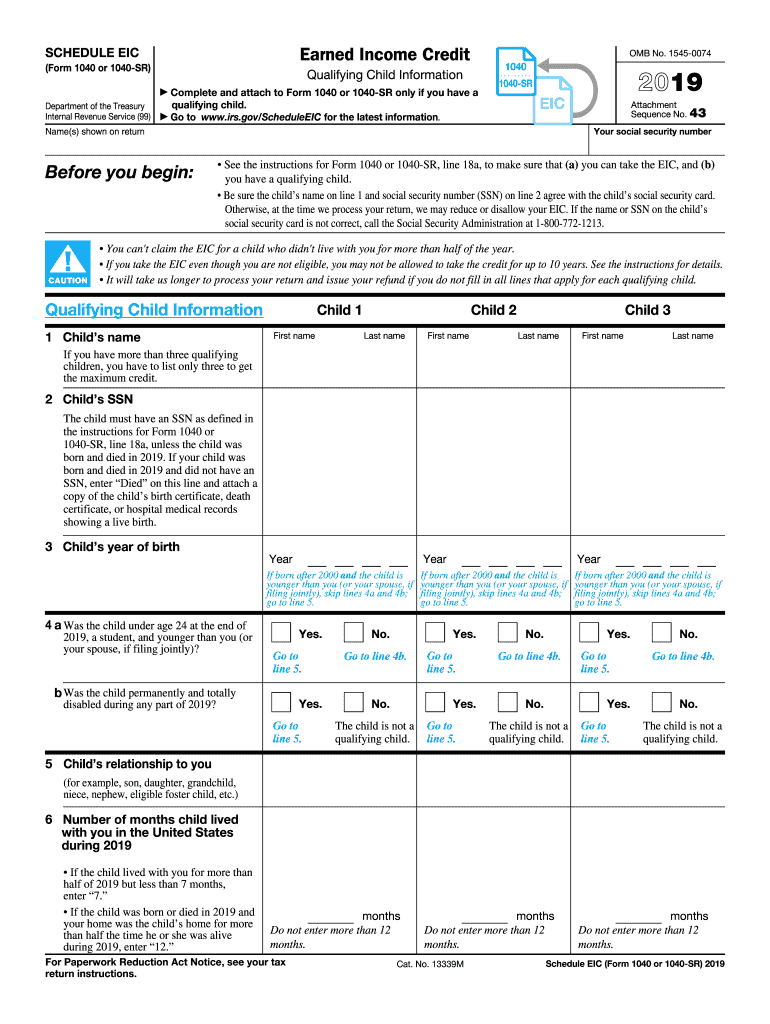

Schedule EIC (Form 1040 or 1040-SR) is a critical document for taxpayers in the United States seeking to claim the Earned Income Credit (EIC). This credit is designed to reduce the tax liability for low to moderate-income working individuals and families, primarily benefiting those with qualifying children. Schedule EIC Form 1010 serves as an auxiliary document to form 1040 or 1040-SR, helping taxpayers report the necessary details about their qualifying children.

Important Terms Related to Schedule EIC Form 1010

- Earned Income Credit (EIC): A tax credit available to low and moderate-income workers, aimed at reducing their tax burden.

- Qualifying Child: A child who meets specific criteria set by the IRS, including age, residency, and relationship requirements.

- Form 1040/1040-SR: Primary tax forms used by individuals to file their annual tax returns, to which Schedule EIC is attached.

How to Use the Schedule EIC Form 1010

To effectively use Schedule EIC Form 1010, taxpayers need to compile detailed information regarding their qualifying children. This includes each child's name, Social Security number, relationship to the filer, and the duration of residency throughout the year. The form is vital for accurately reporting these details to qualify for and maximize the EIC benefit, which can significantly reduce overall tax liability or increase potential tax refunds.

Steps to Complete the Schedule EIC Form 1010

-

Gather Personal and Child Information:

- Collect Social Security numbers and birth dates of each child.

- Verify that each child meets the IRS criteria for a qualifying child.

-

Fill Out Basic Identification Details:

- Enter your name and Social Security number at the top of the form.

-

Provide Details for Each Child:

- For each qualifying child, enter their full name, Social Security number, and date of birth.

- Specify the child's relationship to you and the total number of months they lived with you during the tax year.

-

Review and Attach:

- Double-check all information for accuracy to avoid delays or penalties.

- Attach Schedule EIC to the filled Form 1040 or 1040-SR before submission.

Eligibility Criteria for the Schedule EIC Form 1010

The eligibility criteria for using Schedule EIC form primarily involve income limits, filing status, and residency requirements. Taxpayers must have earned income within IRS-specified limits and possess valid Social Security numbers for themselves and their qualifying children. It is essential that the primary residence for both the taxpayer and the child be in the U.S. for more than half the tax year.

Qualifying Child Criteria:

- The child must be under 19 years old (or 24 if a full-time student) at the end of the tax year, or any age if permanently disabled.

- The child must have lived with the taxpayer for more than six months within the year.

Examples of Using the Schedule EIC Form 1010

Consider a single parent with two children, ages eight and twelve, who lived with them for the entire tax year. By completing Schedule EIC, the parent can list both children as qualifying and significantly increase their EIC amount, thereby reducing their tax liability or enhancing their refund.

In a scenario involving joint filers, if both taxpayers work low-wage jobs, inclusion of qualifying children in Schedule EIC can yield a substantial tax credit. This often results in not just a lower tax bill but sometimes a sizeable refund, which can be a financial boon.

Penalties for Non-Compliance

Non-compliance with IRS regulations related to Schedule EIC can lead to penalties, including repayment of claimed credits and additional fines. Deliberate misreporting of qualifying child information may lead to a ban on claiming the EIC in future years.

Consequences of Incorrect Claims:

- Overstating child-related credits can result in billing notices from the IRS demanding repayment of credits plus interest.

- Habitually incorrect filings could lead to an audit, where more substantial penalties and denial of credits in banned years can occur.

IRS Guidelines and Filing Deadlines

IRS guidelines specify that Schedule EIC Form 1010 must be submitted alongside your annual tax return by the appointed federal tax deadline, usually April 15. Extension requests for filing a tax return can be made, but the extension does not apply to tax payment deadlines.

Required Documents:

- The taxpayer should have all relevant documentation, including the child's Social Security card, birth certificate, and any school or medical records verifying residency requirements.

Form Submission Methods

Taxpayers can submit Schedule EIC Form 1010 electronically or via mail, depending on how they file their full 1040 or 1040-SR return. Electronically filing tax returns, including Schedule EIC, can expedite processing and reduce error rates compared to paper submissions.

Online Submission:

- Leverage IRS-approved tax software to fill out and transmit your tax forms.

Mailing Instructions:

- If filing by paper, ensure Schedule EIC is properly attached to your Form 1040 or 1040-SR and mailed to the correct IRS address.

State-Specific Rules for Schedule EIC Form 1010

While Schedule EIC primarily pertains to federal tax filing, some states may have additional requirements for reporting earned income credits on state tax forms. Taxpayers should consult state guidelines to determine eligibility for any further state-based credits.

Differences to Consider:

- Some states offer their own earned income credits or have specific adjustments needed on the state tax return, demanding careful attention to state tax instructions in addition to federal compliance.

By following these structured guidelines and insights, U.S. taxpayers can optimize their use of Schedule EIC Form 1010 to claim the Earned Income Credit accurately and efficiently.