Definition and Purpose of Schedule C (2013)

Schedule C (Form 1040) for the year 2013 is primarily used by sole proprietors to report their business income and expenses, helping them to calculate their net profit or loss. This document plays a critical role in the tax process for individuals running a business or trade alone, assisting in fulfilling federal tax obligations. It includes sections dedicated to various elements of business operations, such as income, expenses, and cost of goods sold, offering a detailed breakdown of financial activities for the year.

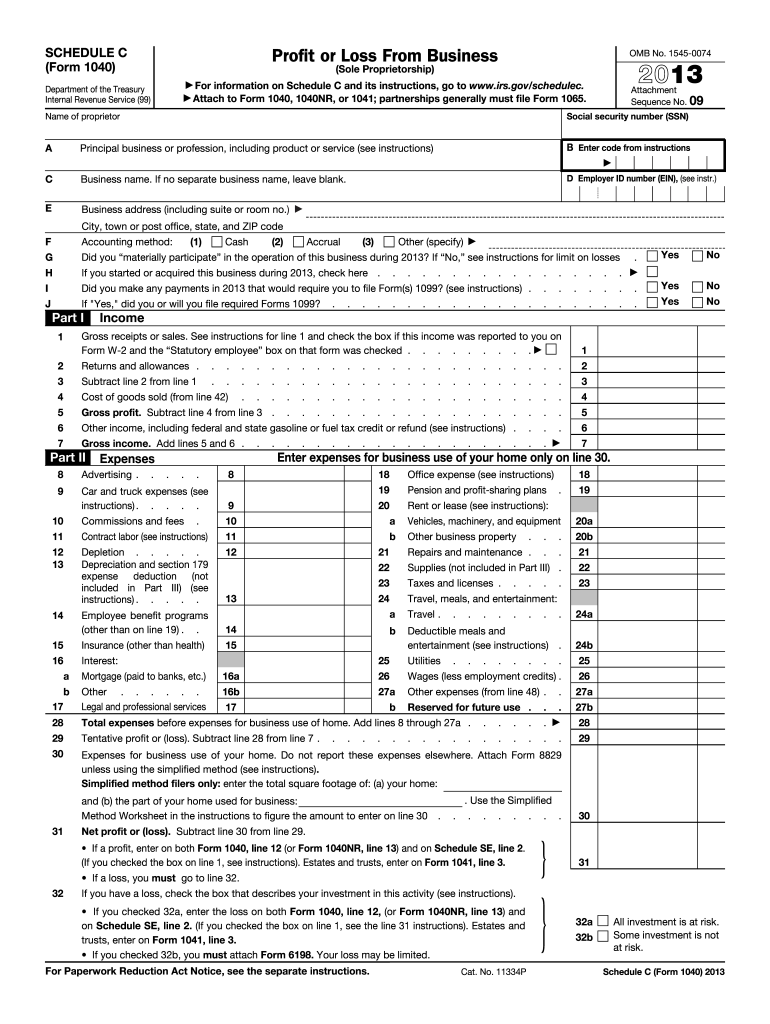

How to Use Schedule C (2013)

To use the Schedule C 2013 form effectively, begin by gathering all necessary financial documents that outline your income and expenses for the year in question. This includes sales receipts, invoices, and records of business expenses. Structuring your form accurately involves:

- Filling in personal information, including name and Social Security Number, at the top of the form.

- Completing Part I to record gross receipts or sales, returns, and allowances, and other income items.

- Proceeding to Part II to document your business expenses categorized by type, such as advertising, car expenses, and travel.

- Using Part III if you have a Cost of Goods Sold, which requires inventory numbers to calculate the cost.

- Moving on to the remaining sections as applicable to your situation, ensuring all figures are accurate to avoid potential IRS scrutiny.

Steps to Complete the Schedule C (2013)

Completing the Schedule C 2013 form involves several steps:

-

Section A - Gross Income:

- Record total income, including all sales and other business-related income, minus any returns or allowances.

-

Section B - Business Expenses:

- List ordinary business expenses under detailed categories such as wages, rent, and utilities. Ensure you have supporting documentation for each expense.

-

Section C - Cost of Goods Sold (COGS):

- Calculate the beginning and ending inventory to determine COGS for businesses that sell products.

-

Section D - Vehicle Information:

- If applicable, include any vehicle expenses such as mileage and depreciation. Maintain a dedicated mileage log for accuracy.

-

Final Review:

- Thoroughly review each section for accuracy, ensuring every entry is supported by documentation.

Key Elements of Schedule C (2013)

The form is structured with essential components crucial for accurately reporting business finances:

- Income Section: Captures total receipts, sales, or revenue generated by the business.

- Expense Section: Allows the deduction of costs associated with running the business, fostering an accurate portrayal of net income.

- Cost of Goods Sold: Essential for businesses dealing with inventory, necessitating the calculation of the cost basis for goods sold.

- Supplementary Expenses: Covers additional costs not itemized in the primary expense section, such as various miscellaneous costs.

Who Typically Uses Schedule C (2013)

Schedule C (2013) is primarily employed by sole proprietors and single-member LLCs who must report their business income and deductions. The form is particularly relevant for freelancers, independent contractors, and small business owners who run their operations without formally incorporating their business as a separate taxable entity.

IRS Guidelines for Schedule C (2013)

Adhering to IRS guidelines is crucial when filing the Schedule C form. Key rules include:

- Accurate Recording: All income and expenses must be accurately reported to prevent underreporting or misrepresentation.

- Documentation: Maintaining proper documentation for all reported income and expenses is essential, as the IRS may request this proof in case of an audit.

- Filing Deadlines: Ensure timely submission aligned with the broader tax filing deadline, typically the 15th of April, unless extended.

Important Terms Related to Schedule C (2013)

Several terms are commonly associated with the Schedule C (2013) form:

- Ordinary and Necessary Expenses: Business expenses must be ordinary and necessary to qualify as deductible.

- Depreciation: A tax deduction spread over the useful life of business assets.

- Self-Employment Tax: Additional tax levied to cover Social Security and Medicare contributions, reported on this form.

- Net Profit/Loss: The final calculated value post-expense deductions which affects overall taxable income.

Filing Deadlines / Important Dates

For the 2013 tax year, the filing deadline for the Schedule C form coincided with the broader individual tax filing deadline:

- Regular Deadline: April 15, 2014

- Extension Deadline: October 15, 2014 (if an extension was filed)

Understanding and adhering to these deadlines is critical to avoid penalties and ensure compliance with federal tax obligations.