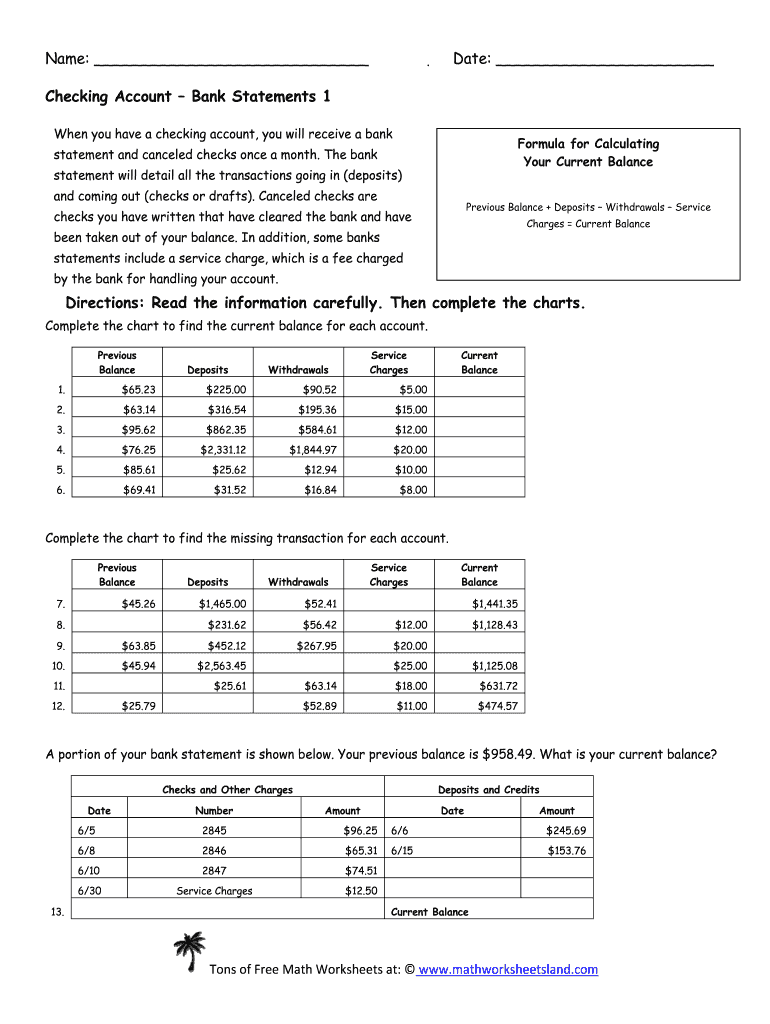

Understanding Checking Account Bank Statements

Detailed knowledge of checking account bank statements is crucial for effective financial management. These documents serve as official records of the transactions and balances in a checking account over a specific period, typically monthly.

The Importance of Bank Statements

Bank statements provide a comprehensive overview of account activity and are essential for:

- Reconciling Accounts: Users can compare their personal records with the bank's records to ensure accuracy.

- Tracking Spending: Statements help users understand their spending habits and identify areas for potential savings.

- Identifying Errors: Regular review of statements allows users to spot unauthorized transactions or bank errors.

Frequency of Statement Issuance

Most banks typically issue checking account statements on a monthly basis. However, users may have options for:

- Daily Statements: Some banks offer daily transaction alerts.

- Quarterly Statements: Accounts with infrequent activity may receive statements quarterly.

Understanding how frequently John typically receives account statements from his bank can help to gauge the bank’s customer service practices and the relevance of the information delivered.

Components of a Checking Account Statement

Checking account statements generally include the following sections:

- Account Information: Account holder's name, account number, and statement date.

- Transaction History: A detailed list showing deposits, withdrawals, and fees incurred.

- Balance Summary: Starting balance, total deposits, total withdrawals, and ending balance for the period.

This information is crucial for customers to maintain an accurate understanding of their financial standing.

Key Terms to Know

Several important terms frequently appear on checking account statements. Understanding these can enhance clarity when reviewing financial documents:

- Cleared Transactions: Transactions that have been processed and posted to the account.

- Pending Transactions: Transactions that have been initiated but not yet processed.

- Overdraft Fees: Charges incurred when the account balance goes below zero.

How to Reconcile Bank Statements

Reconciliation involves comparing bank statements with personal records. Here’s a step-by-step process:

- Gather Documents: Collect the bank statement and personal transaction records.

- Match Transactions: Check off transactions that appear in both the bank statement and personal records.

- Identify Discrepancies: Note any differences, such as missing transactions or discrepancies in amounts.

- Correct Errors: Investigate and resolve any identified issues.

Regular reconciliation ensures that your financial records are accurate and complete.

Digital Banking Features Related to Bank Statements

Many banks offer online banking platforms, allowing easy access to checking account bank statements. Key features often include:

- Online Statements: Availability of electronic statements which can be stored and managed digitally.

- Transaction Alerts: Notifications for activities, enhancing awareness of account changes.

- Download Options: Ability to download statements in various formats, including PDF and CSV.

These digital banking features facilitate effective management of financial activities.

Planning for Tax Season

Bank statements can be instrumental during tax season, especially for individuals with significant transactions. Users often need to keep records of:

- Income Sources: Ensuring all income is reported accurately.

- Deductible Expenses: Identifying expenses that may qualify for tax deductions.

Retention of these documents contributes to a more streamlined tax preparation process.

Conclusion on Checking Account Management

Understanding checking account bank statements, including how to read and utilize them, is vital for effective financial oversight. Regular review and management of these documents enhance budgeting capabilities, track spending, and ensure compliance with financial obligations.