Definition and Significance of CG 20 10 10 01

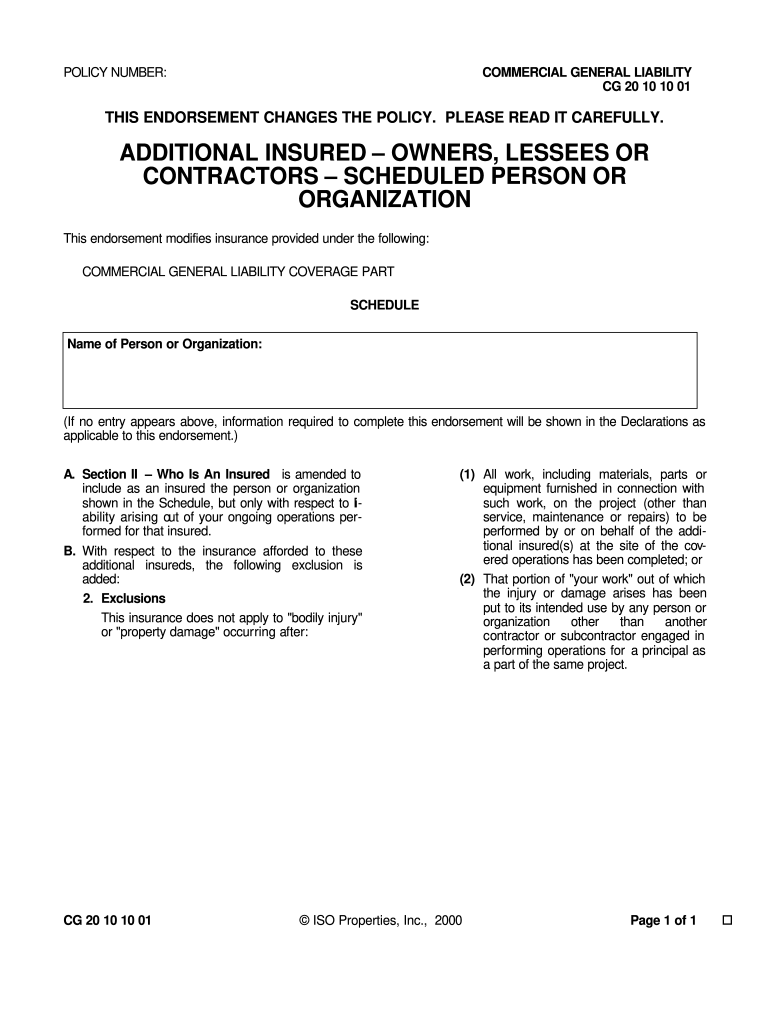

The CG 20 10 10 01 form is a specialized endorsement in the realm of Commercial General Liability (CGL) insurance. Specifically, it pertains to the inclusion of additional insured parties under a liability policy, highlighting conditions under which these parties are covered for liabilities arising from ongoing operations performed on their behalf.

- Purpose of the Form: This endorsement is primarily designed to extend coverage to parties that may not be named in the original policy but require protection due to contractual obligations or project demands. This is particularly important in industries such as construction, where contracts often necessitate such provisions to limit the exposure of the primary contractor.

Key Features of CG 20 10 10 01

Several integral attributes characterize the CG 20 10 10 01 form:

- Coverage Scope: The endorsement specifies that additional insured parties are covered for liabilities associated with ongoing operations performed for them. This can include incidents occurring on job sites or during project execution.

- Exclusions: It explicitly states exclusions for certain liabilities. For instance, it does not cover bodily injury or property damage that occurs after the work has been completed or once the work has been put to its intended use. This delineation helps clarify to all involved parties when coverage applies and when it does not.

- Requried Documentation: Typically, this form is appended to the main policy and requires documentation from both the primary insured and additional insured indicating agreement to the terms.

Utilization of CG 20 10 10 01 in Professional Settings

In practical terms, the CG 20 10 10 01 is widely used across various industries, particularly where third-party interactions are common, such as construction and real estate.

- Contractor Applications: Contractors often utilize this form when engaging with subcontractors or other third parties. For instance, a general contractor may need to provide proof of coverage to the property owner, ensuring that the owner is protected against claims arising from the contractor's operational activities.

- Real Estate Transactions: In real estate deals, property owners may request this form to ensure that they are covered against any incidents that arise out of construction or maintenance work conducted on their premises.

How to Use the CG 20 10 10 01

To effectively utilize the CG 20 10 10 01 form, follow these steps:

- Identify Additional Insured Parties: Determine which parties need to be covered. This often includes property owners, general contractors, or other related entities.

- Modifying the Policy: Coordinate with your insurance provider to amend your existing CGL policy to include these additional insured parties under the specific terms outlined in the CG 20 10 10 01.

- Submission for Approval: Complete and submit the endorsement to your insurer, providing evidence that all parties have consented to the coverage changes.

Importance of Compliance with CG 20 10 10 01

Ensuring compliance with the stipulations set forth by the CG 20 10 10 01 is vital for minimizing risk exposure and ensuring that all parties are adequately protected.

- Contractual Obligations: Many contracts stipulate the requirement for additional insured endorsements to mitigate risks associated with project-related activities.

- Risk Management: Properly documenting the inclusion of additional insured parties through this form is an effective risk management strategy that can mitigate potential liabilities and disputes arising from commercial operations.

Variants and Related Forms

The CG 20 10 10 01 is one of several related endorsements used in the insurance industry. Understanding its relationship with similar forms, such as CG 2010 and CG 2037, can help stakeholders navigate contractual and insurance landscapes effectively.

- CG 2010: This form, also known as the "Additional Insured – Owners, Lessees or Contractors – Scheduled Person or Organization," provides a more tailored approach for specific entities rather than a blanket coverage.

- CG 2037: The "Additional Insured – Owners, Lessees or Contractors – Automatic Status When Required in Construction Agreement with You" gives broader automatic coverage to additional insured entities, simplifying the insurance process for ongoing projects.

Common Scenarios Involving CG 20 10 10 01

Practical scenarios where the form may come into play include:

- Construction Projects: A main contractor working on a large project might be required to add the property owner as an additional insured on their liability policy through the CG 20 10 10 01 to meet insurance requirements.

- Event Planning: An event organizer hiring third-party service providers may use the form to ensure that vendors and subcontractors are also covered in case of incidents during the event.

Legal Context and Compliance

The CG 20 10 10 01 form is designed to comply with the legal frameworks surrounding liability coverage in the United States, ensuring that businesses adhere to state-specific regulations regarding insurance and liability protection.

- Understanding Local Regulations: Each state may have different requirements regarding endorsements and additional insured status, so it is crucial to verify compliance with local laws.

- Audit Trails: Keeping a complete record of all endorsements and agreements related to the CG 20 10 10 01 helps ensure legal compliance and protects against potential disputes arising from liability claims.

Conclusion

The CG 20 10 10 01 form plays a critical role in the intersection of liability coverage and risk management for businesses engaged in industries requiring additional protection for various stakeholders. Understanding and utilizing this endorsement properly can safeguard against significant financial losses that can arise from operational risks.