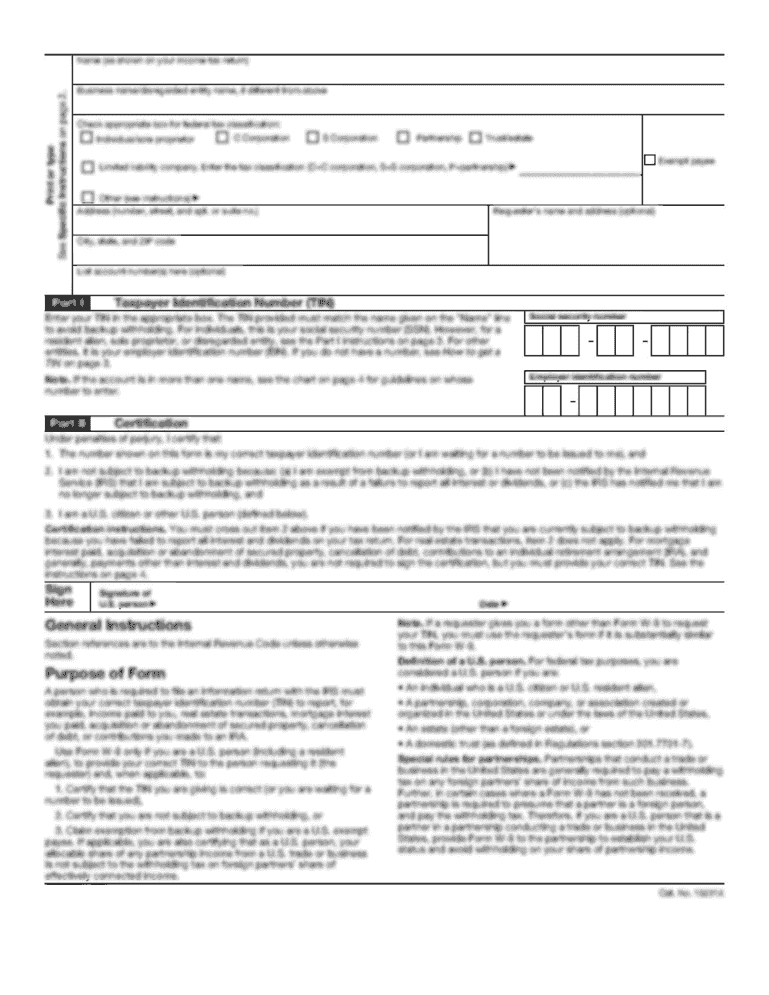

Definition and Meaning

The 1998 Schedule CA(540) - California Adjustments Residents, 1998 FTB 3885A - Depreciation and Amortization Adjustments, and 1998 Schedule D(540) - California Capital Gain or Loss Adjustment are essential tax documents for California residents. These forms allow taxpayers to report specific adjustments to federal income, calculate depreciation and amortization adjustments, and manage capital gains or losses unique to California tax laws. Understanding these documents is crucial to ensuring accurate tax reporting and compliance with state regulations.

How to Use the Forms

To use the 1998 Schedule CA(540), taxpayers must report any state-specific income modifications not reflected in their federal tax returns. This includes differences in interest income, personal exemptions, and various deductions unique to California. For the 1998 FTB 3885A, you will adjust the depreciation and amortization reported on your federal return to reflect California’s methods and conforming guidelines. The Schedule D(540) is used to account for discrepancies between federal and state tax treatments of capital gains or losses, especially pertinent when property values differ due to state assessments.

How to Obtain These Forms

The forms can be obtained directly from the California Franchise Tax Board's website or requested by mail. Tax preparation software frequently includes these forms, streamlining the process for those who file electronically. It's advisable for users to verify that they are accessing the forms for the correct tax year, ensuring compliance with 1998-specific tax guidelines and avoiding the use of outdated or incorrect versions.

Steps to Complete the Forms

- Gather Necessary Information: Have your federal tax return, income statements, and records of deductions ready.

- Adjust Federal Income: Use Schedule CA(540) to make necessary additions or subtractions from your federal adjusted gross income.

- Depreciation and Amortization Adjustments: Complete the FTB 3885A to adjust federal depreciation amounts to align with California’s tax rules.

- Calculate Capital Gains or Losses: On Schedule D(540), adjust the capital gain or loss entries to match California’s tax policies.

- Review for Accuracy: Double-check entries for each form to ensure correctness before submission.

- Submission: File the completed forms with your California state tax return by mail or electronic submission through approved tax software.

Who Typically Uses These Forms

The primary users of these tax forms are California residents who require specific income adjustments, possess depreciable assets, or have experienced capital transactions during the tax year. This includes individuals, couples filing jointly, and business entities operating within California. Understanding the requirements for these forms ensures accurate reporting for those engaging in diverse financial activities influenced by state-specific tax laws.

Key Elements of Schedule CA(540)

The 1998 Schedule CA(540) features sections for adjusting federal adjusted gross income, including separate lines for interest/dividend income, business income, and itemized deductions. California residents must report supplementary income adjustments that differ from federal calculations, emphasizing the discrepancy in personal exemptions between state and federal filings. Notable areas to address include student loan interest deductions and self-employment tax adjustments.

Subsection: Schedule D(540) Components

Schedule D(540) focuses on capital gains or losses. Its crucial components include the computation of gains or losses from asset sales, with adjustments for state-specific valuation rules. Taxpayers should note variance in how California treats specific capital assets compared to federal guidelines, impacting the final taxable amount.

State-Specific Rules

California has distinct rules affecting the calculation of depreciation and amortization, as reflected in FTB 3885A. For example, California residents might not recognize bonus depreciation available in federal returns. Similarly, state tax law may demand a different treatment of like-kind exchanges, affecting the recognized gain or loss.

Important Terms Related to the Forms

Familiarity with essential terminology like "Adjusted Gross Income (AGI)," "Depreciation Conventions," and "Capital Gains Taxation" is vital. Understanding these concepts ensures precise form completion and reveals implications on overall tax liability. These terms often embody differences between federal and California state tax systems, necessitating accurate interpretation.

Filing Deadlines and Important Dates

The deadline for filing the 1998 Schedule CA(540), FTB 3885A, and Schedule D(540) aligns with California's general tax filing deadline, typically April 15. Extensions are available, similar to federal returns, but require proactive application. Timeliness in filing eliminates late penalties and interest charges, safeguarding against compliance issues.

Penalties for Non-Compliance

Failure to submit these forms correctly or within deadlines may result in penalties such as fines or interest accrual on owed taxes. Non-compliance with California-specific tax regulations can lead to audits or further legal complications. Hence, meticulous attention to detail and adherence to submission protocols is crucial for avoiding repercussions.