Definition and Meaning of 2-C Form

The 2-C form is a tax document used by creditors to report the cancellation or forgiveness of a debt to the IRS. When a debt of $600 or more is canceled by a financial institution, government agency, or credit company, the creditor must file this form to inform both the debtor and the IRS. The form is critical as the forgiven debt is often considered taxable income for the debtor, influencing their federal income tax obligations. Understanding this form is essential for both creditors and debtors to accurately report canceled debts and avoid potential penalties.

How to Use the 2-C Form

Using the 2-C form involves several steps for both creditors and debtors. Creditors must accurately fill out the form, ensuring all required fields, such as the amount of canceled debt and the debtor's identification information, are correctly entered. Debtors, upon receipt, should review the form for accuracy and report the canceled debt as income on their tax return unless they qualify for an exclusion or exception. This form helps maintain transparency and accuracy in tax reporting for canceled debts.

Steps for Creditors

- Gather debtor information: Ensure you have updated and accurate debtor details, including Social Security numbers or taxpayer identification numbers.

- Fill out the required fields: Include the date of debt cancellation, amount, and any other relevant creditor codes or information.

- Submit the form to the IRS: File a copy with the IRS and send the debtor their copy by the specified deadline.

Actions for Debtors

- Review for accuracy: Check all information reported by the creditor on the 2-C form.

- Include the income on tax return: Integrate the amount of canceled debt on the appropriate line of the tax return unless an exclusion applies.

- Seek clarification if needed: Contact the creditor if there are discrepancies or errors in the reported information.

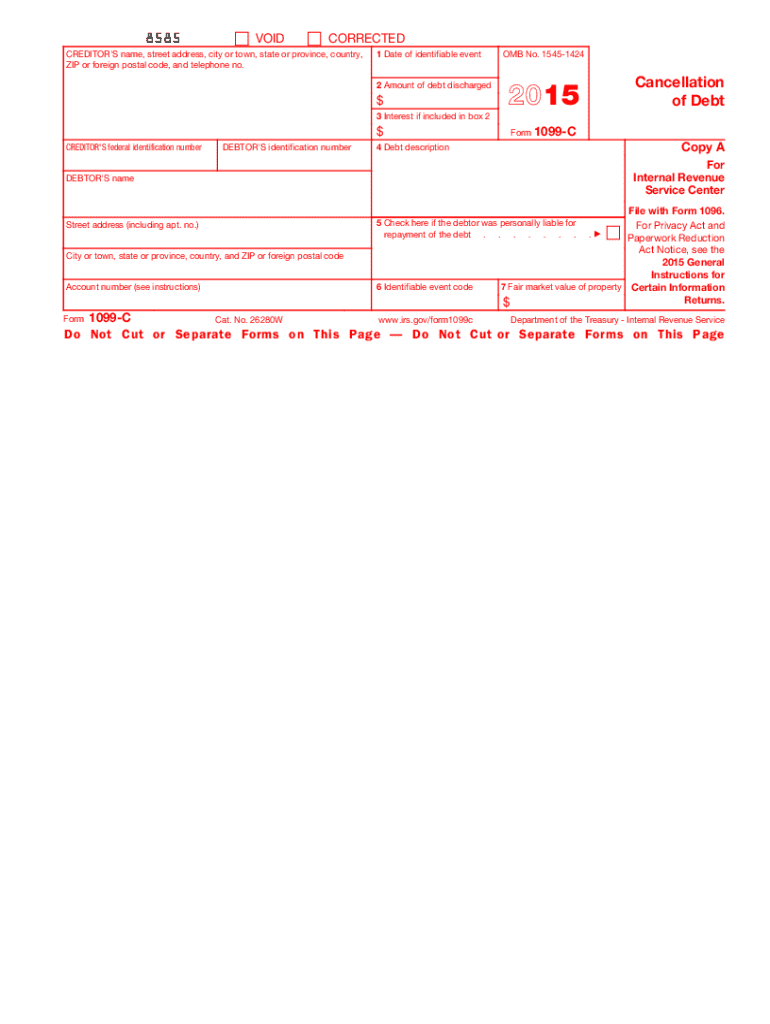

Steps to Complete the 2-C Form

Completing the 2-C form accurately is crucial for compliance with IRS regulations. The process involves detailed documentation and precise entry of information.

- Identify the creditor's details: Begin by entering your company's name, address, and tax identification number.

- Debtor's information: Accurately enter the debtor's name, address, and taxpayer identification number.

- Fill in the amount canceled: Provide the exact amount of debt forgiveness in Box 2.

- Enter the date of debt cancellation: Fill in Box 1 with the appropriate date of debt discharge.

- Additional details: Include any additional information required in subsequent boxes, such as the account number.

- Attach required documentation: Ensure any supporting documents are attached when filing the form with the IRS.

IRS Guidelines and Requirements

The IRS sets specific guidelines for the 2-C form that dictate how it should be completed and submitted. These requirements ensure uniformity and transparency in reporting canceled debts.

- Proper filing: Creditors must file the 2-C form for each debtor whose debt was canceled, except in specific legal exclusions.

- Deadline compliance: Send the debtor's copy by January 31 of the following year, and file the IRS copy by February 28 for paper submissions or March 31 if filing electronically.

- Accurate reporting: Ensure that all data is correct to avoid penalties and additional scrutiny from the IRS.

Filing Deadlines and Important Dates

Meeting deadlines for the 2-C form is crucial to avoid penalties. Specific dates must be adhered to each tax year for the distribution and submission of the form.

- January 31: The deadline to provide the debtor with a copy of the form.

- February 28: The deadline for paper filing with the IRS.

- March 31: The deadline for electronic submissions with the IRS.

Failure to meet these deadlines can result in fines and complications for both creditors and debtors.

Penalties for Non-Compliance

Non-compliance with the annual filing requirements of the 2-C form can incur significant penalties from the IRS. Penalties vary based on how late the form is filed and if there was intentional neglect.

- Late filing fines: Penalties increase with the delay. For forms filed within 30 days, the penalty can be up to $50 per form; more severe penalties apply for later filings.

- Intentional disregard: If non-compliance is intentional, the penalty is substantially increased, often with no maximum limit.

- Debt omission: Misreporting or failing to report can lead to additional tax liabilities for the debtor.

Digital vs. Paper Version of the 2-C Form

The 2-C form can be submitted either digitally or on paper, with each method having its own set of procedures and benefits.

- Digital submission: Offers quicker processing and confirmation from the IRS, suitable for businesses with a high volume of filings.

- Paper version: Traditional method, necessitating physical completion and mailing, suitable for smaller firms with fewer forms.

Regardless of the method chosen, accuracy and adherence to IRS guidelines are crucial to ensure proper handling and reporting of canceled debts.