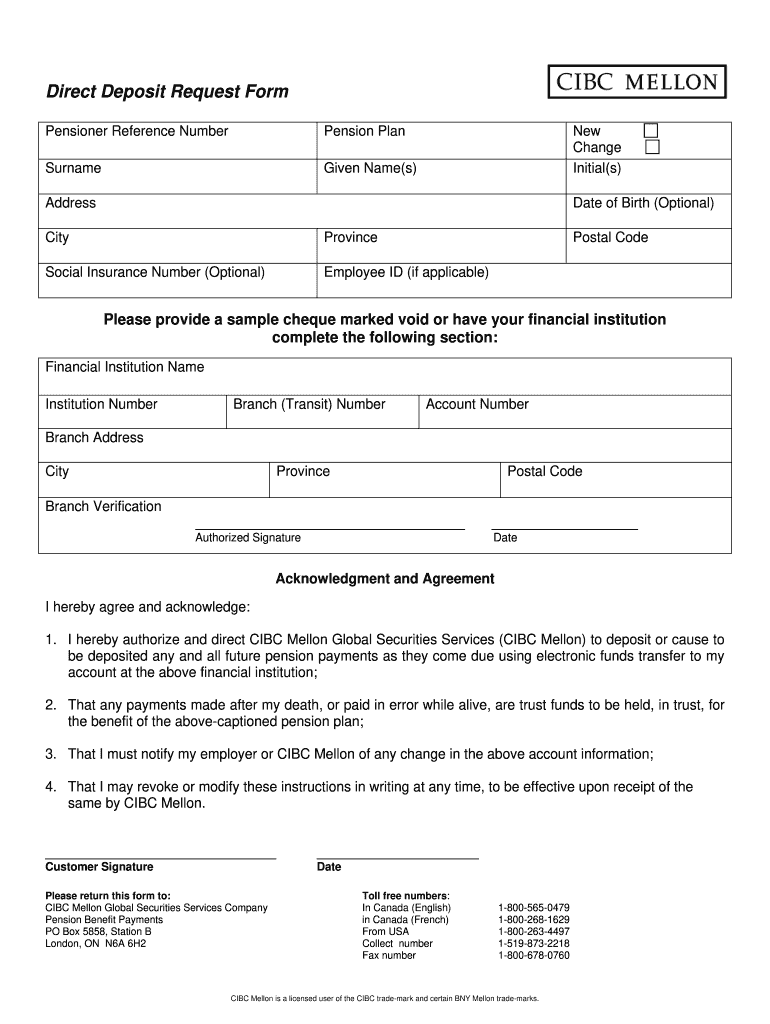

Definition and Purpose of the Direct Deposit Form

The direct deposit form is an official document designed to facilitate electronic funds transfers directly into a bank account. This form streamlines the process of receiving payments, such as wages, benefits, or reimbursements, making it an essential tool for individuals and organizations alike.

Key Features of the Direct Deposit Form

- Personal Information: The form typically requires details like the payee's name, address, and social security number (or tax identification number) to identify the recipient.

- Bank Account Details: It includes fields for the bank's name, account number, and routing number. The routing number is crucial as it directs the payment to the correct financial institution.

- Authorization Statement: The form generally contains an authorization section where the payee grants permission for their funds to be deposited electronically.

Understanding these key elements enhances comprehension of the document's role in financial transactions.

How to Complete the Direct Deposit Form

Filling out the direct deposit form accurately is critical to ensure smooth processing of payments. The following steps outline how to effectively complete this form:

- Personal Information: Start by providing your full name, address, and any identifying numbers, such as your social security number.

- Bank Information:

- Enter the name of your bank or financial institution.

- Fill in the account number where you want the funds deposited.

- Include the bank’s routing number, ensuring it is correct to avoid issues.

- Authorization: Read the terms provided, and if you agree, sign and date the form. This step is vital as it signifies your consent for the direct deposit arrangement.

- Attachments: If required, attach any documentation that may validate your identity or banking details, like a voided check or bank statement.

Tips for Accurate Completion

- Double-check all banking information for accuracy to prevent misdirected funds.

- If submitting digitally, ensure that your electronic signature meets the necessary requirements.

Obtaining the Direct Deposit Form

Obtaining a direct deposit form can typically be done in several ways:

- Online: Many financial institutions provide downloadable PDF versions of the direct deposit form on their websites. This option is often the fastest way to obtain the form.

- In-Person: You can visit your bank or credit union branch to request a physical copy of the direct deposit form.

- Through Employers or Institutions: If you are setting up direct deposit for payroll, your employer may provide a specific form or instructions on how to complete it.

Who Uses the Direct Deposit Form?

Various entities and individuals utilize direct deposit forms for different purposes, including:

- Employees: Workers set up direct deposit to receive salaries directly into their bank accounts, which can improve financial management and access to funds.

- Federal and State Beneficiaries: People receiving government benefits, like Social Security or unemployment payments, use direct deposit to receive funds electronically.

- Self-Employed Individuals: Freelancers or contractors may also request direct deposit for prompt payment.

Understanding the diverse user base highlights the form's significance in ensuring timely access to funds.

Important Terms Related to the Direct Deposit Form

Familiarizing yourself with essential terminologies is crucial when engaging with a direct deposit form:

- Routing Number: A nine-digit number that identifies the bank's location and is required for accurate fund transfers.

- Account Number: The specific number assigned to a bank account which ensures that deposits reach the correct financial account.

- Authorization: A signed consent by the account holder permitting the automatic deposit of funds.

These key terms contribute to a broader understanding of the direct deposit process and its implications.

Legal Use of the Direct Deposit Form

The legal framework surrounding the use of the direct deposit form is defined by regulations such as the Electronic Fund Transfer Act (EFTA). Here are important considerations:

- Consent: It is imperative to obtain the account holder's consent before initiating direct deposits.

- Security Measures: Organizations must implement security protocols to protect personal and financial information, complying with federal laws regarding data protection.

- Record Keeping: Adequate documentation must be maintained for all transactions to provide an audit trail and satisfy regulatory requirements.

Consequences of Non-Compliance

Organizations failing to adhere to these regulations may face penalties, including fines, legal action, or increased scrutiny from regulatory bodies.

Potential Variants of the Direct Deposit Form

While a standard direct deposit form is widely used, there are variations that may be employed based on specific contexts:

- Payroll Direct Deposit Form: Typically used by employers to set up salary deposits, this variant may require additional employment-related information.

- Tax Refund Direct Deposit Form: This version allows individuals to specify how they want their tax refunds deposited, including choice of accounts.

Each version serves critical functions tailored to specific financial transactions, reinforcing the importance of understanding the context in which the form is used.

Examples of Using the Direct Deposit Form

Real-world scenarios illustrate the utility of the direct deposit form across various situations:

- Employee Payroll: A company uses the direct deposit form to set up payroll for its employees, ensuring timely payments without the need for paper checks.

- Government Benefits: A retiree completes a direct deposit form to receive monthly Social Security payments directly into their checking account, thus avoiding delays related to postal services.

- Freelance Payments: A freelancer provides a client with their direct deposit form to facilitate the electronic transfer of payment for services rendered.

These examples highlight the practicality and convenience of using a direct deposit form in everyday financial transactions.