Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out Claims Initiation Kit - for the Federal Long Term Care Insurance...

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

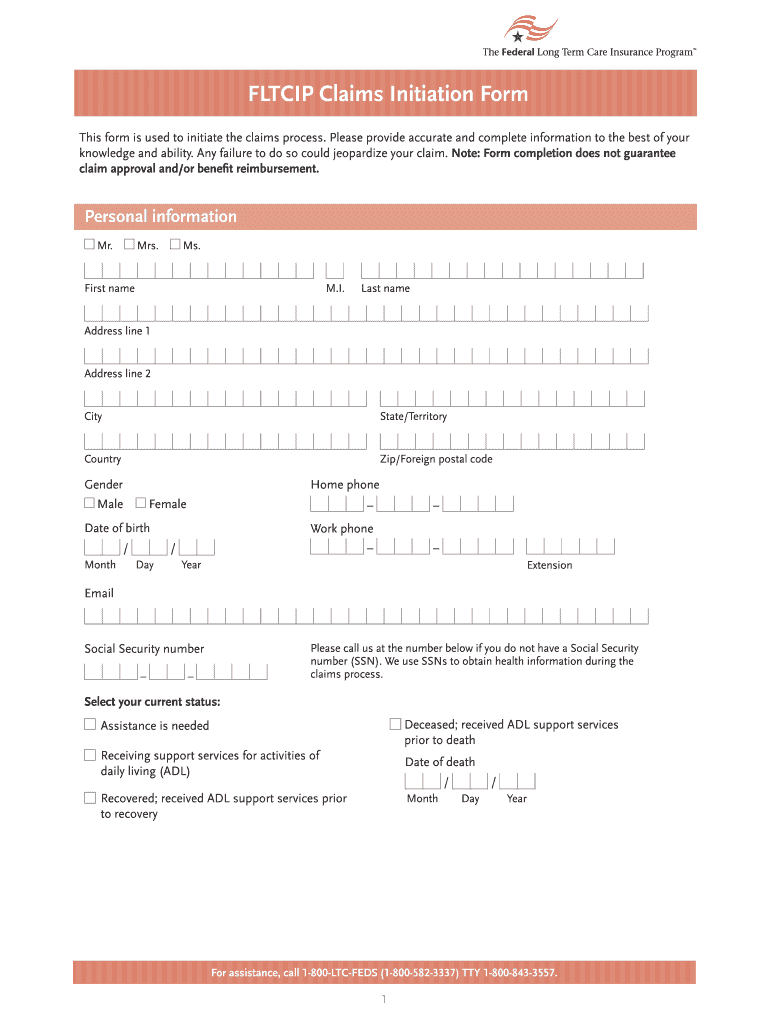

Begin by filling out your personal information. Include your name, address, contact details, and Social Security number if applicable. Ensure all fields are completed accurately.

Indicate your current status regarding assistance needs and living accommodations. Select options that best describe your situation and provide any necessary dates.

In the claim information section, briefly explain why you are filing a claim. Answer questions about your need for assistance with daily activities and cognitive impairments.

Provide detailed insurance information, including any medical insurance you have and long-term care policy details.

Complete the medical information section by listing all relevant healthcare providers and their contact details over the past year.

Finally, review the Agreement and Acknowledgment section. Sign and date the form to certify that all provided information is accurate before submitting it via mail or fax.

Start using our platform today to easily complete your Claims Initiation Kit for free!

Fill out Claims Initiation Kit - for the Federal Long Term Care Insurance... online It's free

See more Claims Initiation Kit - for the Federal Long Term Care Insurance... versions

We've got more versions of the Claims Initiation Kit - for the Federal Long Term Care Insurance... form. Select the right Claims Initiation Kit - for the Federal Long Term Care Insurance... version from the list and start editing it straight away!

What is the biggest drawback of long-term care insurance?

FLTCIP is insurance that pays benefits towards the cost of covered services that individuals receive if they are unable to perform everyday tasks due to a chronic mental or physical condition. For example, FLTCIP helps pay for home health care, adult day care, or for nursing home or assisted living facility costs.

Why is OPM suspending long-term care insurance?

The combination of ongoing volatility in long term care costs and a diminished insurance market are undermining the programs ability to establish new premium rates that reasonably and equitably reflect the cost of the benefits provided (as required under federal law).

What is the oldest age for long-term care insurance?

It IS possible to still purchase long-term care insurance at age 75 (79 is generally the cut off). BUT its going to be highly dependent on your current health. The few insurers who accept applicants at age 75 reject almost half of the applicants.

Who offers the best long-term care insurance?

Best long-term care insurance Best for seniors: Mutual of Omaha. Best for comparison shopping: GoldenCare. Best hybrid long-term care insurance: Nationwide. Best for couples: New York Life. Best for customer service: MassMutual. Best for high benefit limits: Northwestern Mutual. Best for inflation protection: Brighthouse.

Why did Opm suspend FLTCIP?

OPM has determined that this extension of the FLTCIP suspension of applications for coverage is in the best interest of the Program due to ongoing volatility in long term care costs and a diminished insurance market, which are undermining the ability to establish benefit offerings with premium rates that reasonably and

Related Searches

Claims initiation kit for the federal long term care insurance templateClaims initiation kit for the federal long term care insurance pdfClaims initiation kit for the federal long term care insurance formClaims initiation kit for the federal long term care insurance 2022FLTCIP claims Initiation FormWhy was Federal long term care insurance suspendedFederal long term care insurance reviewsFederal long term care insurance cost

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

26 CFR 54.9815-2719T - Internal claims and appeals and

(4) The plan and issuer must provide a description of available internal appeals and external review processes, including information regarding how to initiateRead more

Feb 8, 2018 Long-Term Care Insurance. Long-term care insurance contracts generally are treated as accident and health insurance contracts. Amounts you.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.