Definition & Meaning of the R 940

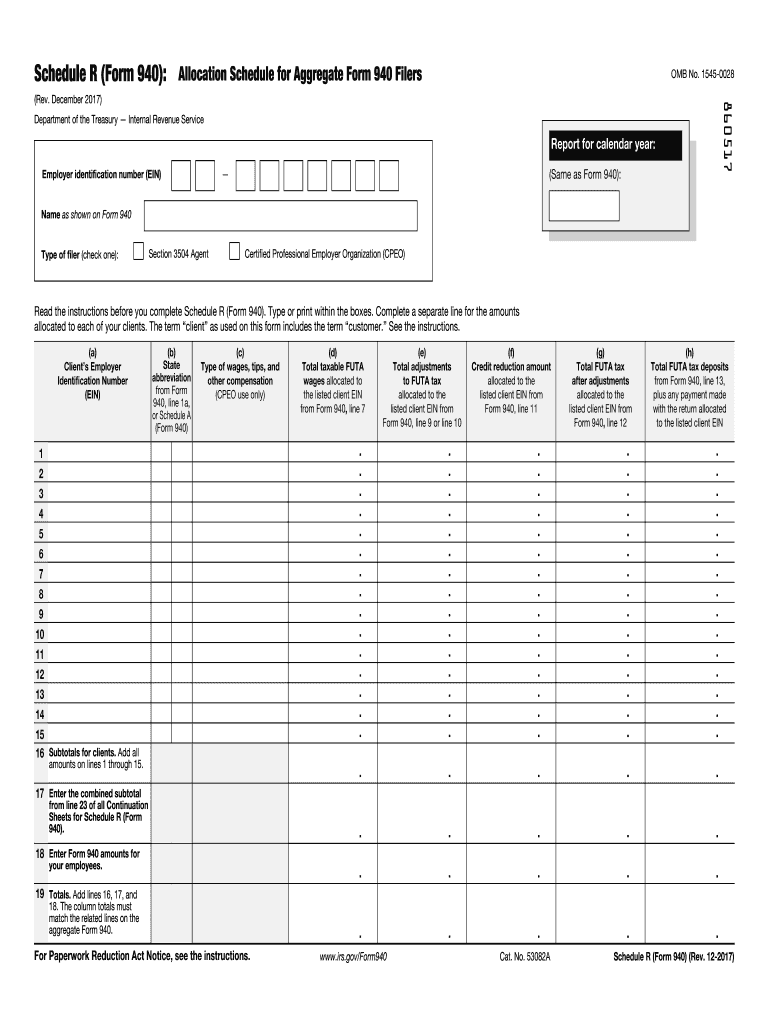

Schedule R (Form 940) is a formal document utilized by certified professional employer organizations (CPEOs) and section 3504 agents. This form serves to allocate aggregate information reported on Form 940 to individual clients. The data on Schedule R must detail each client’s Employer Identification Number (EIN), the type of wages paid, the state in which wages were paid, and various tax amounts tied to the Federal Unemployment Tax Act (FUTA). The precise handling of these data points is essential for ensuring legal compliance and avoiding discrepancies in unemployment tax reporting.

Detailed Components of the Form

- Employer Identification Number (EIN): Each client's unique federal tax identifier, crucial for tracking and identifying tax responsibilities.

- State Identification: Specifies where the wages were paid, ensuring adherence to local tax regulations.

- Wage Types and Amounts: Breaks down the categories and sums of wages subjected to FUTA tax.

- Total Allocation: Ensures figures align with those reported on the aggregate Form 940 to avoid errors.

How to Use the R 940

Using the Schedule R (Form 940) requires careful attention to detail. Start by collecting comprehensive data on each client, including the EIN and wage details. Enter this information accurately to match the overall amounts declared on Form 940. Ensuring consistency between Schedule R and Form 940 is critical to avoiding penalties. This form is typically filed annually, accompanying Form 940 as a supplementary document, and must be prepared with precision to ensure all client data is accurately represented.

Steps to Complete the R 940

Filing Schedule R (Form 940) involves several key steps:

- Gather Required Information: Collect all necessary data, including each client's EIN and relevant wage details.

- Accurate Data Entry: Enter the gathered data on Schedule R, ensuring precise representation of client information.

- Ensure Consistency: Verify that all data align with what's reported on the primary Form 940.

- Review for Errors: Double-check entries for any inaccuracies or inconsistencies.

- Submit with Form 940: Schedule R must accompany Form 940 to provide detailed client allocation.

Why Should You File the R 940

Filing Schedule R (Form 940) is essential for CPEOs and section 3504 agents who handle payroll on behalf of multiple clients. It allows these entities to detail each client's share of FUTA tax, ensuring that all tax liabilities are correctly allocated. By doing so, organizations maintain transparency and accuracy in tax reporting, align with IRS requirements, and minimize the risk of facing penalties for non-compliance.

Important Terms Related to the R 940

Understanding specific terms associated with Schedule R (Form 940) is critical:

- FUTA: The Federal Unemployment Tax Act, which mandates taxation on individuals' wages to fund unemployment compensation.

- CPEO: Certified Professional Employer Organization, a designation allowing companies to manage payroll, taxes, and human resources for their clients.

- Section 3504 Agent: An agent authorized to perform acts required of employers, responsible for correct tax filing on behalf of clients.

IRS Guidelines for R 940

The IRS provides specific guidelines for preparing and submitting Schedule R (Form 940). These instructions emphasize the importance of accurate data entry and the necessity for entries to correlate with those on Form 940. Additionally, CPEOs and section 3504 agents must ensure the document is filed alongside Form 940 within the stipulated deadlines to maintain compliance and uphold legal obligations.

Filing Deadlines and Important Dates

Schedule R (Form 940) must be filed annually in line with Form 940’s submission timeline. Typically, Form 940 is due by January 31 following the year of reporting. However, if an organization has made timely deposits in full payment of the taxes due for the year, they may be granted a ten-day grace period. Staying informed of these deadlines ensures that reports are filed timely and penalties for late submission are avoided.

Penalties for Non-Compliance

Non-compliance with Schedule R (Form 940) filing requirements can lead to significant penalties. Common issues include late submission, missed deadlines, or discrepancies between Schedule R and Form 940. Penalties can include fines and interest on unpaid taxes. Therefore, maintaining accuracy and submitting all required documentation within prescribed deadlines is paramount to avoiding fiscal penalties and legal complications.