Definition & Meaning

The Form W-2, commonly known as the Wage and Tax Statement, is utilized by employers to report employees' annual wages and the amount of taxes withheld from their paychecks for the respective year. For the 2006 tax year, this document provides critical information about an employee's earnings and tax contributions, both of which are essential for accurate tax filing. The form includes details such as social security numbers, taxable fringe benefits, and retirement plan information. This standardized document is mandated by the Internal Revenue Service (IRS) to ensure consistent reporting of taxable income across the United States.

How to Obtain the W-2 2006 Form

Employers issue the W-2 2006 Form to employees by mailing it to their registered addresses or providing access through an online employee portal. For employees who misplaced or never received their form, contacting the employer's payroll department is a recommended first step. Additionally, the Social Security Administration (SSA) offers a resource to order past forms. It's essential to ensure that the employer has the correct mailing address to avoid misplacement of crucial tax documents.

Steps to Complete the W-2 2006 Form

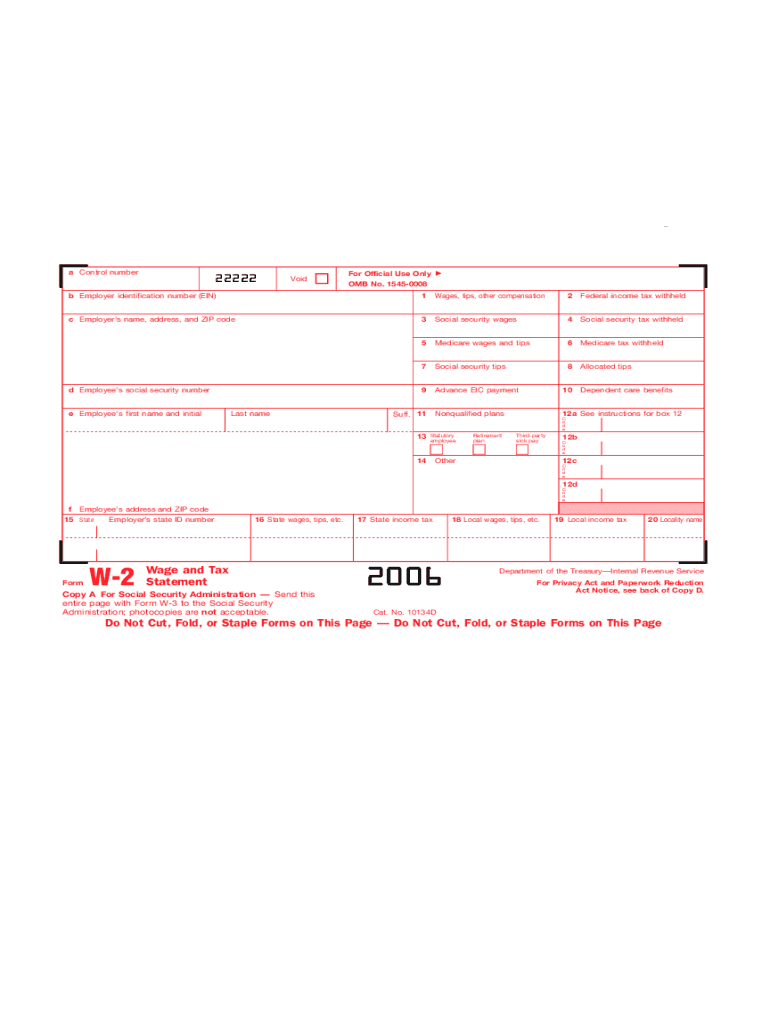

- Employer Information: Begin by filling out the employer's details, including the Employer Identification Number (EIN), name, and address.

- Employee Information: Accurately input the employee’s details, such as their social security number, name, and address.

- Wage Details: Report the total wages paid, along with the taxes withheld, into the respective boxes.

- Benefits and Deductions: Include taxable fringe benefits, retirement plan contributions, and any other relevant deductions.

- Review and Distribute: Double-check for accuracy. Once all entries are verified, distribute copies to the employee, nearby state agencies, and file with the SSA.

Legal Use of the W-2 2006 Form

The legal framework surrounding the W-2 Form requires that employers furnish this document to both employees and the SSA to ensure statutory compliance. Filing must adhere to the deadlines set by the IRS to avoid legal ramifications. This form is pivotal in verifying income and tax contributions, influencing both state and federal tax reporting. Employers failing to issue the form on time, or employees not using the W-2 when completing their tax returns, may face penalties.

Key Elements of the W-2 2006 Form

- Employee's Wage and Withholding Information: Clear indication of gross income and withheld taxes.

- Employer and Employee Identifiers: Includes EIN and social security numbers.

- Taxable Benefits: Reports contributions to retirement plans and non-cash benefits.

Who Typically Uses the W-2 2006 Form

The primary users of the W-2 2006 Form include employees who had taxes withheld from their wages or salaries throughout the 2006 calendar year. It is equally crucial for employers who must report employee compensation and tax withholding to the IRS and SSA. Tax professionals and financial advisors also rely on W-2 forms to provide accurate filing assistance and advice to their clients.

IRS Guidelines

The IRS provides comprehensive guidelines on filling out, issuing, and filing the W-2 Form. Employers should align with these standards to ensure accurate reporting of wage and tax information. The IRS mandates that forms be distributed to employees by January 31 following the reported year, with a filing deadline to the SSA by the last day of February if submitting by paper, or the last day of March if electronically filed.

Penalties for Non-Compliance

Failure to comply with proper filing and distribution of the W-2 2006 form can lead to financial penalties. Employers may face charges for late submissions, inaccurate statements, or not providing a form to the employee. These penalties increase with the duration of the delay and can be significant, emphasizing the need for timely and diligent compliance with IRS regulations.

Filing Deadlines / Important Dates

For the W-2 2006 Form, employers must adhere to IRS deadlines: distribute forms to employees by January 31, 2007, and file with the SSA by the end of February or March (depending on the method of submission). Meeting these deadlines ensures compliance and helps avoid any potential late-filing penalties, which can impact both the employer and employee.

Digital vs. Paper Version

While the traditional paper version of the W-2 was standard in 2006, digital advancements allow for electronic distribution and filing. Employers opting for digital versions must ensure they comply with IRS electronic submission guidelines. Digital documents benefit from easy distribution and storage, while paper forms require physical mailing and handling.

Required Documents

Preparation of the W-2 2006 Form requires access to employer payroll records, employee tax profiles, and contributions to benefits programs. Employers must track and document all relevant financial interactions accurately. Employees receiving forms should compare them to their pay stubs and financial records to ensure consistency and accuracy before filing their tax returns.