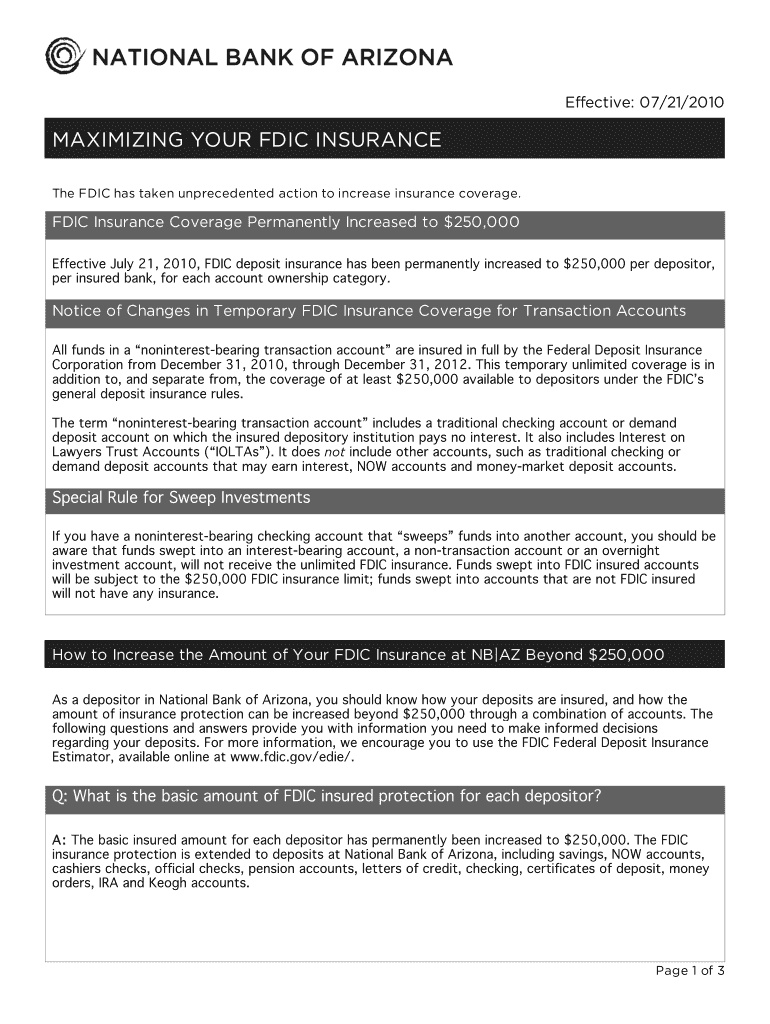

Definition and Understanding of FDIC Insurance

FDIC insurance protects depositors by insuring their deposits in member banks up to $250,000 per depositor, per insured bank, for each account ownership category. This insurance is a safety mechanism established by the Federal Deposit Insurance Corporation (FDIC) to maintain stability and public confidence in the financial system. Understanding the intricacies of how this insurance works can help individuals and families maximize their coverage beyond the standard limit, ensuring their savings remain protected in a variety of financial scenarios.

How to Maximize Your FDIC Insurance

Maximizing FDIC insurance is about strategically structuring your accounts to achieve coverage beyond the $250,000 per depositor limit. This can be accomplished by:

- Utilizing Different Ownership Categories: Each category, like single accounts, joint accounts, and retirement accounts, provides separate insurance coverage.

- Spreading Funds Across Different Banks: Since each insured bank provides separate coverage, depositing funds in different banks can increase the total insured amount.

- Creating Revocable Trust Accounts: Allocating beneficiaries in a revocable trust account can increase coverage based on the number of beneficiaries designated.

Examples of Account Structuring

Consider a family with $400,000 to deposit. By opening separate accounts under different ownership categories and at separate banks or designing trust arrangements, they can ensure full coverage for the total amount.

Steps to Optimize FDIC Coverage

- Assess Financial Situations: Inventory total deposits across all accounts.

- Identify Current Coverage Levels: Determine the existing coverage based on account types and balances.

- Reorganize Accounts: Structure accounts to utilize different ownership categories and banks.

- Consult with a Financial Advisor: Seek advice for personalized strategies to maximize coverage.

Importance of Strategic Account Management

Proper management not only aids in maximizing insurance coverage but also aligns with long-term financial planning.

Who Benefits from Maximizing FDIC Insurance

Maximizing FDIC insurance is particularly beneficial for:

- High-Net-Worth Individuals: Those with substantial deposits need coverage beyond the standard limit.

- Small Businesses: Enterprises requiring liquidity protection for operating capital.

- Trustees and Executors: Individuals managing substantial funds on behalf of others.

Legal Considerations When Maximizing FDIC Insurance

Legal considerations are vital when managing accounts for maximum insurance coverage:

- Compliance with FDIC Regulations: Ensure that account structures align with FDIC guidelines.

- Trust Agreement Clarity: Legal documents must clearly outline relationships between grantors and beneficiaries for trust accounts.

- Consultation with Legal Professionals: Legal advice ensures compliance with state and federal laws.

Important Terms Related to FDIC Insurance

- Deposit Insurance Fund (DIF): The fund that pays insured deposit claims.

- Beneficiary: Person designated to benefit from an account.

- Revocable Trust: A trust which can be altered or revoked by the grantor.

Case Studies of Effective FDIC Maximization

Real-world applications can illustrate these strategies. For instance, a retired couple might use joint accounts and trusts to enhance their coverage, ensuring their retirement savings are fully insured.

Software Tools for Managing FDIC Coverage

Certain financial software tools, like QuickBooks, may offer features to track deposits and highlight potential areas where FDIC coverage can be optimized. These tools can also assist in streamlining document management and financial planning related to FDIC insurance coverage.