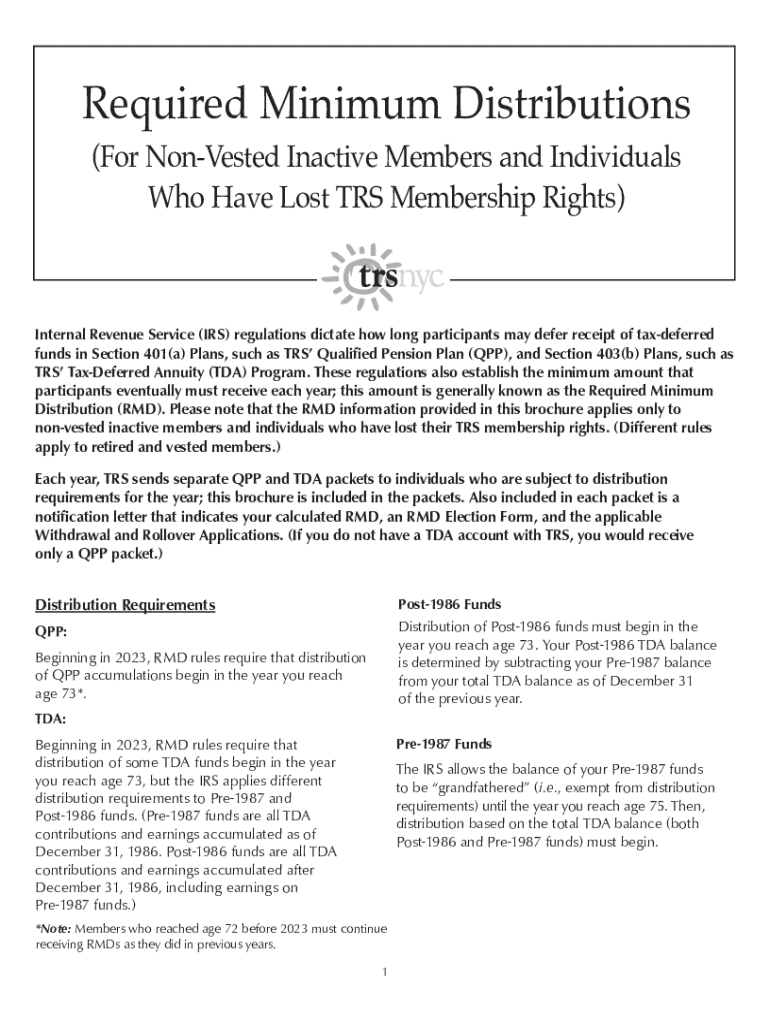

Understanding Required Minimum Distributions (RMDs)

Required Minimum Distributions (RMDs) refer to the minimum amounts that non-vested inactive members and individuals who have lost their TRS membership rights under IRS guidelines must withdraw annually from their qualified plans, such as Qualified Pension Plans (QPPs) and Tax-Deferred Annuities (TDAs). These regulations ensure the gradual depletion of tax-deferred retirement accounts to prevent indefinitely avoiding taxes. RMDs generally start at age 72, with specific calculations based on factors such as account balance and life expectancy.

Importance of RMD Compliance

Failure to comply with RMD regulations can result in substantial IRS penalties, equivalent to up to 50% of the undistributed amount. This requirement ensures orderly and timely tax revenue collection while preventing abuse of tax-favored retirement accounts. Understanding and adhering to these rules is critical to avoiding unnecessary financial setbacks and ensuring proper retirement planning.

How to Use the Required Minimum Distributions Form

To correctly utilize the RMD form, begin by gathering pertinent information regarding your retirement accounts, such as account balances and personal details. The form guides users through a series of sections to input relevant data and calculate the RMD amount. Complete each section carefully, ensuring all information aligns with IRS mandates and the specifics of your account types.

Obtaining the RMD Form

The RMD form can be obtained directly from the IRS website or through your plan administrator. Ensure you have the most current version, as modifications to IRS regulations may bring changes to form requirements and criteria. Some plan providers may offer digital versions compatible with document management platforms like DocHub, enabling easier completion and submission.

Calculating Required Minimum Distributions

RMD calculations depend on the account balance as of the prior year's end and the applicable distribution period or life expectancy factor, available from the IRS Uniform Lifetime Table. For non-vested inactive members, it's crucial to verify the specific account type and the associated rules, as some accounts may have distinct minimum distribution tables or requirements.

Filing Deadlines and Important Dates

RMDs must generally be taken by December 31 each year after reaching age 72. However, the first RMD can be delayed until April 1 of the following year. Missing these deadlines can result in penalties. Mark calendars and set reminders to ensure timely distribution, especially if you are initiating the process for the first time.

Key Terms and Definitions

Understanding the terminology related to RMDs is essential:

- Qualified Pension Plan (QPP): Employer-sponsored retirement plan offering tax advantages.

- Tax-Deferred Annuity (TDA): Investment vehicle allowing tax-deferred growth.

- Non-vested Inactive Members: Individuals with retirement accounts who are no longer accumulating benefits and do not meet vesting requirements.

IRS Guidelines

The IRS mandates RMDs to prevent indefinite tax deferral. Regulations outline specific methods for calculating distributions based on account types and provide standards for compliance. It's important to remain updated with these guidelines to ensure accurate and timely withdrawals.

Penalties for Non-Compliance

Miscalculations or failure to withdraw the RMD amount can result in a 50% excise tax on the amount that should have been withdrawn. Awareness of these penalties underscores the importance of precise adherence to RMD rules, encouraging proactive management of retirement plan distributions.

Required Documents

Gather essential documents such as statement balances for retirement accounts and personal information before initiating the RMD process. Accurate document preparation is fundamental for completing the RMD form accurately and efficiently.

Digital vs. Paper Form Options

While traditional paper forms are available, digital versions offer convenience and efficiency. Platforms like DocHub support digital signing and submission, streamlining compliance with RMD requirements. Users benefit from using digital forms due to automated calculations, digital signatures, and synchronized submissions with tax software.

Collecting Legally Binding Electronic Signatures

Utilize platforms like DocHub for collecting electronic signatures on your RMD forms. These signatures are compliant with the ESIGN Act, ensuring legality and security. Such platforms enable straightforward capture and management of signatures, enhancing the efficiency of the form submission process.

Form Submission Methods

There are multiple methods for submitting RMD forms, including online submission, mail, or in-person filing. Selection depends on individual preferences and plan administrator requirements. Online submission through secure platforms is often recommended for enhanced security and efficiency, given the sensitive nature of the information involved.

State-Specific Regulations

RMD requirements are generally consistent across the United States, but some state-specific nuances may exist, especially regarding state tax implications. Verify with local tax authorities or a financial advisor to ensure compliance with both federal and state regulations.