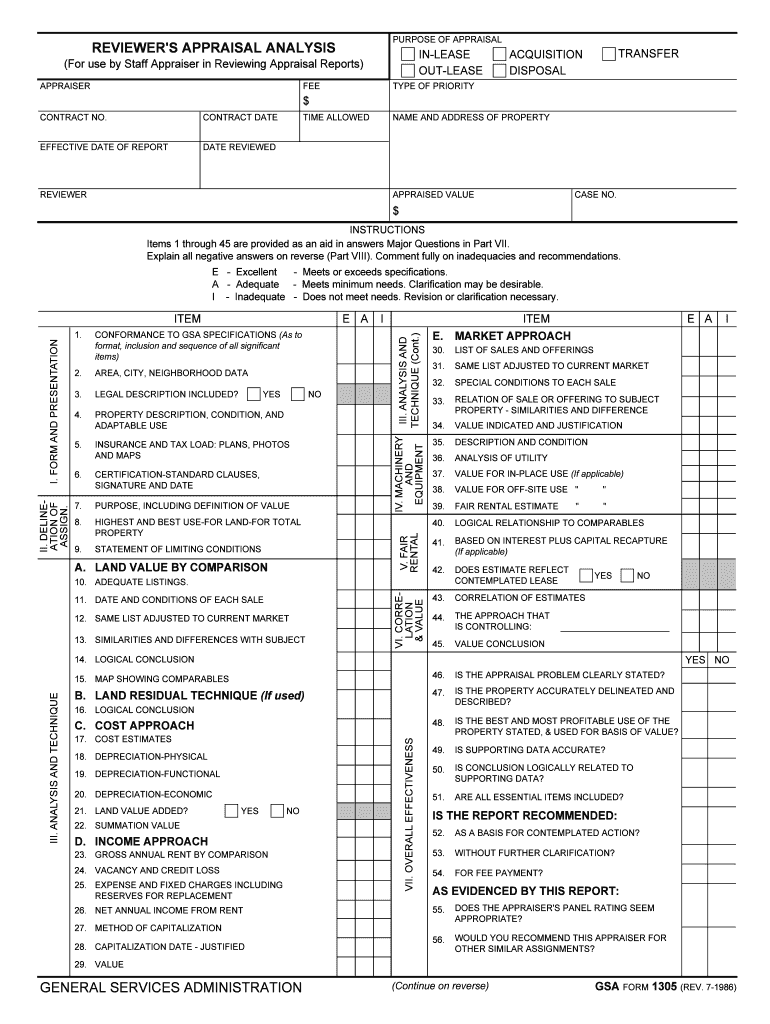

Definition and Meaning

Appraisal Review Reminders for Freddie Mac Single-Family properties serve as an essential tool for ensuring the accuracy and reliability of property appraisals. These reminders guide staff appraisers through a systematic review process, focusing on critical appraisal elements such as valuation approaches, clarity, and effectiveness. The intent is to maintain high standards for property valuation to support informed lending decisions.

Key Elements of the Appraisal Review Reminders

A comprehensive understanding of the Appraisal Review Reminders involves recognizing its core components, which include:

- Valuation Approaches: Emphasizing the market, cost, and income approaches to appraisal.

- Consistency Check: Ensuring that all data within the appraisal report is consistent and supports the final valuation.

- Risk Assessment: Identifying any potential risks or discrepancies within the appraisal that could affect lending decisions.

- Quality Assurance: Guaranteeing that the appraisal meets Freddie Mac's guidelines and standards for accuracy and completeness.

How to Use the Appraisal Review Reminders

To use the Appraisal Review Reminders effectively, appraisers should follow a structured approach:

- Initial Review: Begin with a thorough examination of the property's details and the overall report.

- Detailed Assessment: Check the valuation methods used and verify data accuracy.

- Documentation: Record any findings, inconsistencies, or areas of concern.

- Feedback: Provide actionable feedback and recommendations for improving the appraisal if needed.

Each step ensures that appraisers have a clear, methodical approach to reviewing appraisals, supporting high-quality outcomes.

Steps to Complete the Appraisal Review Reminders

Completing the Appraisal Review Reminders entails a detailed process:

- Gather Required Documents: Start by collecting all relevant property documentation and the appraisal report.

- Analyze Valuation Techniques: Delve into the techniques employed in the appraisal, ensuring they align with industry standards.

- Assess Report Clarity: Examine the report for clarity of presentation and the logical flow of information.

- Annotate Points of Concern: Use annotation tools to highlight and comment on any concerns.

- Compile a Review Summary: Develop a summary of the appraisal review, outlining both strengths and recommended improvements.

Each step is crucial for appraisers to validate both the credibility and quality of the appraisal report.

Who Typically Uses the Appraisal Review Reminders

The primary users of the Appraisal Review Reminders are:

- Appraisers: Professionals tasked with evaluating property value for lenders.

- Lending Institutions: Banks and financial entities that rely on accurate appraisals for mortgage approvals.

- Real Estate Professionals: Agents and consultants who advise clients based on property valuations.

This diverse user base underscores the reminders' application across multiple industries seeking reliable appraisal information.

Legal Use of the Appraisal Review Reminders

The Appraisal Review Reminders have specific legal purposes:

- Compliance: Ensuring adherence to Freddie Mac guidelines for property appraisals.

- Accuracy Verification: Legally documenting appraisal reviews to verify factual accuracy.

- Risk Mitigation: Documenting discrepancies mitigates risk by identifying issues preemptively, helping avoid potential legal disputes.

Legal compliance, accuracy, and risk management are crucial in the context of property and financial regulation.

Important Terms Related to Appraisal Review Reminders

Understanding relevant terminology is vital for users:

- Market Approach: A valuation technique based on the sale prices of comparable properties.

- Cost Approach: Estimating property value based on the cost of replacing it.

- Income Approach: Valuing property based on the income it can generate over time.

- Amendment: Modifications made to the original appraisal report to correct or update information.

These terms facilitate a clearer interpretation of the appraisal process and its components.

Penalties for Non-Compliance

Failing to adhere to the Appraisal Review Reminders may result in:

- Financial Penalties: Potential fines for non-compliance with Freddie Mac standards.

- Revocation of Appraiser Credentials: Risk of losing certification if guidelines are not respected.

- Legal Consequences: Appraisers may face legal actions if inaccuracies result in financial loss.

Understanding the penalties underscores the importance of complying with these appraisal reminders for all stakeholders involved.