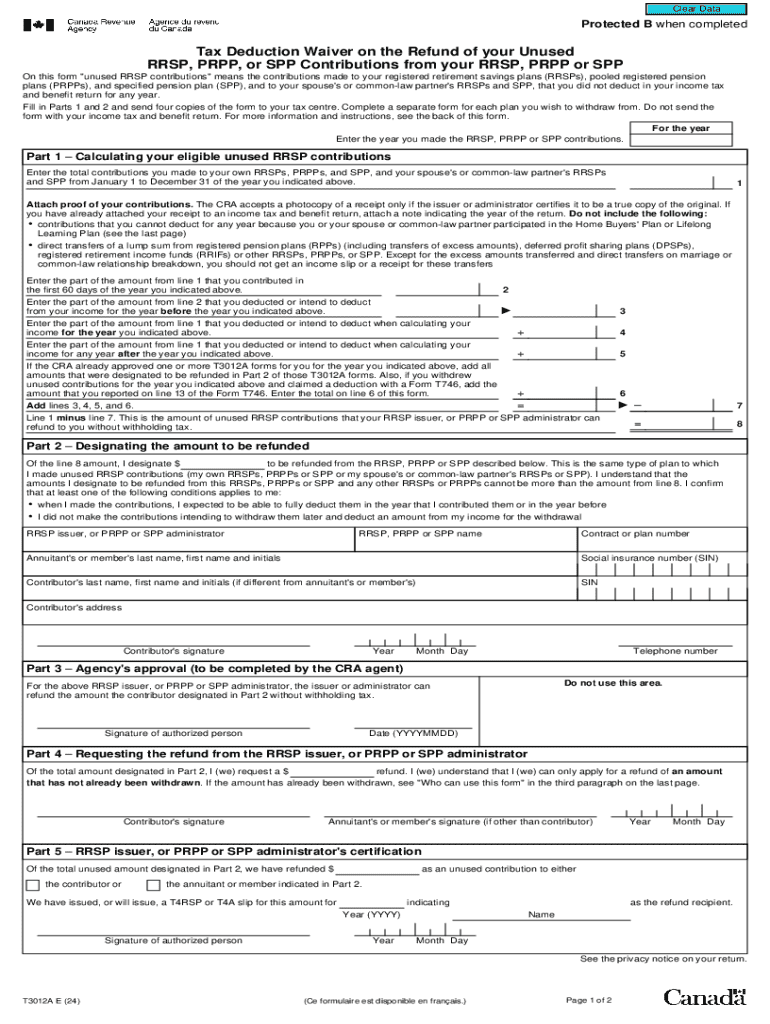

Definition and Meaning of the Tax Deduction Waiver

A "Tax Deduction Waiver" allows individuals or entities who have unused contributions in registered retirement savings plans (RRSPs), pooled registered pension plans (PRPPs), or specified pension plans (SPPs) to request a refund of these amounts without being subject to withholding taxes. These waivers serve to alleviate the immediate tax burden that typically accompanies refunds of unused contributions, ensuring taxpayers can recover their funds efficiently. Understanding the intricate criteria for such waivers is crucial for maximizing financial benefits within the regulatory framework defined by tax authorities.

Eligibility Criteria

To qualify for a tax deduction waiver, taxpayers must meet specific eligibility criteria. These often include but are not limited to:

- Verification of unused contributions within the RRSP, PRPP, or SPP accounts.

- Demonstrating that the contributions exceed annual limits or were made erroneously.

- Complying with timelines set by tax authorities for filing the waiver request. Taxpayers should carefully review these requirements to determine their eligibility and prepare the necessary documentation to support their claims.

Steps to Complete the Waiver Process

- Document Verification: Review your account statements to confirm unused contributions.

- Form Acquisition: Obtain the appropriate tax deduction waiver form from your local tax authority or online.

- Complete Required Information: Fill out personal details, contribution amounts, and other relevant financial information on the form.

- Attach Necessary Documentation: Include records and statements that substantiate your claim for a waiver.

- Submit the Form: Depending on the jurisdiction, submission methods may include online portals, mailing the form, or delivering it in-person to the tax office.

- Await Confirmation: After submission, wait for acknowledgment and approval from tax authorities.

These steps ensure thorough preparation and adherence to procedural requirements, minimizing the risk of delays or rejections.

Required Documents

Essential documentation includes:

- Recent RRSP, PRPP, or SPP account statements showing unused contributions.

- Copies of previous tax returns if reclaiming contributions from past tax years.

- Identification documents, such as a driver's license or Social Security card.

- Form confirmations of contributions made in error or exceeding annual limits.

Having a comprehensive set of documents ready facilitates a smoother application process and supports the credibility of the waiver request.

IRS Guidelines for Waivers

While tax deduction waivers are common, guidance from authorities such as the IRS provides clarity on permissible practices. The IRS offers detailed directives on how to assess eligibility, the process for refund applications without withholding implications, and compliance with federal tax laws. It is critical to consult these guidelines to ensure that the waiver submission aligns with IRS standards and avoids potential legal complications.

Application Process and Approval Time

The application process for a tax deduction waiver involves meticulous form completion and submission within specified deadlines. Approval times can vary depending on the completeness of the application and the volume of requests processed by the tax authority. Typically, decisions are communicated within several weeks but can extend to a few months during peak tax seasons. Proactively managing expectations and preparing for such timelines is advised.

Legal Use of the Waiver

A tax deduction waiver must be used within the parameters set by relevant tax legislation. Legal use entails:

- Ensuring the waiver is only applied to qualified excess contributions.

- Utilizing waivers for legitimate refund claims without tax manipulation.

- Maintaining accurate records for future tax audits or inquiries.

Understanding and adhering to these legal frameworks protects against legal pitfalls and financial penalties.

Examples of Using the Waiver

Practical examples highlight scenarios where tax deduction waivers could be beneficial:

- Scenario 1: An individual discovers excess contributions to their RRSP due to a payroll error. A waiver allows recovery of this amount without withholding tax, aligning contributions with legal limits.

- Scenario 2: A taxpayer nearing retirement reassesses their financial plan, identifying unused contributions within their PRPP. By applying for a waiver, they maximize their accessible funds in accordance with tax regulations.

These examples shed light on how waivers can be strategically employed in diverse financial circumstances to optimize tax outcomes.

Penalties for Non-Compliance

Failure to comply with tax deduction waiver regulations can result in significant penalties, such as:

- Financial fines for excess contribution violations.

- Additional taxes on unreported or improperly claimed refunds.

- Potential legal action for fraudulent waiver submissions.

Taxpayers must remain vigilant and informed about compliance obligations to avoid costly repercussions or adverse tax consequences.