Definition & Meaning

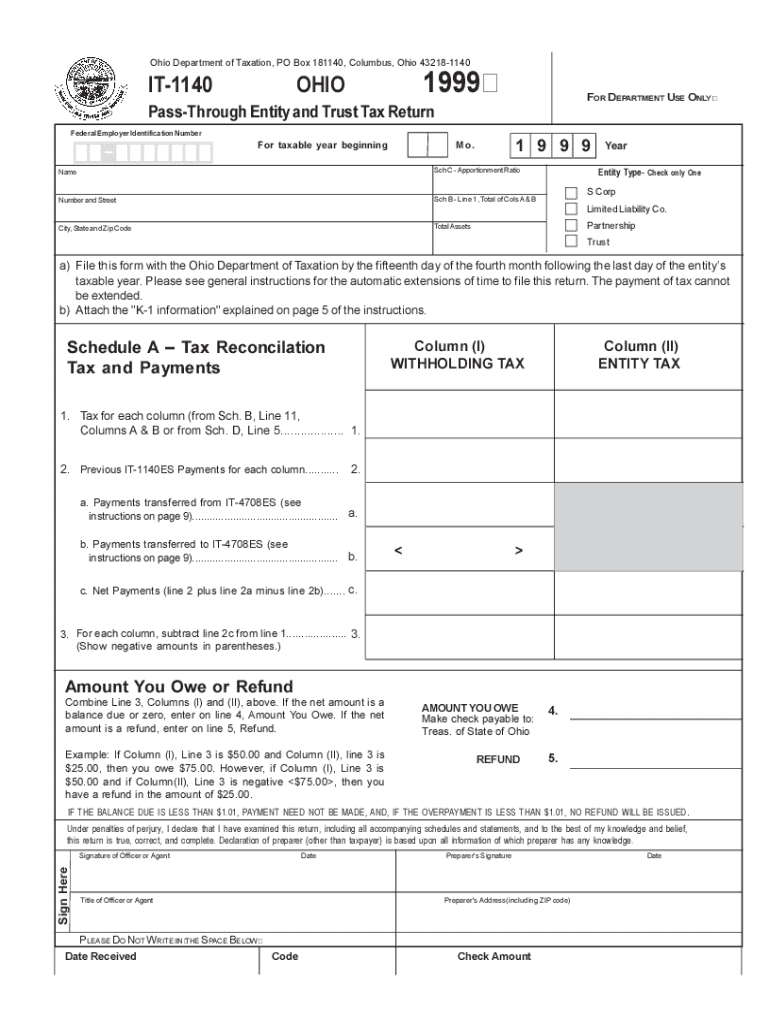

The It-1140 form, specifically for Ohio, serves as a Pass-Through Entity and Trust Tax Return. It is a tax document used to report and reconcile tax obligations for entities such as partnerships, S-corporations, and trusts that pass income to individual members or beneficiaries. Unlike corporations taxed at the entity level, these entities distribute income, and taxes are accounted for at the individual recipient level. The form encompasses detailed sections to capture income, deductions, credits, and allocate income among individual beneficiaries or members.

Steps to Complete the It-1140

-

Gather Necessary Information: Start by collecting all relevant financial documents, such as income statements, balance sheets, and records of distributions to members or beneficiaries.

-

Select Entity Type: Clearly indicate your entity type at the beginning of the form. You need to match this with the existing structure of your organization, like partnership or S-corporation.

-

Income Reporting: Include all income received by the entity. This can be from various sources like sales revenue, dividends, or interests.

-

Deduction and Credits: List all allowable deductions and any applicable credits. This helps determine the taxable income of the entity.

-

Calculate Apportionment Ratios: For entities doing business in multiple states, calculate the apportionment ratio to determine the Ohio taxable income.

-

Complete Payment Coupon: Fill out estimated tax payment coupons, if required, for future years' obligation compliance.

Who Typically Uses the It-1140

Pass-through entities, including partnerships, S-corporations, and some trusts, use the It-1140 form. These entities are defined by their structure where income is "passed through" to the individual members. Typically, owners or managers responsible for tax compliance within these organizations would be the individuals completing this form.

Filing Deadlines / Important Dates

- Regular Filing Deadline: The It-1140 must be filed by the 15th day of the fourth month following the close of the fiscal year. For calendar-year taxpayers, this would be April 15.

- Extensions: While extensions can be filed, they do not extend the time for payment of taxes owed. Timely applications for extensions are crucial to avoiding penalties.

- Estimated Tax Payments: Due dates for estimated taxes are typically on a quarterly basis.

Key Elements of the It-1140

- Entity Type Selection: Specify whether the entity is a partnership, S-corporation, or trust.

- Apportionment Ratios: Essential for entities operating in multiple states, this determines the percentage of income taxable by Ohio.

- Schedules for Tax Reconciliation: Includes schedules that help in reconciling the computed tax with the effective tax owed or refund expected.

Important Terms Related to It-1140

- Pass-Through Entity: An organization that passes income to the personal tax filings of its owners or investors.

- Apportionment Ratio: A figure used to allocate a portion of income to a particular jurisdiction.

- Trust Income: Earnings or revenue accrued to a trust, which must be detailed and reported for tax purposes.

State-Specific Rules for the It-1140

Ohio imposes specific guidelines and tax rates for pass-through entities and has unique rules regarding the apportionment of income. Regulations also include details on how to handle nonresident member taxes and specific apportioning formulas that all users must adhere to when filing.

Penalties for Non-Compliance

Failing to file the It-1140 correctly or on time can result in significant penalties. Ohio may impose late filing fees, interest on owed taxes, and potential fines for incorrect accounting or failure to appropriately report all income and deductions. Compliance is paramount to avoid financial and legal repercussions.