Definition and Purpose of Form No. 27Q

Form No. 27Q is a quarterly statement required under the Income-tax Act, specifically for reporting tax deductions on payments made to non-residents, excluding salaries. The form ensures compliance with tax regulations by providing a structured format for documenting TDS (Tax Deducted at Source) transactions. It includes sections that capture the deductor’s information, details of the tax deducted and paid to the government, and specifics about each deductee.

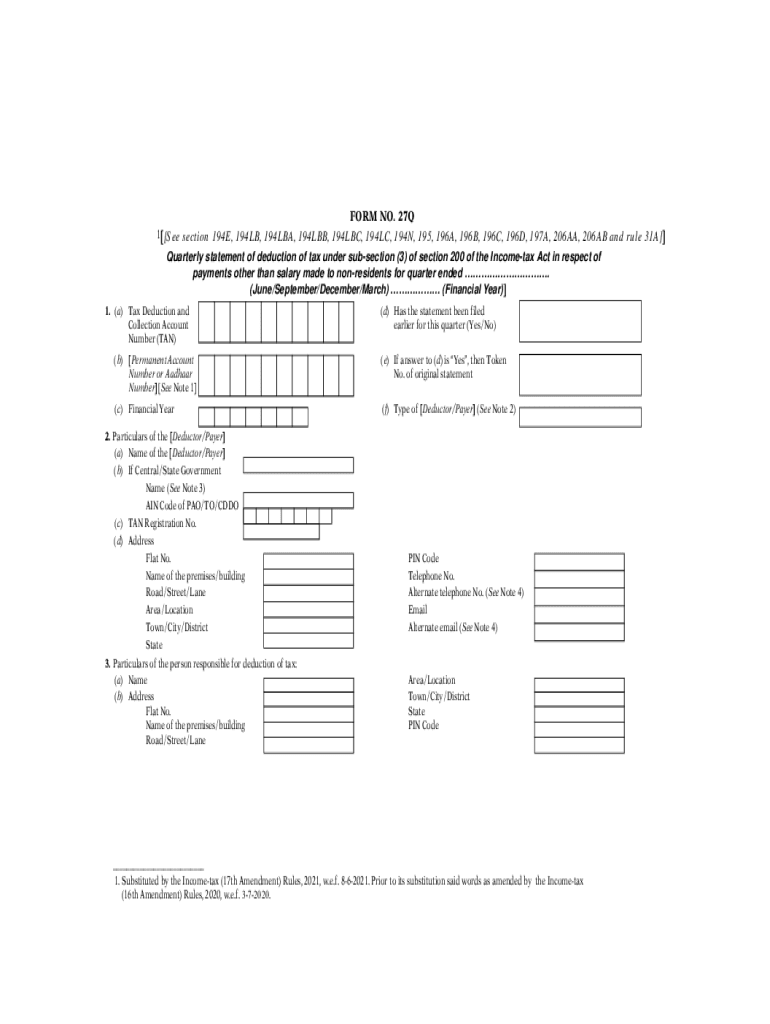

How to Use Form No. 27Q

Form No. 27Q is used to report TDS on other payments such as interest, dividend, or any other sum chargeable under the provisions of the Income-tax Act, except for salaries. The deductor needs to fill out this form on a quarterly basis, ensuring that all financial transactions involving non-residents are reported accurately to the government. Documentation must be precise to avoid discrepancies and potential penalties for non-compliance.

Steps to Complete Form No. 27Q

- Gather Required Information: Before starting, collect details about all applicable payments, tax deductors, and non-resident deductees.

- Fill Deductor Details: Enter the name, address, and PAN of the deductor in the relevant sections.

- Complete Deduction Details: For each transaction, provide the amount paid, date of payment, rate of TDS applied, and the tax deducted.

- Enter Deductee Information: List non-resident details like name, address, and PAN or tax identification number from their home country.

- Verify and Submit: Double-check all entries for accuracy and then submit the form either online or via mail, adhering to specified deadlines.

Important Terms Related to Form No. 27Q

- Deductor: The individual or entity responsible for deducting TDS on payments to non-residents.

- Deductee: Non-resident individuals or entities receiving payments subject to TDS.

- Tax Identification Number (TIN): A unique identifier required for non-residents when filing Form No. 27Q.

- TDS (Tax Deducted at Source): The amount withheld from payments made to non-resident entities.

Who Typically Uses Form No. 27Q?

Form No. 27Q is primarily used by businesses and organizations in India that engage in financial transactions with non-residents in contexts other than employment. This includes financial institutions, multinational corporations, and firms that pay interest, royalties, or other sums liable to TDS under sections such as 194E, 194LB, 194LBA, 194LBB, and 194LBC.

Legal Use and Compliance for Form No. 27Q

Compliance is essential when using Form No. 27Q, as it ensures legal recognition of the TDS process on international payments. The form is governed by various sections like 194E (payments to non-residents, athletes), 194LB (interest on infrastructure debt funds), 194LBA (distributed income of business trusts), among others. Proper adherence to all regulatory guidelines mitigates the risk of legal repercussions and penalties.

Filing Deadlines for Form No. 27Q

- Quarter 1 (April – June): Due by July 31

- Quarter 2 (July – September): Due by October 31

- Quarter 3 (October – December): Due by January 31

- Quarter 4 (January – March): Due by May 31

Meeting these deadlines is critical to avoid penalties and ensure smooth tax processing and compliance.

Penalties for Non-Compliance

Failure to file Form No. 27Q or inaccuracies within the document can result in substantial penalties. The tax authorities may impose fines, typically ranging from ₹100 per day until compliance, up to a maximum of the amount of TDS involved. Additional penalties may apply for incorrect or incomplete submissions; hence accuracy in reporting is crucial.

Required Documents for Form No. 27Q

- PAN of Deductor and Deductee: Proof of tax identification is mandatory for filing.

- Transaction Details: Comprehensive records of payments and deductions to ensure accurate reporting.

- Certificates of TDS Deductions: For validation of tax payment to authorities.

- Supporting Documentation: Any agreements or contracts related to the transaction.

Keeping these documents organized and accessible is key for a successful filing process.

Digital vs. Paper Version of Form No. 27Q

While Form No. 27Q can be submitted both online and via paper forms, the digital version has gained popularity due to its efficiency. Online submission reduces errors through validation checks and enables faster processing times. However, the paper version remains an option for simplicity or when digital access is limited. Understanding which method suits their capabilities ensures that businesses comply without complication.