Definition and Meaning of After-tax Super Contributions

After-tax super contributions refer to personal contributions made to a retirement savings account from income that has already been taxed. These contributions are typically added to superannuation funds in Australia without the contributor claiming a tax deduction. Unlike other types of contributions, after-tax contributions do not reduce taxable income since the funds are sourced from post-tax earnings. These contributions can grow the retirement fund over time, with investment earnings generally taxed at a lower rate within the fund. Understanding how after-tax contributions work is crucial for efficient retirement planning.

Key Characteristics

- Voluntary Contributions: After-tax contributions are voluntary, offering individuals more control over their retirement savings strategy.

- Tax-Free Component: Because the contributions are made from post-tax income, they form part of the tax-free component of your super when you retire.

- Contribution Cap: There are limits on the amount you can contribute in a year, labeled as non-concessional contributions, to prevent potential tax penalties.

Benefits

- Tax Benefits at Withdrawal: Funds become tax-free when withdrawn as part of a retirement income stream.

- Increased Super Balance: Higher contributions equate to a larger investment growth potential over time, benefiting from compound interest.

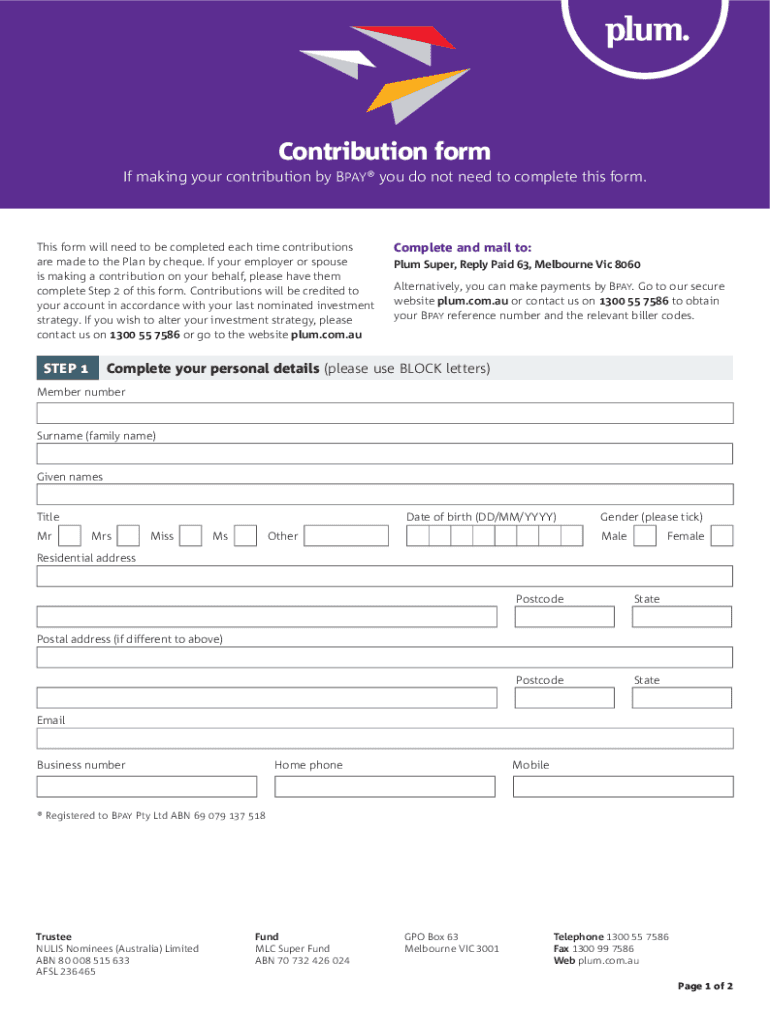

How to Use the After-tax Super Contributions Form

The form for after-tax super contributions is essential for correctly allocating funds to your super account. Here is a guideline on effectively using this form:

Steps to Utilize

- Fill in Personal Details: Start by providing accurate personal information such as full name, super fund details, and contact information.

- Specify Contribution Amount: Indicate the exact amount you wish to contribute as after-tax contributions.

- Declaration Section: Sign the declaration confirming your understanding of the superannuation rules related to after-tax contributions.

- Adherence to Contribution Limits: Cross-verify the stipulated non-concessional contribution cap to avoid exceeding limits.

Submission Methods

- By Mail: Complete and send the physical form to your super fund's provided mailing address.

- Online Portals: Many super funds offer online submission options through member portals for ease and efficiency.

How to Obtain the After-tax Super Contributions Form

Accessing the after-tax super contributions form can be straightforward. Here are methods to acquire it:

Available Sources

- Super Fund Websites: Visit the official site of your superannuation fund; the form is often available for download as a PDF.

- Customer Service: Contact your super fund directly to have the form emailed or mailed to you.

- Financial Advisors: Professional advisors can provide access or guide you on where to acquire the necessary documents.

Considerations Before Obtaining

- Membership Verification: Ensure you are a current super fund member to access and submit forms.

- Digital Access: Opt for digital forms when available to streamline the process and reduce paper usage.

Steps to Complete the After-tax Super Contributions Form

Completing the after-tax super contributions form accurately ensures correct processing. Follow these steps to fill out the form comprehensively:

- Personal Information Entry: Begin by entering your complete name, date of birth, and member number for identification.

- Contribution Details: Clearly state the contribution amount and select the type as "After-tax Contribution."

- Payment Method Selection: Choose between options like cheque or electronic transfer. Provide bank details if necessary.

- Review and Sign: Double-check all entered information for accuracy, then sign where designated, affirming the truthfulness of the details provided.

- Recheck Fund Compliance: After completing, ensure the form adheres to your respective super fund's requirements and specifications.

Final Steps

- Secure a Copy: Retain a photocopy or digital version of the completed form for personal records.

- Submission Confirmation: If submitting online, confirm submission via email acknowledgment or transaction receipt.

Why Use After-tax Super Contributions

Opting for after-tax super contributions brings distinct advantages to your retirement planning strategy:

Potential Benefits

- Tax Efficiency: Provide a tax-efficient way to increase super savings since investment income earned is taxed at concessional rates in the fund.

- Flexibility: These contributions give members flexibility in how much additional savings they choose to set aside for retirement.

- Supplementing Employer Contributions: They act as a supplement to employer contributions, substantially growing the total super balance over one's career.

Long-term Strategy

- Investment Growth: Consistent after-tax contributions can significantly boost fund size due to compound growth potential.

- Retirement Preparedness: A larger balance at retirement age ensures a more comfortable post-work financial situation.

Who Typically Uses After-tax Super Contributions

Understanding who primarily utilizes after-tax super contributions can aid in assessing its applicability to your financial context:

Common User Groups

- Higher Income Earners: Individuals who have reached or exceeded other concessionary caps often use after-tax options to increase their retirement savings.

- Self-employed Individuals: Often rely on personal contributions, including after-tax contributions, due to the lack of employer contributions.

- Retirees or Near-retirees: Those transitioning to retirement who wish to boost their fund balance may use after-tax contributions as a strategic top-up.

Target Demographics

- Professionals with Variable Incomes: Those with fluctuating income patterns, such as freelancers or contract workers, may use after-tax contributions during high earning periods.

Legal Use of After-tax Super Contributions

Legal considerations when making after-tax super contributions are crucial to avoid penalties:

Compliance with Regulations

- Contribution Caps: Adhere to annual non-concessional contribution limits to prevent attracting excess contribution taxes.

- Age Restrictions: Be mindful of age caps and work test requirements if applicable, particularly for those over sixty-seven.

- Declaration of Intent: Include any necessary declarations if intending to claim contributions as personal deductible contributions later.

Penalties and Monitoring

- Exceeding Caps: Tax penalties apply for contributions exceeding the cap; therefore, strict adherence to limits is advisable.

- Record-keeping: Retain documents for potential auditing or to verify compliance with superannuation laws.

Examples of Using After-tax Super Contributions

Practical examples provide context for using after-tax super contributions for various financial strategies.

Case Scenarios

- Scenario One: An individual making consistent annual $5,000 contributions after-tax, ultimately increasing their super balance significantly by retirement through compound interest.

- Scenario Two: A high-income earner contributing the maximum allowable after-tax each year to enhance their super fund balance beyond employer contributions.

Diverse Applications

- Property Sale Proceeds: Using proceeds from major asset sales to make lump sum contributions to a super fund after-tax.

- Bonuses and Windfalls: Allocating bonuses or financial windfalls as after-tax contributions for long-term benefits.