Definition & Meaning

Form 8379, known as the Injured Spouse Allocation, is a specific tax document issued by the IRS. It allows a spouse to claim their portion of a joint tax refund that might otherwise be used to offset a partner's past-due financial obligations. These obligations may include debts like unpaid child support, federal student loans, or other federal debt. The term "injured spouse" refers to the taxpayer in a marriage who does not owe these debts but risks losing part of their refund due to their partner's liabilities.

How to Use the 2 Form

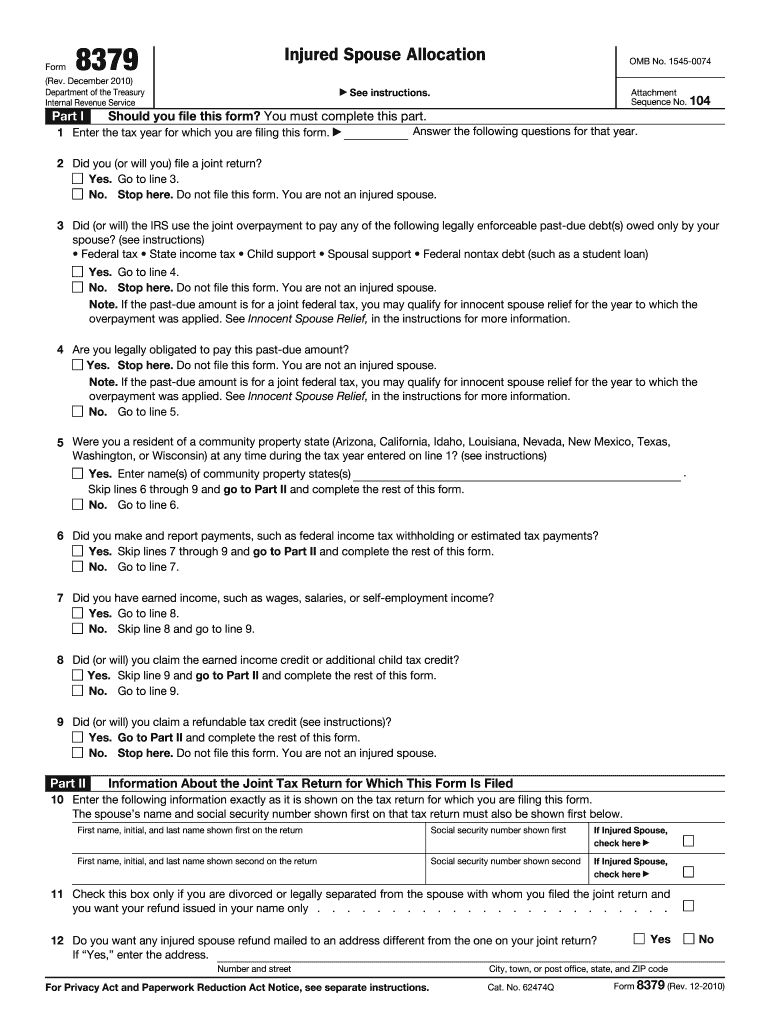

To utilize Form 8379 effectively, it's crucial to determine if you qualify as an injured spouse. You should file this form when filing a joint tax return with a spouse who has past-due debts that might result in the IRS withholding part or all of your refund. Completing the form accurately ensures you can recover the portion of the refund you are entitled to, based on your income and tax payments.

Steps for Using the Form

- Assess Eligibility: Confirm that your refund is at risk due to your spouse's debts.

- Gather Information: Collect details about each spouse's income, deductions, and withholdings.

- Complete the Form: Enter your personal information and answer all eligibility questions.

- Submit with Tax Return: Either attach Form 8379 with your joint return or submit it separately if you have already filed.

How to Obtain the 2 Form

Obtaining Form 8379 is straightforward. It can be downloaded from the official IRS website for free. Alternatively, if you require a paper version, it can be ordered through various tax preparation software like TurboTax or directly from IRS assistance centers. Ensure that you are using the form designated for the correct tax year to prevent processing delays.

Steps to Complete the 2 Form

Completing Form 8379 involves several specific steps:

- Personal Information: Fill in your name, Social Security number, and tax year.

- Income Allocation: Allocate income and withholding amounts between you and your spouse.

- Expenses and Credits: Divide applicable deductions and credits.

- Sign and Date: Ensure both spouses sign if the document is submitted after the initial joint filing.

Tips for Accurate Completion

- Double-check calculations to ensure each spouse's income and deductions are correctly allocated.

- Use precise figures from tax documents to avoid discrepancies that could lead to processing delays.

Required Documents

When completing Form 8379, access to specific documents is necessary to ensure accuracy:

- Previous Tax Returns: For reference and comparison.

- W-2 Forms: To verify income amounts.

- 1099 Forms: If applicable, for additional income sources.

- Proof of Withholdings: Such as pay stubs or end-of-year statements.

Having these documents on hand will facilitate the accurate allocation of income, deductions, and credits.

Filing Deadlines / Important Dates

The Injured Spouse Allocation can be submitted with your joint tax return. However, if applying after filing, you must do so as soon as possible to expedite the process. There is a three-year statute of limitations from the original return due date or within two years from when the tax was paid, whichever later, to file Form 8379. It's crucial to adhere to these deadlines to avoid missing out on any refund allocations you are entitled to.

IRS Guidelines

The IRS provides clear guidance for when and how to submit Form 8379:

- Timely Filing: Submit concurrently with your joint tax return for prompt processing.

- Separate Submission: Allowed if the need is identified post-filing.

- Completeness: Incomplete forms can lead to processing delays.

Penalties for Non-Compliance

While Form 8379 itself does not incur penalties for non-compliance, failing to file could lead to the loss of potential refunds due to undistributed injured spouse allocations. Timely and accurate filing is essential to ensure you receive all benefits entitled to you.

Examples of Using the 2 Form

Consider a joint return scenario where one spouse owes past-due student loans. By submitting Form 8379, the other spouse, who bears no responsibility for this debt, can claim their rightful portion of the tax refund without it being applied to their partner's debt.

Scenario Breakdown

- Spouse A: Owes $5,000 in delinquent student loans.

- Spouse B: No past-due debts, contributes $3,000 annually in tax withholdings.

- Outcome: By filing Form 8379, Spouse B can reclaim their $3,000 share of a joint refund before any debt recovery actions affect it.