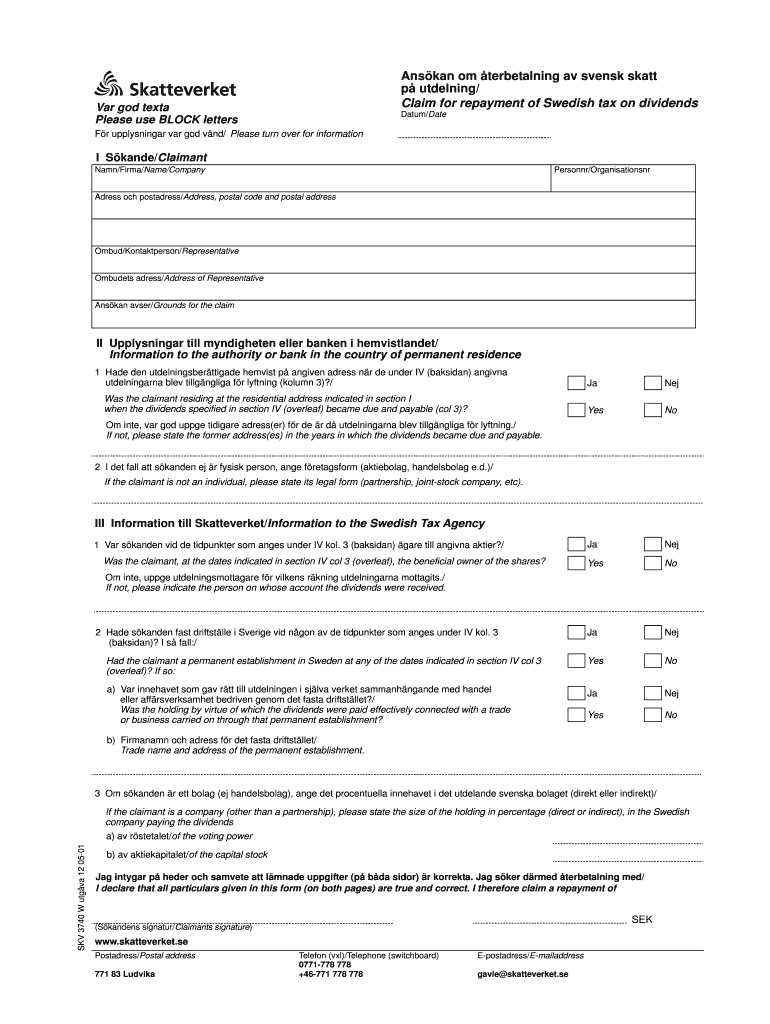

Definition and Meaning of SKV 3740

"SKV 3740" is a specialized tax form used in Sweden for claiming the repayment of taxes on dividends received from Swedish companies. The form requires detailed information from the claimant to facilitate a claim for a refund of excess tax paid on dividends, typically due to the differences between Swedish tax rates and those of the claimant's country of residence. The document ensures compliance with international tax treaties and provides a structured approach for reclaiming overpaid taxes.

How to Use the SKV 3740 Form

Using the SKV 3740 form involves several steps that are crucial to ensure a successful claim for tax repayment. Here’s a step-by-step breakdown of how to use it effectively:

-

Gather Necessary Information:

- Collect all relevant details about your dividends, including the amount received, the dates of receipt, and the Swedish tax withheld.

- Secure documentation of your residency status and tax identification number.

-

Complete the Form:

- Fill out personal details, company information, and tax residency.

- Ensure accuracy in the dividend details section to avoid discrepancies that could delay processing.

-

Attach Supporting Documents:

- Include a certificate of residence to prove your tax domicile outside Sweden.

- Attach documentation of the dividends received and taxes withheld.

-

Review and Confirm Details:

- Carefully review the completed form to check for completeness and accuracy.

- Correct any errors to prevent delays in processing.

-

Submission:

- Submit the form to the Swedish Tax Agency within the required time frame, often within five years from the dividend payment date.

How to Obtain the SKV 3740 Form

Acquiring the SKV 3740 form is a straightforward process that can be completed through various channels:

-

Online Access:

- Visit the official Swedish Tax Agency website and download the SKV 3740 form.

- Ensure you access the most recent version to avoid using outdated guidelines.

-

Physical Copies:

- Request a paper copy from the Swedish Tax Agency by contacting them directly.

-

Assistance from Financial Advisors:

- Financial advisors familiar with international tax matters can often provide the form and offer assistance in completing it correctly.

Steps to Complete the SKV 3740 Form

To complete the SKV 3740 form thoroughly, follow these steps:

-

Identify the Payer:

- Clearly state the name and address of the company or financial institution that paid the dividend.

-

Enter Your Details:

- Provide your full name, address, and country of residence.

- Include your tax identification number.

-

Detail Dividend Information:

- List each dividend payment with the source, date, gross amount, and Swedish tax withheld.

- Use additional pages if necessary to document all transactions.

-

Confirm Residency Status:

- Attach the certificate of residence issued by your local tax authority.

-

Sign and Date:

- Ensure the form is signed and dated before submission.

- Retain a copy for your records in case of queries from the tax authorities.

Who Typically Uses the SKV 3740

The SKV 3740 form is most commonly used by non-resident individuals and entities who receive dividends from Swedish sources. This includes:

-

International Investors:

- Individuals residing outside Sweden investing in Swedish companies seeking to recover withheld taxes.

-

Foreign Corporations:

- Companies based outside Sweden with investments in Swedish subsidiaries or assets.

-

Pension Funds and Trusts:

- Entities often granted tax exemptions or lower rates under bilateral tax treaties.

-

Financial Institutions:

- Banks and investment firms managing international portfolios engaging in cross-border dividend transactions.

Important Terms Related to SKV 3740

Understanding specific terms within the SKV 3740 context is vital for accurate completion:

-

Dividend:

- A distribution of profits by a corporation to its shareholders, taxed at source in Sweden for non-residents.

-

Tax Credit:

- A provision allowing foreign tax paid to be offset against tax payable in the taxpayer's country of residence.

-

Certificate of Residence:

- An official document confirming an individual's or entity's fiscal residence to support a claim under international tax treaties.

-

Withholding Tax:

- The tax retained by the payer on dividend payments made to non-residents, usually deductible against subsequent tax liabilities.

Legal Use of the SKV 3740

Filing the SKV 3740 form must be done with legal accuracy to ensure compliance with Swedish tax laws:

-

Compliance with Tax Treaties:

- Ensures claims align with double taxation agreements between Sweden and the claimant's country.

-

Documentation Requirements:

- Legal obligation to provide supporting documentation, validating claims for tax repayment.

-

Ethical Considerations:

- Accurate and truthful filing to avoid penalties or legal issues associated with fraudulent claims.

Required Documents for SKV 3740 Submission

The submission of the SKV 3740 form requires specific documentation to support the claim:

-

Certificate of Residence:

- Issued by your local tax authority, confirming your status as a non-resident.

-

Dividend Statements:

- Documentation from the payer detailing each dividend payment and tax withheld.

-

Identity Verification:

- Copies of identity documents to confirm the claimant’s identity and tax residency.

Preparing these documents accurately reduces processing times and increases the likelihood of a successful tax repayment claim.