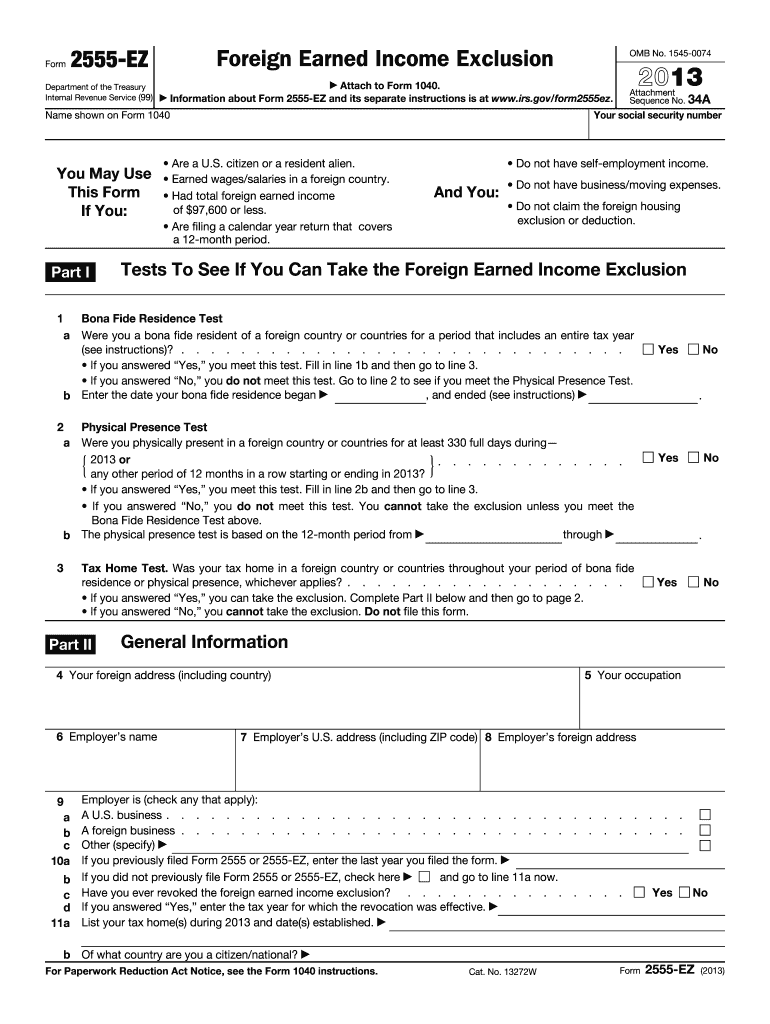

Definition & Purpose of Form 2555-EZ

Form 2555-EZ is used by U.S. citizens or resident aliens to claim the Foreign Earned Income Exclusion, simplifying the process of excluding income earned abroad from taxable income. This form applies to individuals with foreign earned income of $97,600 or less, having no self-employment income, and meeting specific residency or physical presence tests. It is crucial for optimizing tax obligations when living and working overseas.

Key Aspects:

- Foreign Earned Income: Specifically targets income earned in a foreign country.

- Eligibility: Simplified compared to Form 2555; excludes those with self-employment income.

- Residency Tests: Requires either the Bona Fide Residence Test or the Physical Presence Test for eligibility.

- Income Limit: Applicable if foreign earned income does not exceed the set threshold.

How to Obtain the Form 2555-EZ

Acquiring the Form 2555-EZ is a straightforward process. It is available for download on the official IRS website, ensuring easy access for taxpayers globally. Additionally, most tax preparation software supports this form, allowing direct integration during the tax filing process.

Download Options:

- IRS Website: Available in PDF format under IRS forms and publications.

- Tax Software Integration: Many platforms like TurboTax provide automated links to the form during tax preparation.

Steps to Complete the Form 2555-EZ

Completing the Form 2555-EZ involves a series of methodical steps to ensure accuracy in tax filings. While simplified compared to its counterpart, Form 2555, it requires precise information to validate foreign income exclusion.

-

Part I - General Information: Enter personal information, such as your name, Social Security number, and address.

-

Part II - Foreign Earned Income Exclusion: Detail the foreign country where income was earned and specify the nature of your employment.

-

Part III - Bona Fide Residence Test or Physical Presence Test: Indicate which test applies, providing dates of foreign residence or presence to confirm eligibility.

-

Part IV - Income Exclusion Calculation: Calculate the amount of foreign income eligible for exclusion.

- Review and Submit: Validate all information and ensure signatures where applicable before submission.

Important Terms Related to Form 2555-EZ

Understanding the terminology associated with Form 2555-EZ is crucial for accurate completion. Key terms have specific implications and dictate eligibility for the foreign earned income exclusion.

Essential Terms:

- Foreign Earned Income: Wages or salaries earned abroad.

- Bona Fide Residence Test: A test confirming permanent, full-time residence in a foreign country.

- Physical Presence Test: Involving proof of physical presence in a foreign country for at least 330 full days during a 12-month period.

Legal Use of the Form 2555-EZ

The Form 2555-EZ serves a legal function for taxpayers, allowing for the legitimate exclusion of foreign earned income, thereby ensuring compliance with U.S. tax regulations. Misuse, or incorrect filing could lead to penalties.

Compliance Guidelines:

- Accuracy: Ensure accurate representation of foreign income and residency status.

- Documentation: Retain supporting evidence, like foreign residency proof, for IRS verification.

Eligibility Criteria

Eligibility for Form 2555-EZ is contingent on meeting specific residency tests and income thresholds, simplifying the tax filing process for eligible individuals. This section elaborates on who qualifies to file this form.

Criteria Include:

- Income Threshold: Total foreign earned income of $97,600 or less.

- Residency: Must fulfill either the Bona Fide Residence or Physical Presence Test.

- Exclusivity: Cannot have self-employment income or claim housing exclusions/deductions.

Examples of Using the Form 2555-EZ

Real-world scenarios demonstrate the practical application of Form 2555-EZ, offering clarity for potential filers. These examples showcase different taxpayer situations in which the form can be utilized.

Scenarios:

- Corporate Employee Abroad: A U.S. citizen employed by an international company meeting residency tests and income limits.

- Government Employees: Expatriates with earnings from governmental bodies that fit within eligibility parameters.

Filing Deadlines / Important Dates

Understanding the timelines is important for taxpayers using Form 2555-EZ. Filing must coincide with federal tax deadlines unless extensions are granted.

Key Dates:

- General Filing Deadline: April 15, unless it falls on a weekend or holiday.

- Extensions: Automatic two-month extensions are available to those living outside the U.S.

- Late Filing: Incurs penalties unless an approved extension is in place, corroborated with necessary documentation.