Key Elements of the Form 6765 (Rev December 2024) Credit for Increasing Research Activities

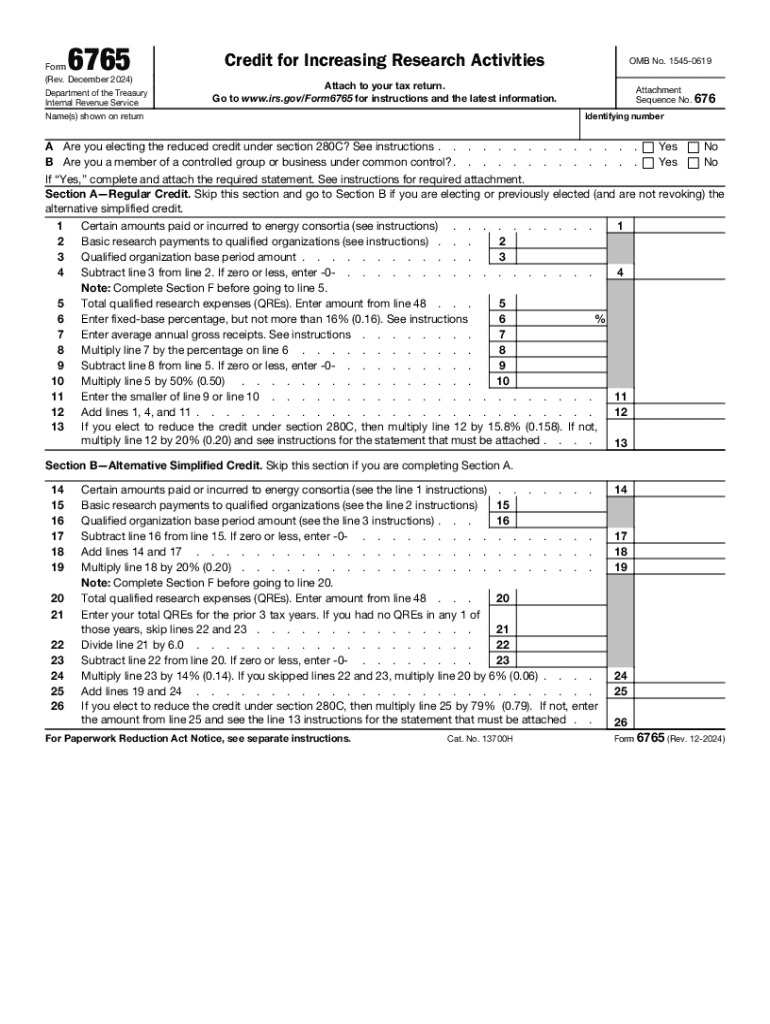

Form 6765 is essential for businesses claiming the Credit for Increasing Research Activities. This form helps taxpayers calculate two main types of tax credits: the Regular Credit and the Alternative Simplified Credit. Understanding the key elements is crucial for accurate claiming and compliance.

-

Regular Credit and Alternative Simplified Credit: This form guides claimants through calculating both types of credits. The Regular Credit is calculated based on the increase in qualified research expenses (QREs) compared to a base amount, while the Alternative Simplified Credit is determined based on a percentage of QREs over a fixed-base percentage outlined within the form.

-

Qualified Research Expenses (QREs): These include wages for employees directly involved in research activities, supply costs, and a portion of contract research expenses. Accurately documenting QREs is fundamental for maximizing credit claims.

-

Payroll Tax Election for Small Businesses: Businesses eligible under defined criteria may choose to apply a portion of the research credit against their payroll tax liability, which can be a beneficial option for start-ups and small enterprises.

How to Use the Form 6765 (Rev December 2024)

Form 6765 can be complex, requiring precise calculations and comprehensive documentation. To use it effectively, follow a structured approach:

-

Gather Necessary Information: Collect all relevant financial documents, including payroll records, supply cost invoices, and contract agreements related to research activities.

-

Determine Qualified Research Activities: Ensure your activities meet the IRS definition of research, including the four-part test focused on technological activities aimed at developing new or improved business components.

-

Complete Calculations for Credit: Use the form to compute your Regular and Alternative Simplified Credits, choosing the most beneficial method.

-

Review & Attach Supporting Documentation: Double-check figures and attach required documents as evidence for your claims to avoid processing delays or denials.

Steps to Complete the Form 6765

Completing Form 6765 requires attention to detail and careful adherence to the guidelines set by the IRS. Follow these comprehensive steps:

-

Identify Qualified Research Activities: Evaluate your activities against IRS guidelines to confirm eligibility.

-

Calculate Base Amount and Incremental Expenses: Calculate the base period expenses and determine the incremental increase to compute the tax credit.

-

Fill Out Sections on QREs: Accurately complete sections detailing wages, supplies, and contract research costs.

-

Choose Credit Computation Method: Decide between Regular Credit and Alternative Simplified Credit based on your calculations.

-

Complete Form Details: Fill in general information, including business name, taxpayer identification number, and other particulars.

-

Attach Necessary Attachments: Ensure the inclusion of supporting documentation that underlines your credit claims.

Who Typically Uses Form 6765

Form 6765 is used by a variety of business entities engaging in qualified research activities. Understanding who benefits from using this form can guide its application.

-

Corporations and Small Businesses: Companies actively involved in research and development (R&D) projects utilize this form to reduce taxable income.

-

Partnerships and LLCs: These entities commonly use Form 6765 when their operations involve technological development or experimental breakthrough activities that meet IRS stipulations.

-

Start-Ups: Smaller businesses can particularly benefit from the payroll tax offset provided for under the form, allowing them to focus funds back into R&D efforts.

Eligibility Criteria for Form 6765

Eligibility to claim the Credit for Increasing Research Activities using Form 6765 involves stringent criteria:

-

Qualified Research Activities: Activities must be intended for the development of a new or improved business component and should involve a process of experimentation.

-

Documented Expenses: The claimant must provide comprehensive documentation demonstrating qualified research expenditures.

-

Business Size and Type: Certain tax offsets available through Form 6765 are specific to small businesses or start-ups, making size criteria relevant.

IRS Guidelines for the Credit for Increasing Research Activities

The IRS provides specific guidelines for taxpayers looking to claim the Credit for Increasing Research Activities using Form 6765. Adhering to these guidelines is vital for compliance:

-

Documentation and Substantiation: Maintain thorough records of all expenses classified as QREs, underpinning your claimed tax credit amount.

-

Four-Part Test for Research Activities: Engage in activities satisfying the IRS's tests related to advancing technological knowledge and applying principles of science.

-

Avoid Disallowed Activities: Administrative tasks, routine data collection, and similar activities are not deemed eligible.

Penalties for Non-Compliance with Form 6765

Failure to accurately complete and file Form 6765 can result in significant penalties. Ensure compliance by understanding the repercussions of non-adherence:

-

Underpayment of Taxes: Incorrect assessments can lead to underpayments, attracting interest and penalties from the IRS.

-

Inaccurate Claims: Misrepresenting research expenses or failing to substantiate claims can lead to audits and the repayment of disallowed credits.

-

Negligence Penalties: Persistent inaccuracies or failure to provide requested documents may result in negligence penalties.

Application Process and Approval Time for the Credit

Understanding the application process and expected timelines can help in planning and ensuring a smooth filing experience:

-

Submission Methods: Form 6765 can be submitted either electronically or through traditional mail filings. Each method has its own timelines and processing speeds.

-

Processing Time: Generally, the IRS may take several weeks to several months to review and process credit claims depending on their complexity and the volume of claims being expediently processed.

-

Follow-Up and Contact: It's advisable to check the status of your credit claim and communicate with the IRS as necessary to address any potential issues promptly.

Digital vs. Paper Version of Form 6765

Taxpayers have the option to use either the digital or paper version of Form 6765. Each has its own benefits and considerations:

-

Digital Filing: Offers convenience and faster processing. Digital submissions often facilitate automatic calculations, reducing errors.

-

Paper Submission: While traditional, it may be necessary for those without reliable internet access or who prefer physical documentation.

In detailed crafting of Form 6765, taxpayers can ensure their claims are accurate, compliant, and timely, thereby maximizing their benefit from research activities.