Definition and Meaning

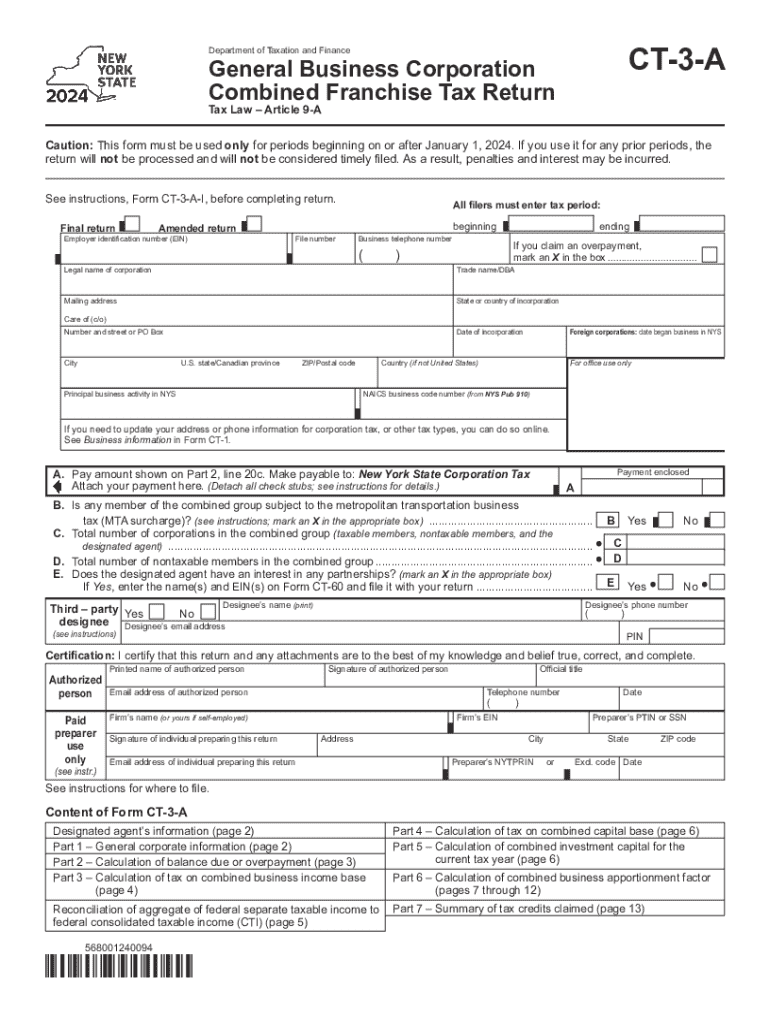

The Form CT-3-A is a Combined Franchise Tax Return specifically designed for General Business Corporations operating within the state of New York. This form is utilized for tax periods beginning on or after January 1, 2024. It mandates corporations to report their income, deductions, and tax liabilities accurately. It includes essential sections that cover general corporate information, calculations of both business income and capital taxes, as well as apportionment factors and any tax credits claimed. Compliance with this form is crucial as it ensures that corporations are adhering to New York State's tax regulations and avoiding potential penalties.

How to Use the Form CT-3-A

To effectively utilize Form CT-3-A, corporations should start by gathering all necessary financial data for the tax year in question. The process involves meticulously entering corporate income and deductions, which serve as the foundation for calculating tax liabilities. Important sections on this form also require the listing of any applicable tax credits that can reduce the overall tax burden. Additionally, corporations must provide details on apportionment factors, which determine the portion of the business's income taxable in the state of New York. The form serves as a comprehensive tool for tax reporting and compliance, ensuring that all financial activities are accurately reflected.

- Gather all pertinent financial documents.

- Accurately input income and deduction information.

- List relevant tax credits and apportionment data.

- Double-check all entries for accuracy to avoid filing errors.

Steps to Complete the Form CT-3-A

Completing the Form CT-3-A involves a detailed and structured approach. Adhering to the following process can streamline the completion:

- Collect Financial Statements: Gather comprehensive financial records covering the reporting year.

- Fill Out Corporate Information: Enter details such as corporate name, address, and federal employer identification number.

- Calculate Net Income: Determine total revenue and subtract allowable deductions.

- Identify Apportionment Factors: Calculate factors that apply to income generated within New York.

- Apply Tax Credits: Enter any tax credits your corporation is eligible for.

- Complete Tax Payment Section: Calculate the total tax due and ensure payment is prepared.

- Review and Sign: Verify all information for accuracy, then sign the form to certify its correctness.

Important Terms Related to Form CT-3-A

Understanding certain key terms is crucial while dealing with the Form CT-3-A:

- Apportionment Factors: Ratios used to determine the proportion of income subject to state taxation.

- Tax Credits: Deductions from tax liability accepted under specific conditions to encourage certain types of business activities.

- Net Income: The profit calculated after deducting all expenses from the total revenue for the period.

- Franchise Tax: A tax levied on corporations for the privilege of doing business in a state, based on income or capital.

State-Specific Rules for the Form CT-3-A

New York State imposes specific criteria and rules that govern the use of Form CT-3-A. Corporations must be aware of these regulations to ensure compliance:

- New York businesses must use apportionment formulas when operating within and across state lines.

- New York State requires reporting of receipts and expense allocations to ensure accurate tax liability assessments.

- Corporations must maintain detailed records that support figures reported on Form CT-3-A.

Filing Deadlines and Important Dates

Timely filing of the Form CT-3-A is imperative to avoid penalties:

- Filing Deadline: Typically due by March 15th of the year following the reporting period.

- Extension Requests: Corporations can file for an extension if additional time is needed, but this does not defer payment obligations.

- Estimated Payment Dates: Quarterly estimated tax payments must be made to avoid penalties for underpayment.

Penalties for Non-Compliance

Failure to comply with the filing and payment requirements associated with Form CT-3-A can result in:

- Late Filing Penalties: Charges incurred for submitting the form past the due date.

- Underpayment Penalties: Fees assessed if estimated taxes are significantly underpaid.

- Interest on Unpaid Taxes: Additional charges on any remaining unpaid tax balance.

Corporations should ensure accurate and timely submissions to mitigate these risks.

Eligibility Criteria for Using Form CT-3-A

The Form CT-3-A is designated for specific corporate entities, including:

- Corporations that are part of a combined group must file jointly.

- Businesses operating in New York State that meet particular thresholds defined by state law.

- Companies engaged in interstate commerce that require apportionment of income.

Understanding eligibility is essential to determine the correct suite of tax forms for any given business.