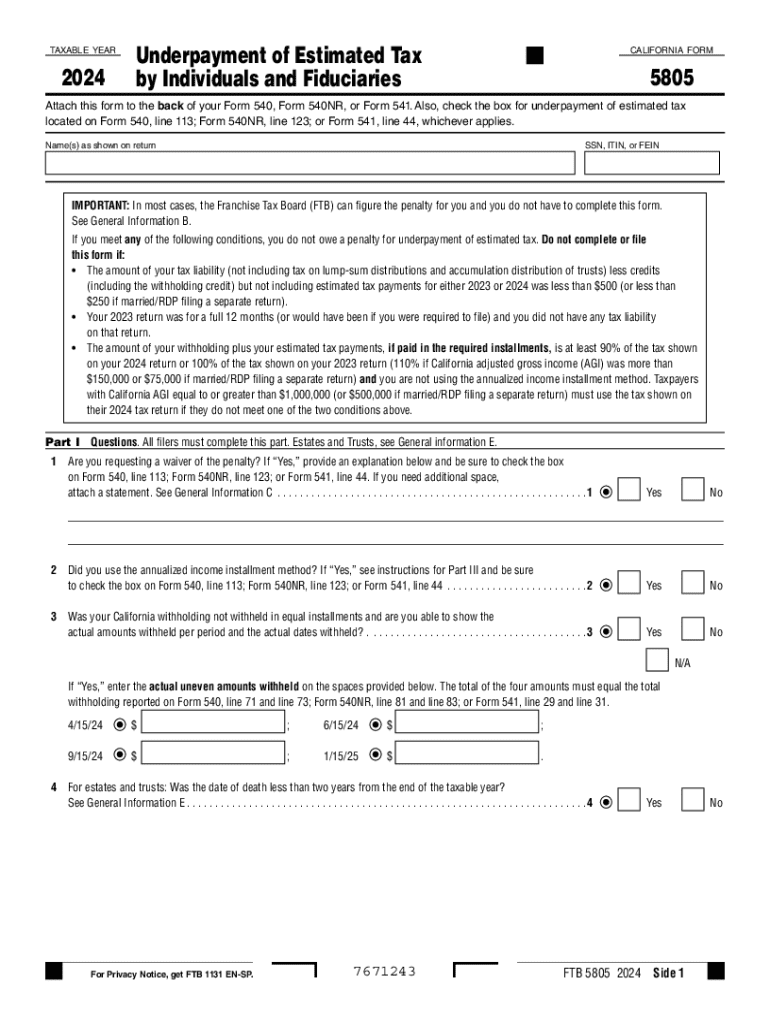

Definition and Purpose of Form 5805

The 2024 California Form 5805 addresses the underpayment of estimated tax by individuals and fiduciaries. Individuals and fiduciaries must use this form to calculate and report any underpayment of their estimated taxes. It provides instructions on how taxpayers might qualify for exemptions or reduced penalties if they did not pay enough in estimated taxes throughout the year. The form systematically guides you through calculating your required annual payment and penalties for any underpayment. It is an essential tool to ensure compliance with tax laws and to minimize unnecessary penalties.

Steps to Complete Form 5805

-

Gather Required Documents: Start by collecting all necessary income documents, such as W-2s, 1099s, and any other records that provide details of income received since they are essential for accurate calculation.

-

Calculate Estimated Tax: The form provides sections for estimating the total tax liability. This involves compiling your income, deductions, and credits to determine the amount you should have paid.

-

Enter Payment Data: Fill in details of any tax payments made, particularly estimated payments done throughout the year ensuring they are accurately recorded for comparison against the estimated tax.

-

Calculate Underpayment and Related Penalties: Use the provided worksheets in the form to compare what you paid against what you should have paid. The form permits detailed calculation of any penalties due, using either the annualized income method or regular installments.

-

Check Eligibility for Waivers: The form allows taxpayers to apply for waivers under certain conditions. Review these provisions to determine eligibility.

-

Finalize and Submit: After completing the necessary sections, review the form for accuracy before submission. Errors or omissions can lead to delays or additional penalties.

Who Typically Uses Form 5805

Form 5805 is commonly used by:

- Self-Employed Individuals: Those who must pay estimated taxes throughout the year because they do not have withholdings from an employer.

- Retirees: Individuals receiving pensions or retirement income who might not have sufficient withholdings.

- Investors: Taxpayers with significant income from dividends, interest, or capital gains.

- Fiduciaries: Executives or trustees managing estates or trusts that involve significant tax handling.

Key Elements of Form 5805

- Estimated Tax Calculation: Core tables and worksheets for computing your total estimated tax liability based on your expected income.

- Payment Tracking: Detailed sections for entering previously made estimated tax payments.

- Underpayment Calculation: Illustrated steps and formulae for computing any amount that remains unpaid.

- Penalty Conditions: Taxpayer-friendly breakdowns of threshold calculations determining when penalties apply.

- Waiver Eligibility: Sections explaining the conditions under which you may apply for underpayment penalty waivers with the necessary documentation.

Important Terms Related to Form 5805

- Estimated Tax: An approximation of taxes a taxpayer expects to owe on income that is not subject to withholding.

- Fiduciary: An entity responsible for managing assets for another party, often in the context of a trust or estate.

- Annualized Income Installment Method: A calculation approach used to align estimated payments with income received during different periods of the year to avoid penalties.

- Safe Harbor Rule: A tax regulation that avoids penalties if taxpayers pay the smaller amount between their previous year's tax or 90% of the current year's tax.

State-Specific Rules for Form 5805

California has distinct requirements when it comes to estimated tax payments, which could vary from federal guidelines:

- Threshold Income Levels: California sets specific income levels as thresholds for when individuals or fiduciaries must file or pay estimated taxes.

- State and Federal Concordance: While similarities exist between state and federal calculations, some variances necessitate adherence to California’s specific guidelines.

Filing Deadlines and Important Dates

- Estimated Tax Payment Deadlines: Typically following the quarterly schedule (April, June, September, and January of the following year).

- Annual Filing Deadline: April 15th is the general deadline for filing Form 5805, but extensions may apply under specific circumstances.

Penalties for Non-Compliance

Failure to submit Form 5805 or underpayment without suitable justification can lead to:

- Financial Penalties: Monetary fines calculated based on the shortfall amount and duration.

- Interest Charges: Additional charges may be accrued on unpaid amounts calculated from the due date until payment is received.

By accurately completing Form 5805 and adhering to payment schedules, taxpayers can ensure compliance and avoid these penalties.