Definition and Meaning

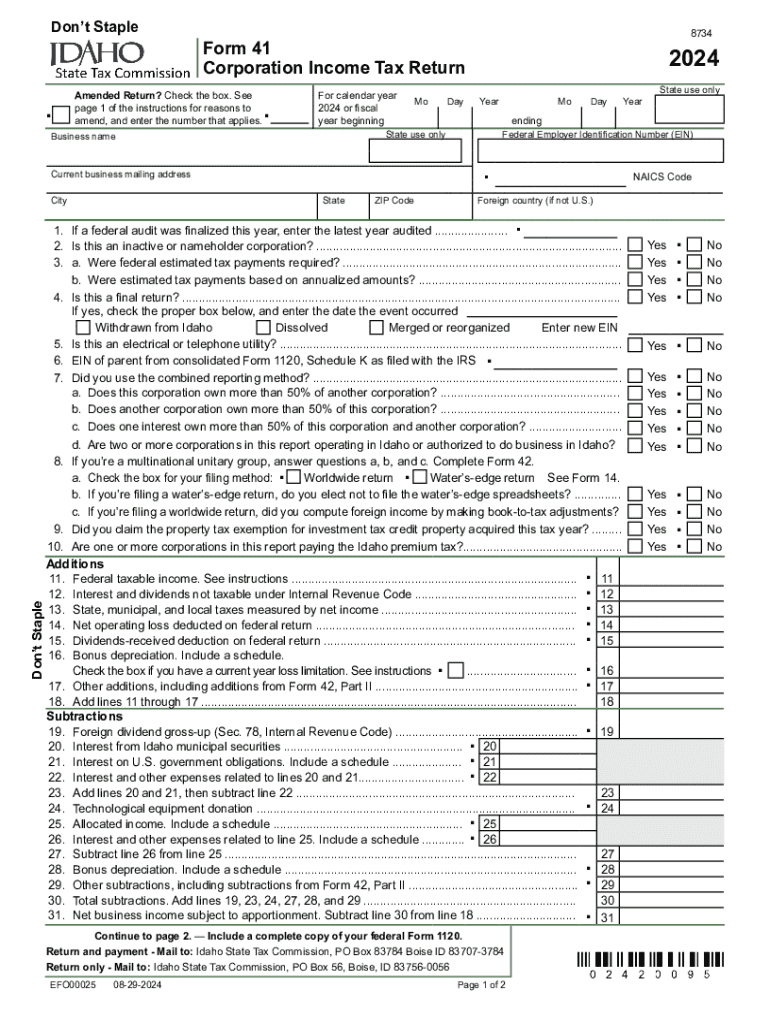

Form 41, known as the Idaho Corporation Income Tax Return and Instructions 2024, is a tax document used by corporations filing their income tax returns in Idaho. This form outlines various sections that require businesses to provide essential information about their operations and financials. Companies utilize this form to report income, compute state taxes owed, and claim applicable tax credits or deductions.

Key sections within the form involve questions regarding estimated tax payments and federal audits. By fulfilling these requirements, corporations ensure compliance with state regulations and accurately report financial activities.

How to Use Form 41, Corporation Income Tax Return and Instructions 2024

To effectively use Form 41, corporations must follow specific steps:

- Gather Necessary Information: Collect all relevant documents, including federal tax returns, financial statements, and records related to income and deductions.

- Fill Out Business Information: Start by completing sections that ask for basic business details, such as name, address, and tax identification number.

- Report Income and Deductions: Use designated sections to declare total income and list deductions or credits that reduce taxable income.

- Calculate Taxes Owed: Follow the instructions to determine the total tax liability based on income and credits.

- Review and Submit: Double-check all entries for accuracy, then submit the completed form via the chosen submission method.

Steps to Complete Form 41, Corporation Income Tax Return and Instructions 2024

Completing the Form 41 involves several detailed steps:

-

Begin with General Information:

- Fill in the corporation name, address, and Federal Employer Identification Number (FEIN).

- Indicate if the corporation is part of a consolidated group.

-

Income and Tax Computation:

- Enter total taxable income using figures from financial statements.

- Compute the Idaho tax liability based on state tax rates.

-

Adjustments and Credits:

- Report any additions or subtractions to federal taxable income.

- Include tax credits applicable, such as those for educational or rehabilitation contributions.

-

Signature and Date:

- An authorized officer must sign and date the form, affirming all information is accurate and complete.

-

Attachments:

- Provide necessary schedules and statements that support data in the form.

Key Elements of the Form 41, Corporation Income Tax Return and Instructions 2024

- Business Information Section: Captures essential data about the corporation, including address and FEIN.

- Income Reporting: Requires details of total income and specific adjustments.

- Tax Calculation: Involves computing tax liabilities based on Idaho's tax laws.

- Tax Credits: Allows for claims on state-specific tax credits.

- Signature Section: Mandatory signature to confirm filed information is accurate.

Filing Deadlines and Important Dates

Corporations must submit their Form 41 by the 15th day of the fourth month following the end of their fiscal year. For most, this is April 15th. It's crucial to adhere to these deadlines to avoid penalties. Extensions may be requested if additional time is needed, but any taxes due should be paid by the original deadline to prevent interest charges.

Required Documents

When completing Form 41, corporations should ensure they have the following:

- Federal tax return copies for reference.

- Financial records detailing income and deductions.

- Documentation for any claimed tax credits.

- Schedule of estimated tax payments and federal audits, if applicable.

Penalties for Non-Compliance

Failure to comply with filing requirements can result in significant penalties. Corporations may face fines for late submissions or inaccuracies in reported information. Penalties can accumulate over time, emphasizing the importance of timely and accurate filing.

State-Specific Rules for the Form 41, Corporation Income Tax Return and Instructions 2024

Idaho has specific regulations that affect how income and deductions are calculated on Form 41. Corporations must carefully consider apportionment factors, especially if they operate in multiple states. Understanding state guidelines can aid in correct tax computation and the identification of eligible credits.