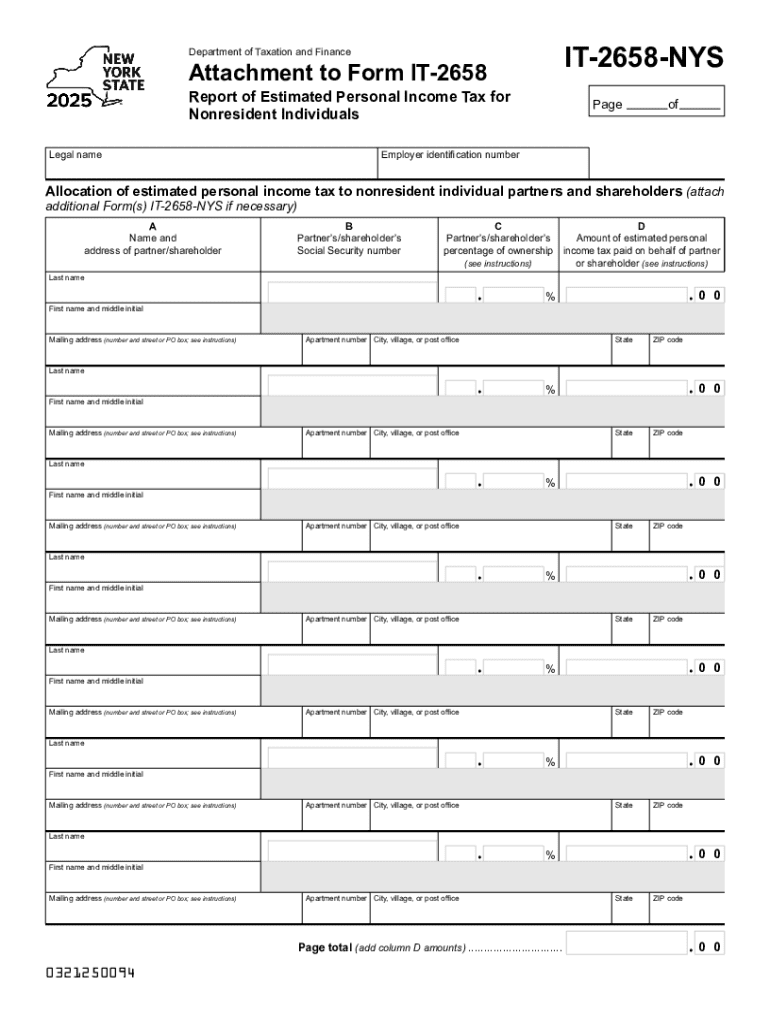

Definition & Purpose of Form IT-2658-NYS

The Form IT-2658-NYS is an attachment to the New York State personal income tax form. Specifically designed for nonresident individuals, it reports estimated personal income tax for those who partake in partnerships, S corporations, and estates or trusts that conduct business in New York. This form facilitates the declaration of owed taxes based on income derived from such entities. Nonresidents, who may not reside in New York but earn income through local businesses, use this form to ensure compliance with state tax obligations.

How to Use Form IT-2658-NYS

To effectively use Form IT-2658-NYS, nonresidents must closely analyze their income derived from New York-based sources. The form requires detailed information, such as partner, shareholder, and beneficiary details, to accurately assess tax liabilities. Users should gather information about income distribution and any payments made by the partners or S corporation on their behalf. Completion of this form ensures appropriate tax deductions and credits are banked against their New York tax obligations, offering them an organized pathway to address state levies adequately.

Steps to Complete Form IT-2658-NYS

-

Gather Necessary Documents: Collect financial documents detailing income from New York-based entities, including K-1 forms and income distribution statements.

-

Enter Personal Information: In the designated section, fill in personal identification details, including name, social security number, and address.

-

Report Income Details: Provide information on income received from partnerships, S corporations, or trusts, ensuring that all figures align with distributed income statements.

-

Calculate Estimated Tax Payments: Use the form to calculate the estimated tax based on New York-sourced income, accommodating any tax payments already made.

-

Review and Validate Information: Double-check all entered data for accuracy to prevent filing errors or future obligations.

-

Submit the Form: Follow outlined methods to submit Form IT-2658-NYS by the due date to avoid penalties.

Who Typically Uses Form IT-2658-NYS

Form IT-2658-NYS is primarily used by individuals who are nonresidents of New York but have financial interests in local partnerships, S corporations, or trusts. This includes nonresident partners and shareholders entitled to income distributions that originate from business activity within the State. The form applies to those seeking to report and remit estimated personal income taxes on their New York-derived income as required under state law.

Key Elements of Form IT-2658-NYS

- Partner and Shareholder Information: Lists details of each partner or shareholder, including ownership percentages.

- Income and Tax Calculation: Details estimated income subject to New York state tax and calculates the due tax amount.

- Filing Instructions: Comprehensive instructions on how to complete and submit the form, emphasizing deadlines and required documentation.

Legal Use of Form IT-2658-NYS

The legal use of Form IT-2658-NYS is to report and pay estimated personal income tax for income garnered through New York business interests. Filing this form is a legal obligation under New York State tax laws for nonresidents earning income through in-state partnerships or S corporations. Accurate completion ensures proper tax compliance and prevents legal issues related to tax evasion or misreporting.

Penalties for Non-Compliance

Failing to file Form IT-2658-NYS or inaccurately reporting income may result in penalties, interest charges, and potential legal ramifications. Non-compliance could lead to audits, assessments of additional taxes, and fines based on the amount of unreported income. Therefore, timely and accurate filing of this form is crucial to avoid these repercussions.

State-Specific Rules for Form IT-2658-NYS

New York State has specific guidelines determining who must file Form IT-2658-NYS, primarily targeting nonresidents with in-state partnerships or corporate interests. Unlike other states, New York mandates such filings when businesses have operations within the state, even if the individual earning the income resides elsewhere. This requirement ensures that taxes are levied appropriately on nonresident incomes earned from New York sources.

Form Submission Methods

Nonresidents can submit Form IT-2658-NYS either electronically through the New York State Department of Taxation and Finance portal or via mail. Electronic submission offers faster processing times and immediate confirmation, while mail submissions require appropriate postage and timing to meet filing deadlines. Users should choose the method that best aligns with their preference for ease and reliability.

Filing Deadlines / Important Dates

The filing deadline for Form IT-2658-NYS typically coincides with the estimated payment due dates, often required quarterly throughout the tax year. Precise deadlines can vary, so it is advisable to check the current year's schedule published by the New York State tax authority to ensure timely compliance. Filing on time is crucial to avoid potential penalties or interest for late submissions.