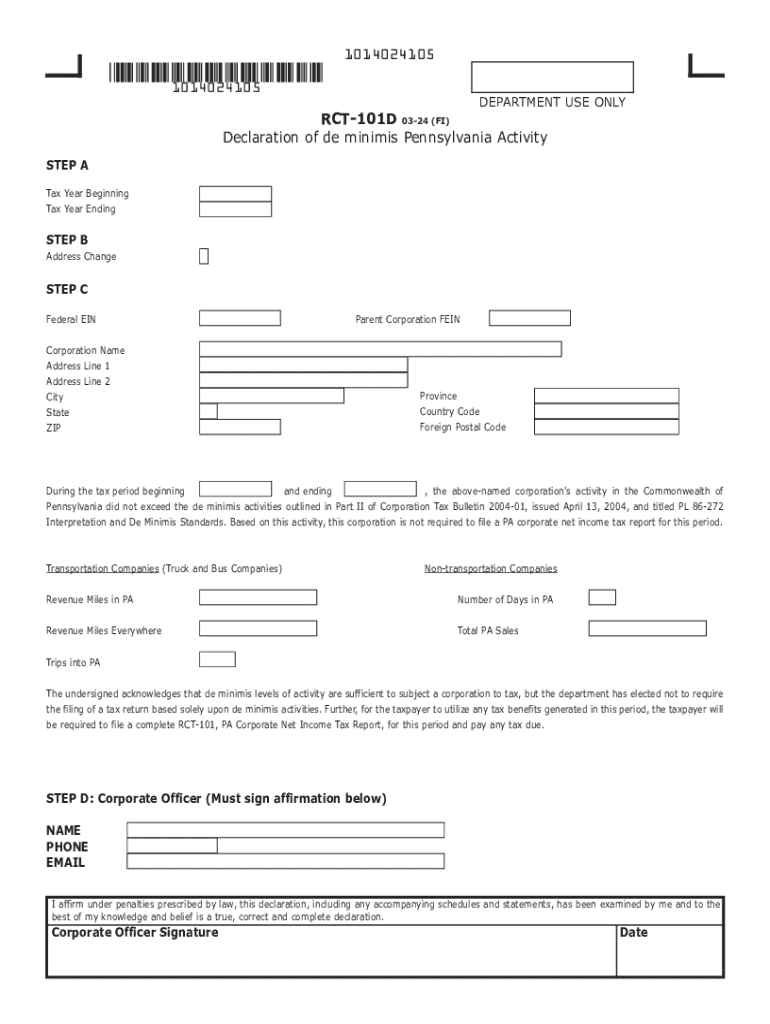

Definition & Meaning

The "Declaration of de minimis Pennsylvania Activity (RCT-101D)" is a specific tax form used in Pennsylvania to declare limited or minor business activities conducted by corporations within the state. This declaration specifies that during the tax period in question, the corporation's activities did not surpass the thresholds set forth in Pennsylvania's tax guidelines. It acknowledges that while certain minimal activities may trigger tax obligations, corporations must submit a comprehensive tax report to leverage any potential tax benefits associated with these activities.

How to Use the Declaration of de minimis Pennsylvania Activity (RCT-101D)

Corporations make use of the RCT-101D form to declare any de minimis business activities within Pennsylvania. It's crucial to ensure that the activities being declared do not exceed the threshold defined by state tax laws. Following these steps, a corporation can accurately file the form:

- Identify the specific business activities completed in Pennsylvania during the relevant tax period.

- Check Pennsylvania’s latest tax guidelines to determine if these activities qualify as de minimis.

- Fill out the form with precise corporate and activity details, ensuring completeness and accuracy.

Corporations must be aware that even if activities are limited, they're required to file appropriate tax documentation.

Steps to Complete the Declaration of de minimis Pennsylvania Activity (RCT-101D)

Filing the RCT-101D involves several methodical steps:

- Gather Documentation: Collect all relevant corporate activity records from the tax year, including financial statements and transaction history.

- Review Thresholds: Refer to Pennsylvania's official tax guidelines to confirm that the activities fall under the de minimis category.

- Complete Form Fields: Enter required information such as tax year dates, corporate details, and activity descriptions. Ensure all sections are filled accurately.

- Officer’s Affirmation: A corporate officer must affirm the accuracy of the declaration by signing the document.

- Submit the Form: Decide on a submission method that suits your corporate setup.

These steps ensure the form is completed properly to support compliance with tax regulations.

Legal Use of the Declaration of de minimis Pennsylvania Activity (RCT-101D)

The legitimate use of the RCT-101D is twofold: First, it functions as a formal declaration acknowledging minor business activities conducted in Pennsylvania that may be subject to state taxes. Secondly, it acts as a required document in the tax reporting process, ensuring that compliance is maintained with state laws. Legal compliance necessitates the correct and timely submission of this declaration by corporations to avoid penalties.

Key Elements of the Declaration of de minimis Pennsylvania Activity (RCT-101D)

Understanding the form’s crucial elements helps ensure accurate completion:

- Tax Year Details: Define the specific period for which the declaration is applicable.

- Corporate Information: Includes the name, address, and tax identification number of the corporation.

- De Minimis Activity Description: Detailed account of activities considered under de minimis thresholds.

- Corporate Officer Signature: Required to attest the accuracy of provided information.

Each element has distinct importance in validating the corporation’s tax position.

State-Specific Rules for the Declaration of de minimis Pennsylvania Activity (RCT-101D)

Pennsylvania's specific regulations around this form dictate the type and extent of activities classified as de minimis. These rules are critical as they:

- Define activity thresholds that characterize minimal or non-taxable corporate actions.

- Outline procedural guidelines for filing and potential rectification if errors occur.

- Provide clarity on how these laws apply to different corporate structures.

These rules vary from those in other states, necessitating thorough comprehension by businesses operating in Pennsylvania.

Filing Deadlines / Important Dates

Adhering to strict deadlines is imperative when filing the RCT-101D. Important dates include:

- Filing Deadline: The form typically follows the corporate tax return deadline, often aligning with the end of the federal tax season.

- Review Periods: Time allocated for the internal review before submission, usually several weeks prior to the final deadline.

- Extension Options: If applicable, extension requests must be submitted by the main deadline.

Remaining cognizant of these dates prevents last-minute rushes and minimizes the risk of late submissions.

Software Compatibility (TurboTax, QuickBooks, etc.)

For efficient handling of the RCT-101D form, companies often utilize tax software solutions compatible with Pennsylvania tax forms:

- TurboTax: Offers tools for managing corporate taxes that integrate the declarations of de minimis activities.

- QuickBooks: Provides transaction tracking and reporting features conducive to managing the form’s requirements.

Utilizing such software ensures accuracy and can simplify the overall management of tax obligations associated with minor corporate activities in Pennsylvania.