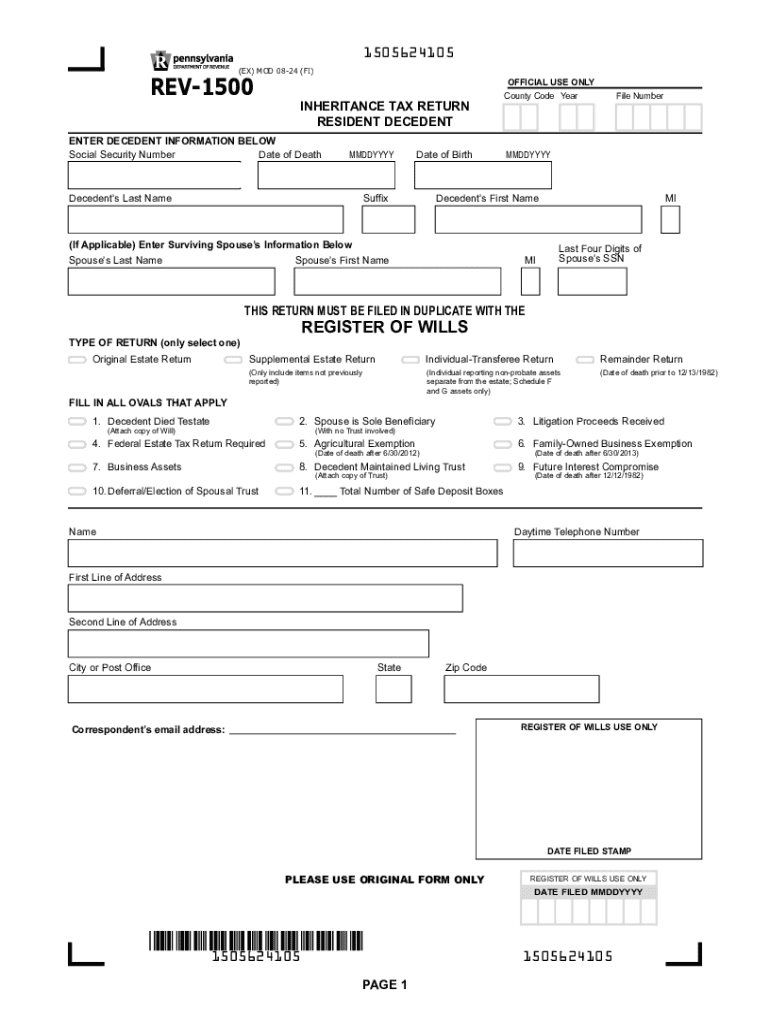

Definition and Meaning of REV-1500

The REV-1500 is a Pennsylvania Inheritance Tax Return form used for the purpose of reporting and calculating inheritance tax obligations for resident decedents. It serves as a crucial document designed to capture detailed information regarding the assets and liabilities of a deceased individual, ensuring proper tax compliance under Pennsylvania state law.

Key Aspects of REV-1500

- Resident Decedents: Specifically tailored for individuals who were legal residents of Pennsylvania at the time of their passing.

- Inheritance Tax: The form calculates taxes owed on inherited assets, which can include real estate, personal belongings, and financial assets.

- Legal Requirement: Filing this form is a mandatory step for estates that meet the specified thresholds for inheritance tax in Pennsylvania.

How to Use the REV-1500

Proper use of the REV-1500 involves several detailed steps to ensure accuracy and compliance. The form is organized into various sections that must be carefully completed.

Sections to Complete

- Decedent Information: Enter details such as the name, date of death, and Social Security number of the deceased.

- Spouse Information: If applicable, provide information about the surviving spouse, including their Social Security number.

- Asset Recapitulation: List and value all properties and assets of the decedent, helping determine the total taxable amount.

- Tax Calculations: Based on the asset values, calculate the inheritance tax owed. This section may require advanced calculations to account for applicable deductions and exemptions.

- Payment Details: Outline how the tax will be paid, indicating if payments will be made in installments or as a lump sum.

Steps to Complete the REV-1500

Completing the REV-1500 requires meticulous attention to detail. Here is a step-by-step guide to help facilitate the process:

- Gather Necessary Documents: Determine all pertinent documents, such as the decedent’s will, asset valuations, and any prior tax returns, to accurately fill out the form.

- Complete Personal Information: Fill in the sections related to the decedent and any surviving spouse.

- List the Assets: Accurately document all assets, including real estate, bank accounts, stocks, and other financial instruments.

- Calculate Taxes: Utilize the provided guidelines to calculate the inheritance tax due.

- Review and Sign: Cross-check all entered information for accuracy. Review the form for any errors before signing.

Important Terms Related to REV-1500

Understanding specific terminology is vital when dealing with the REV-1500 form. Here are some essential terms and their meanings:

- Decedent: The individual who has passed away and whose estate is being settled.

- Beneficiary: A person or entity entitled to receive a portion of the decedent’s estate.

- Asset Recapitulation: The summary and valuation of all the decedent’s assets.

- Exemptions: Deductions allowed from the taxable estate that reduce the overall tax liability.

Filing Deadlines and Important Dates

Deadlines are crucial for the successful filing of the REV-1500. Missing these can result in penalties and additional interest.

Critical Deadlines

- General Submission Period: Typically due nine months after the decedent’s date of death. Extensions may be filed if additional time is needed.

- Late Penalties: A percentage of the tax due might be added as a penalty for late filing or late payment.

Required Documents for REV-1500

Accurate filing requires a comprehensive collection of documents to ensure all data is correct and verifiable.

Essential Documentation

- Will and Trust Documents: Provide legal guidance on the distribution of assets.

- Property Valuations: Appraisals or assessments of real and personal property.

- Investment and Bank Statements: Records showing account values at the time of death.

- Life Insurance: Documentation on any life insurance policies that payout upon the decedent's death.

Legal Use of the REV-1500

The REV-1500 is more than just a tax document; it plays a legal role in estate settlement and tax compliance.

Legal Considerations

- Accuracy Requirement: The information declared must be accurate to the best of the executor’s knowledge, and misrepresentations can have legal repercussions.

- Confidentiality: The information provided on the REV-1500 is treated with confidentiality and used exclusively for determining tax liabilities.

Penalties for Non-Compliance

Failing to properly file the REV-1500 can result in significant financial penalties and further administrative complications.

Consequences

- Financial Penalties: Non-compliance can lead to penalties, including daily interest accumulations on unpaid taxes.

- Legal Repercussions: Continued failure to file can result in legal actions based on Pennsylvania’s tax enforcement statutes.

With precision and adherence to the guidelines, the REV-1500 can be completed successfully, ensuring compliance with Pennsylvania state inheritance tax laws.