Definition and Purpose of Form IT-2664

The Form IT-2664 is a critical document for nonresidents of New York State engaged in the sale or transfer of a cooperative unit. This Estimated Income Tax Payment Form is specifically designed for transactions occurring from December 31, 2023, through January 1, 2025. The form ensures that nonresidents accurately report and remit the estimated income tax due on the gains from such real estate transactions. The primary function of this form is to facilitate the collection of taxes owed to the state for these specific types of sales by nonresidents, effectively bridging the gap between the occurrence of a taxable event and the subsequent tax payment requirement.

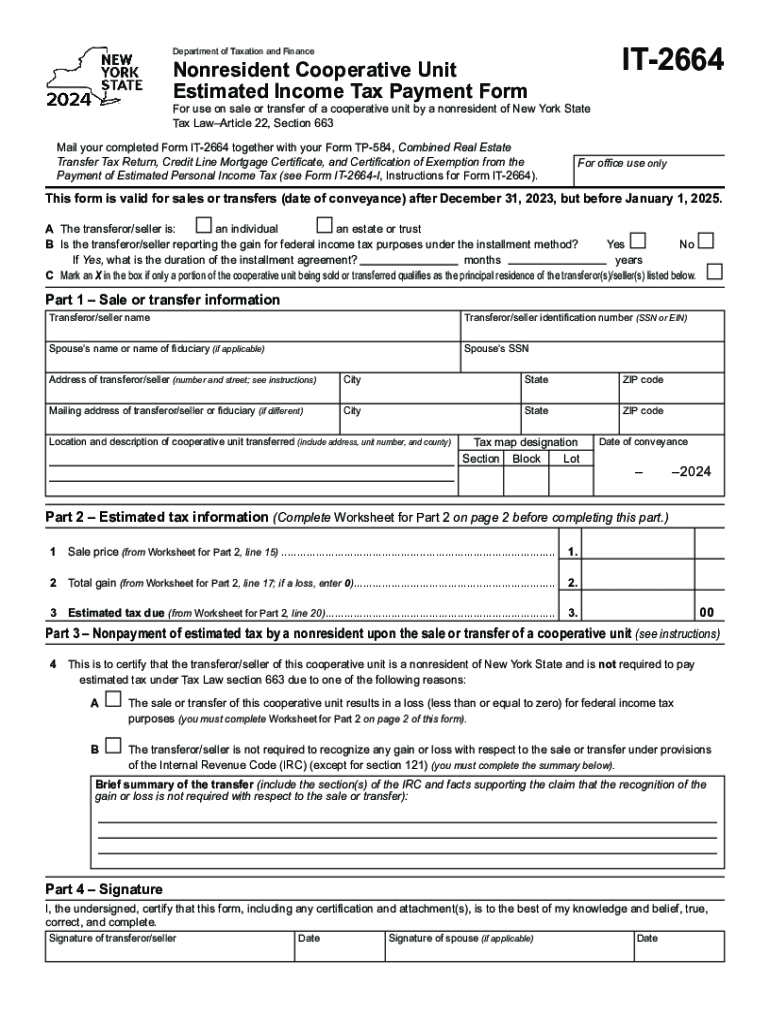

Key Elements of Form IT-2664

Understanding the elements within Form IT-2664 is essential for accurate completion. The form requires vital information such as:

- Transferor/Seller Identification: Includes details like name, address, and social security number.

- Property Descriptions: Specifics about the cooperative unit being sold, including its address and unit number.

- Transaction Information: Includes the sale price, date of sale, and any other pertinent financial data necessary for tax calculations.

- Gain or Loss Calculations: Details on how to compute the gain or loss realized from the sale, which directly impacts the tax due.

- Certification Clauses: These assert that the information provided is truthful and complete, acknowledging the penalties of false reporting.

Steps to Complete Form IT-2664

Accurate completion of Form IT-2664 requires careful attention to detail. Here's a structured approach:

- Collect Personal and Property Details: Ensure all relevant personal identifiers and property details are at hand.

- Calculate Estimated Gain or Loss: Determine the taxable gain by subtracting the adjusted basis of the cooperative unit from the sale proceeds.

- Compute Estimated Tax: Apply New York State tax rates to the calculated gain to determine the estimated tax payment.

- Complete Certification Section: Verify that all details are accurately entered before attesting to their accuracy.

- Submit Tax Payment: Include the calculated estimated tax payment with the form submission.

Filing Deadlines and Important Dates

Timeliness in submitting Form IT-2664 is crucial to avoid penalties. The form, along with the estimated tax payment, must be submitted simultaneously with the property transfer. For transactions falling within the specified window of December 31, 2023, to January 1, 2025, ensuring submission in alignment with these dates is imperative to remain compliant with New York State tax regulations.

How to Obtain Form IT-2664

Form IT-2664 can be accessed through several avenues:

- New York State Department of Taxation and Finance: Available for download from the official website.

- Printed Copies: Can be requested directly from the tax department via postal mail.

- Tax Software: Integrated into tax preparation software suites, simplifying the completion process through guided inputs.

Submitting Form IT-2664

Submission methods for Form IT-2664 include:

- Mail: Send the completed form and payment to the address specified in the form instructions.

- In-Person: Direct submission at designated tax office locations for immediate processing.

- Electronic Filing Systems: Submission through authorized electronic systems offers a streamlined, paperless process.

Who Typically Uses Form IT-2664

The primary users of Form IT-2664 are nonresident individuals or entities involved in the sale or transfer of cooperative units in New York State. This includes:

- Personal Property Sellers: Nonresident individuals selling their cooperative units.

- Investors: Entities such as corporations or trusts that hold cooperative units primarily as investment properties.

- Estates and Trusts: Executors or trustees disposing of estate-held cooperative units.

Non-Compliance Penalties

Fulfilling the requirements of Form IT-2664 is mandatory, as non-compliance can lead to significant penalties:

- Interest on Unpaid Taxes: Accruing from the due date of the tax until payment.

- Fines for Late Submission: Additional penalties for delayed submission beyond the transaction date.

- Legal Repercussions: Potential legal action for intentional underreporting or failure to submit required tax documentation.

Understanding and adhering to these elements ensures compliance with New York State tax regulations and mitigates financial or legal risks.