Definition and Meaning of Form MO-1041

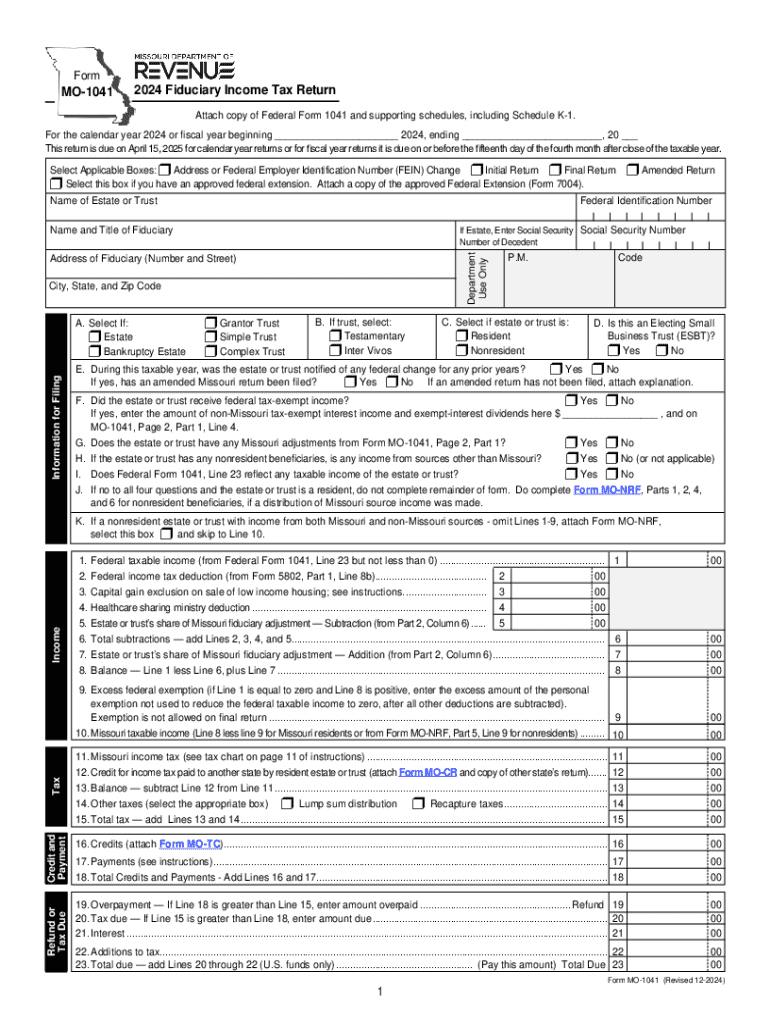

The MO-1041 is the Missouri Fiduciary Income Tax Return Form, used for reporting fiduciary income taxes for estates and trusts within the state. This form is crucial for ensuring that fiduciary entities meet Missouri's tax obligations accurately. It includes specific sections to detail income, deductions, credits, and other relevant tax information pertaining to the fiduciary operations of estates and trusts.

Purpose and Use

The MO-1041 serves as a mechanism for estates and trusts to report their income to the Missouri Department of Revenue. This encompasses the income generated from various sources, such as investments, properties, and other taxable entities associated with the fiduciary's activities. Understanding the purpose of this form is essential for fiduciaries to remain compliant with state tax laws.

Steps to Complete the MO-1041

Filing the MO-1041 requires careful attention to detail. Following a structured approach can simplify this process:

-

Gather Required Information: Accumulate all necessary financial documents, including identification numbers, income statements, and documentation of deductions.

-

Input Identification Information: Complete sections for the trust or estate's name, identification number, and fiduciary details.

-

Report Income: Carefully enter all income sources, including interest, dividends, and any other relevant income streams that the estate or trust has received.

-

Claim Deductions and Credits: Document any applicable deductions and credits, ensuring all calculations align with Missouri tax regulations.

-

Review and Submit: Reassess the completed form for accuracy and submit it as required by the Missouri Department of Revenue.

Important Terms Related to MO-1041

To navigate the MO-1041, understanding key terminologies is vital:

- Fiduciary: An individual or institution managing assets for beneficiaries.

- Estate: Assets and liabilities left by a deceased person.

- Trust: A fiduciary relationship where one party holds assets for another party’s benefit.

- Income Tax: Tax levied by the state on fiduciary income generated within the tax period.

Legal Use of the MO-1041

The MO-1041 is legally binding for reporting fiduciary incomes and liabilities. Missouri state law mandates that estates and trusts operating within the state must complete this form to reflect their tax responsibilities accurately. Ensuring timely and precise filing is crucial to avoid legal repercussions and penalties from the Missouri Department of Revenue.

Filing Deadlines and Important Dates

The completion and submission of the MO-1041 must adhere to specific deadlines:

- Annual Filing Date: Estates and trusts must file the MO-1041 by the 15th day of the fourth month after the close of the taxable year.

- Extensions: If an estate or trust cannot meet this deadline, an extension request must be filed by the original due date to avoid late filing penalties.

Required Documents for Filing

Compiling the necessary documents is a critical preparatory step:

- Identification Numbers: Federal and state identification numbers.

- Income Statements: Documents detailing all income sources.

- Deduction Records: Proof of eligible deductions and credits.

- Financial Statements: Summary of asset and liability positions as required by the Missouri Department of Revenue.

Form Submission Methods

The MO-1041 can be submitted through various channels to suit filer preferences:

- Online Submission: Electronic filing through the Missouri Department of Revenue's platform is encouraged for its efficiency and instant tracking capabilities.

- Mail: Filers can submit a paper version via traditional mail; however, this method may involve longer processing times.

- In-Person: Some filers may prefer to deliver the form personally to a local revenue office.

Penalties for Non-Compliance

Failure to comply with the MO-1041 filing requirements can result in specific penalties:

- Late Filing: Penalties for not filing on time may accrue daily.

- Underpayment: Additional charges for underreporting taxable income or claiming unauthorized deductions.

Adhering strictly to filing requirements protects fiduciaries from accruing unnecessary financial and legal setbacks.

Digital vs. Paper Version of the MO-1041

Utilizing digital forms can streamline the filing process:

- Electronic Filing Advantages: Faster processing and immediate error-checking facilities.

- Paper-Based Filing: While still viable, this method can delay processing due to mail times and manual data entry requirements.

Electronic filing is generally recommended to ensure timely accuracy and efficiency in completing fiduciary tax obligations.