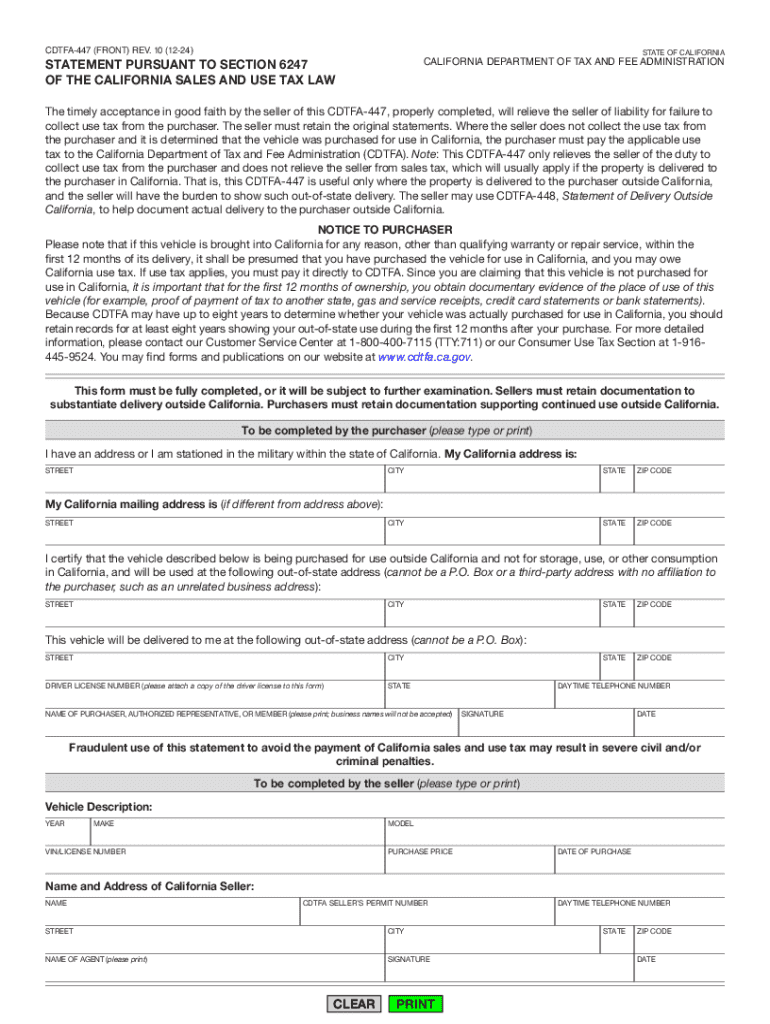

Definition and Meaning of CDTFA-447

The CDTFA-447, known as the Statement Pursuant to Section 6247 of the California Sales and Use Tax Law, is a crucial document issued by the California Department of Tax and Fee Administration (CDTFA). It allows sellers to accept a statement from buyers claiming a vehicle is intended for use outside California. This form ensures that sellers are relieved from the responsibility of collecting use tax on such sales, as long as delivery occurs out-of-state.

Purpose and Utilization

The primary purpose of the CDTFA-447 is to document sales where a vehicle is purchased for use exclusively outside California. Sellers need to verify the integrity of the buyer's statement to remain compliant and avoid potential tax liabilities. It plays a vital role in transactions involving vehicles intended for out-of-state use, providing a structured way to acknowledge and record such sales, minimizing the risk of disputes or tax-related repercussions.

How to Use the CDTFA-447

Effectively using the CDTFA-447 requires adherence to specific processes to ensure its validity. Here’s a step-by-step guide:

-

Seller-Side Requirements

- Verify that the buyer intends to use the vehicle exclusively outside California.

- Ensure the form is accurately completed with all necessary information from the buyer.

- Retain a copy of the completed form for record-keeping.

-

Buyer-Side Information

- Provide clear and truthful information about the intended use of the vehicle.

- Commit to the vehicle’s delivery outside California according to stipulated timelines.

Key Elements of the CDTFA-447

Various elements need careful attention when completing the CDTFA-447:

- Buyer Information: Full details including name, address, and identification numbers.

- Vehicle Details: Make, model, identification number, and proof that it will be delivered out of state.

- Declaration and Signature: Buyer’s signature to confirm the accuracy and truthfulness of the statement.

Steps to Complete the CDTFA-447

To accurately complete the CDTFA-447 form, follow these steps:

- Gather Information: Collect all relevant buyer data and vehicle specifics.

- Fill Out the Form: Insert details in the respective sections of the form, ensuring completeness and accuracy.

- Review and Sign: Both parties should carefully review for errors before signing.

- Submit the Documentation: Retain a copy for your records and ensure timely submission to the relevant tax authorities if necessary.

Legal Use and Compliance

Understanding the legal implications of the CDTFA-447 underpins its utility. Sellers need to ensure compliance with all requirements set forth in Section 6247 of the California Sales and Use Tax Law to mitigate the risk of incurring penalties.

Penalties for Non-Compliance

Failure to comply with the regulations associated with the CDTFA-447 can lead to significant penalties. Non-compliance may involve incomplete documentation or false declarations, resulting in fines or back tax assessments.

Who Issues the Form

The CDTFA-447 form is issued by the California Department of Tax and Fee Administration. It’s crucial for sellers engaging in out-of-state vehicle transactions to utilize the form to validate and document the exemption from use tax collection.

Who Typically Uses the CDTFA-447

The form is primarily used by vehicle sellers and dealerships involved in interstate sales. It’s an essential tool for:

- Automobile Dealers: Those selling vehicles with delivery outside of California.

- Private Sellers: Individuals selling vehicles to out-of-state buyers and needing formal documentation to prevent tax liabilities.

State-Specific Rules for Using the CDTFA-447

While the CDTFA-447 is specific to California, understanding its application within the broader scope of interstate commerce is necessary. Sellers must be aware that the form relates uniquely to California's tax statutes and not reused or adapted for other states without adjustments.

Regional Considerations

It’s critical to note any regional variations in terms and conditions surrounding the CDTFA-447. While the form itself is standard, regulatory interpretations or enforcement may vary slightly across different jurisdictions within California.

Practical Examples of CDTFA-447 Utilization

To better grasp the use of CDTFA-447, consider these scenarios:

- Dealership Sale: A California dealership sells a vehicle to an Oregon resident, delivering it to the buyer’s Oregon address, complete with a signed CDTFA-447 confirming the out-of-state usage.

- Private Transaction: A private seller in California sells a car to a Nevada resident. The CDTFA-447 ensures the seller isn’t liable for California use tax, since the vehicle is intended for exclusive use in Nevada.

These examples illustrate the form's operational importance in expediting vehicle sales while safeguarding both seller and buyer interests.

Filing Deadlines and Important Dates

Proper timing is essential for the CDTFA-447:

- Retention of Records: Sellers must retain the completed form in their records for a specified period as part of their compliance requirements.

- Document Submission: While not routinely submitted, have documentation ready for review by tax authorities if needed.

Compliance Timeline

Failing to adhere to the deadlines for completing or retaining the form can result in penalties or the loss of tax relief benefits under Section 6247 provisions.

Software Compatibility

Understanding the digital aspects of processing the CDTFA-447 is increasingly important. Compatibility with modern software systems can simplify adherence to compliance requirements, ensuring streamlined workflows for:

- TurboTax and QuickBooks: Software solutions may offer functionality to reference or log sales records involving CDTFA-447 for tax preparation purposes.

- DocHub: Can facilitate the document's electronic management, including signing and storage, enhancing accessibility and compliance.

These tools ensure buyers and sellers maintain comprehensive records, critical to effective financial and legal stewardship.