Definition and Meaning

Form 568, officially titled the Limited Liability Company Return of Income, is used primarily by LLCs to report income, deductions, and tax liabilities specific to California. It is mandated by the California Franchise Tax Board for LLCs that must report financial activities, distributions, and payments to ensure compliance with state tax regulations. This form plays a critical role in outlining the income-sharing proportions among LLC members through Schedule K-1.

Key Elements of the Form 568

Income and Deductions

- Gross Income Reporting: Form 568 requires the declaration of all income generated by the LLC during the fiscal year. This includes earnings from services, sales of goods, and any miscellaneous revenue.

- Deductions: The form enables LLCs to subtract eligible expenses, such as business operational costs, salaries, and other claimed deductions, which directly impacts taxable income.

Schedules and Attachments

- Schedule K-1: Essential for reporting each member's share of income, deductions, and credits.

- Schedule EO: Tracks ownership changes throughout the tax year.

- Schedule D-1: Used to report gains and losses from sales or exchanges of the LLC's capital assets.

Steps to Complete the Form 568

- Gather Financial Statements: Collect income statements, balance sheets, and records of expenses.

- Calculate Gross Income: Accumulate total revenue from all sources.

- Deduct Allowable Expenses: Input eligible deductions to lessen tax liability.

- Complete Schedules: Fill out Schedule K-1 and others, as necessary.

- Report Distributions: Specify distributions to members throughout the year.

- Review and Sign: Double-check for errors and secure all necessary signatures.

Eligibility Criteria

LLCs organized or registered to conduct business in California are required to file Form 568. This also includes foreign LLCs with California-derived income or doing business in the state. Regardless of income levels, these entities must comply by submitting the form annually to ensure proper taxation.

Filing Deadlines and Important Dates

- Annual Due Date: The completed Form 568 is generally due by the 15th day of the 4th month following the close of the LLC’s fiscal year, usually April 15 for calendar-year filers.

- Extension Requests: LLCs can request extensions, typically allowing six extra months, but this does not defer tax payment obligations.

Required Documents

- Financial Records: Detailed income and expense ledgers.

- Membership Agreements: Documentation of ownership percentages and changes.

- Prior-Year Filings: If applicable, past returns for reference.

Form Submission Methods

Online Filing

- California's MyFTB: Secure platform for electronic submission; offers immediate confirmation.

- Tax Software: Compatible with systems like TurboTax and QuickBooks, enabling integrated e-filing.

- Paper Submission: Traditional method requiring physical mailing of completed forms and schedules.

Penalties for Non-Compliance

Failure to file Form 568 timely, or provide accurate information, can lead to penalties ranging from late payment fees to misstatement fines. California imposes a significant penalty for non-filing, calculated based on a percentage of unpaid taxes, and interest accrues on any outstanding amounts.

State-Specific Rules

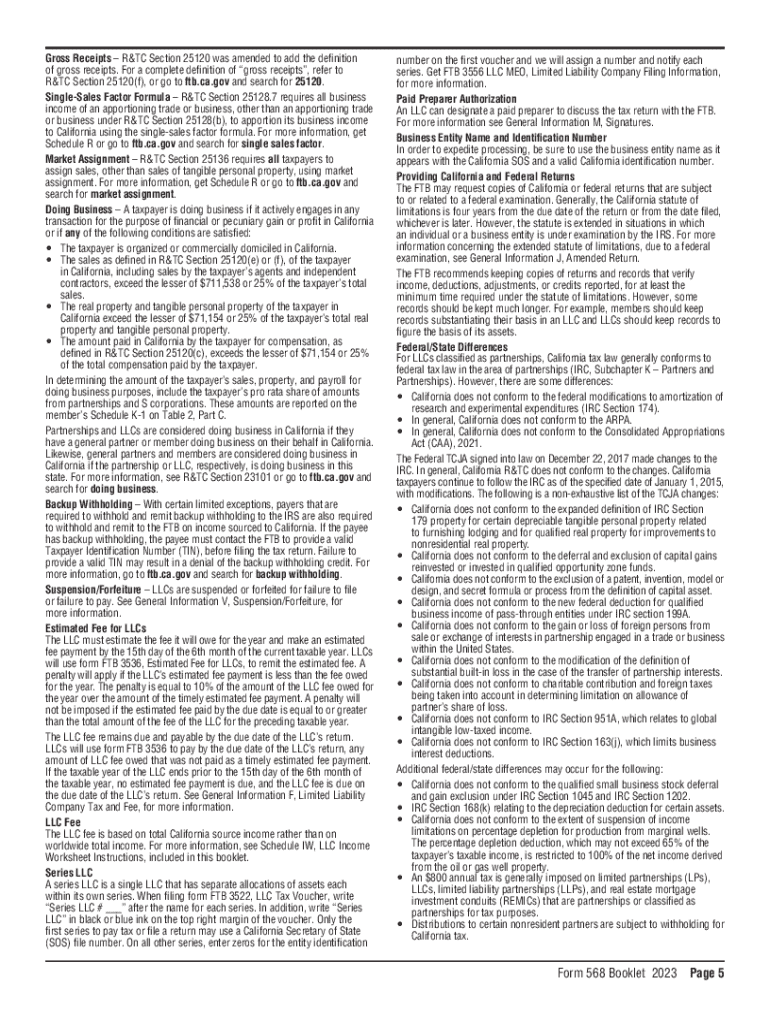

California demands the payment of an annual minimum franchise tax for LLCs, currently set at $800, irrespective of profit margins. Additionally, LLCs with gross receipts exceeding certain thresholds may be subject to an LLC fee, separate from the standard income tax liabilities. This reinforces the complexity of compliance and the need for accurate, timely filing in accordance with state laws.