Definition and Purpose of Schedule K-1 (Form 1041)

The Schedule K-1 (Form 1041) serves a crucial role in the U.S. tax system by linking the income generated by an estate or trust to the beneficiaries entitled to receive it. This form reports a beneficiary's share of income, credits, deductions, and other tax-related items arising from an estate or trust. The 2011 version required accurate reporting of various income types, such as interest, dividends, capital gains, and any other distributions made to beneficiaries. Understanding the function of the Schedule K-1 (Form 1041) is essential for proper filing and compliance with tax laws.

How to Use the 2011 Form 1041 K-1

To effectively use the 2011 Form 1041 K-1, beneficiaries must incorporate the information provided into their personal tax returns. Each section of the form is designed to feed specific data into corresponding lines on the beneficiary's tax return, such as Form 1040. Detailed instructions are provided by the IRS for each section to ensure that income and other tax-related items are accurately reported. It is vital to review all information provided on the K-1 form carefully and consult with a tax professional if needed to ensure compliance.

Steps to Accurately Report Income:

- Transfer your share of estate/trust income to your personal tax return.

- Enter dividends, capital gains, and other specified amounts on the appropriate lines.

- Deduct allocated expenses and losses as instructed in the form guidelines.

- Review calculations and confirm the correct tax treatment for each income type.

How to Obtain the 2011 Form 1041 K-1

The Schedule K-1 (Form 1041) for 2011 is generally issued by the fiduciary of the estate or trust. Beneficiaries should receive this form automatically once the estate or trust has completed its tax filings. If not received, beneficiaries should contact the fiduciary to obtain a copy. For historical forms, they can also be accessed through tax preparation software archives or directly from IRS resources, where available.

Obtaining from Different Sources:

- Fiduciary of the Estate/Trust: Main point of contact.

- IRS Archives: For older forms, IRS websites may have historical data.

- Tax Software: Some platforms maintain records of previous filings.

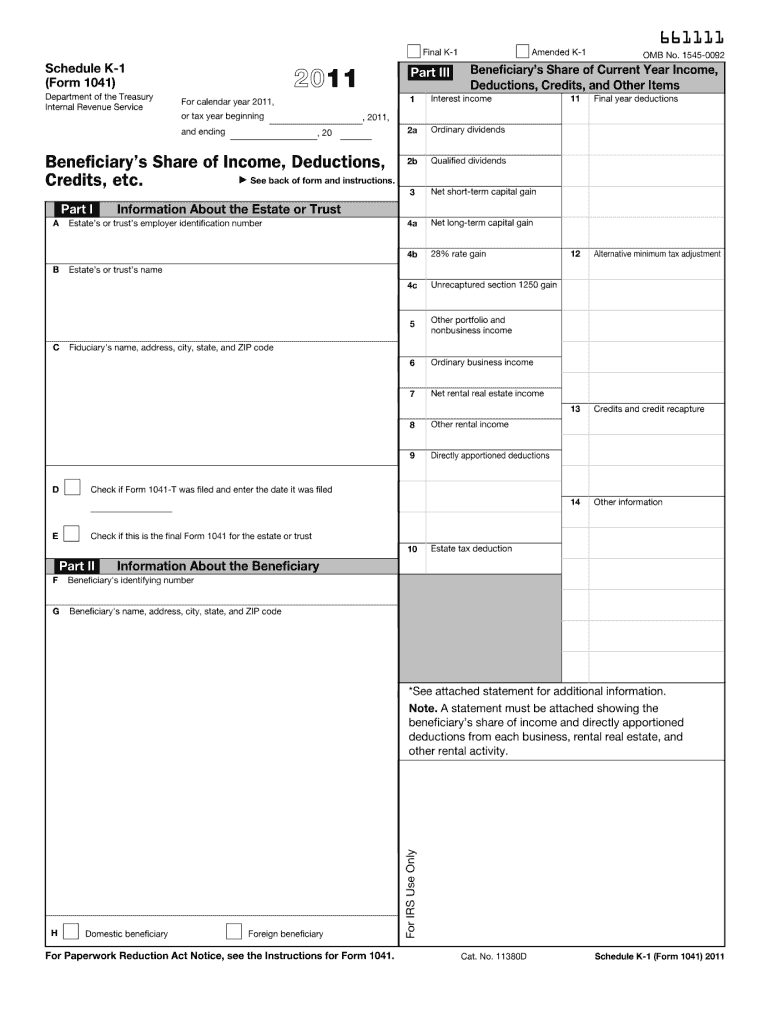

Key Elements of the Form 1041 K-1

The 2011 Form 1041 K-1 is divided into several key sections that each report different types of information related to the distribution of income:

- Part I: Information about the estate or trust, such as the employer identification number (EIN).

- Part II: Beneficiary information, including their identity and share percentage.

- Part III: The breakdown of income and deduction items allocated to the beneficiary. This includes interest, ordinary dividends, capital gains, and other specifics.

Comprehensive Breakdown:

- Income Distribution: Details primary and secondary income sources, such as interest and royalties.

- Deductions and Credits: Reports allowed deductions and applicable credits.

- Tax Withheld: Indicates any taxes withheld at the estate or trust level.

Important Terms Related to 2011 Form 1041 K-1

Several terms are critical to understanding and correctly using the Form 1041 K-1:

- Beneficiary: The person or entity entitled to receive property from the estate or trust.

- Fiduciary: The executor, administrator, or trustee responsible for managing the estate or trust affairs.

- Distributable Net Income (DNI): Represents the limit on the income distribution deduction the estate or trust can claim.

Additional Clarifications:

- Capital Gains and Losses: How they affect distributions.

- Pass-Through Entity: The mechanism by which income is reported to beneficiaries.

Steps to Complete the 2011 Form 1041 K-1

Completing the 2011 Form 1041 K-1 involves gathering accurate information and detailing various income aspects:

- Gather All Required Information: Ensure you have details about the estate or trust, including financial data and EIN.

- Calculate Income Distribution: Use available data to determine each beneficiary's share of net income.

- Complete the Required Sections: Fill out all sections of the K-1 form accurately and comprehensively.

- Review for Accuracy: Double-check entries to minimize errors before submission.

Common Pitfalls to Avoid:

- Misreporting income types or amounts.

- Overlooking deductions or credits that the beneficiary is entitled to claim.

Filing Deadlines and Important Dates

The filing of the Form 1041 K-1 is tied to the broader tax obligations of the estate or trust. The fiduciary must file the Form 1041 by April 15 following the close of the tax year in question. Beneficiaries should ensure they receive their K-1 forms promptly to meet their personal tax filing deadlines, usually the same April 15 date, unless an extension has been granted.

Notable Considerations:

- Extensions: Understand the implications for both estate/trust and beneficiary if filing extensions are sought.

- Penalties for Late Filing: Be aware of potential fines and penalties for delayed submissions.

IRS Guidelines and Compliance

Adhering to IRS guidelines for the Form 1041 K-1 is imperative for accurate reporting and compliance:

- Follow detailed IRS instructions for each form section.

- Keep official records and proofs of all data reported.

- Utilize IRS resources and guidelines to clarify any uncertainties in form completion.

Compliance Checks:

- Confirm alignment with IRS updates or changes from prior years.

- Seek professional advice if discrepancies or peculiar situations arise.

Penalties for Non-Compliance

Failing to properly report using the Form 1041 K-1 can lead to several penalties, from monetary fines to more severe tax audits. Non-compliance might include inaccurately transferring K-1 information to personal tax returns, underreporting, and missing deadlines.

Mitigation Strategies:

- Timely Filing: Ensures no missed deadlines.

- Accurate Reporting: Thoroughly verify data transferred to personal filings.

- Consultation with Tax Experts: Use expertise for complex scenarios or unusual income types.

Each of these sections provides a deep dive into the varied aspects of the 2011 Form 1041 K-1, ensuring comprehensive understanding and proper utilization to avoid issues with tax reporting and compliance.