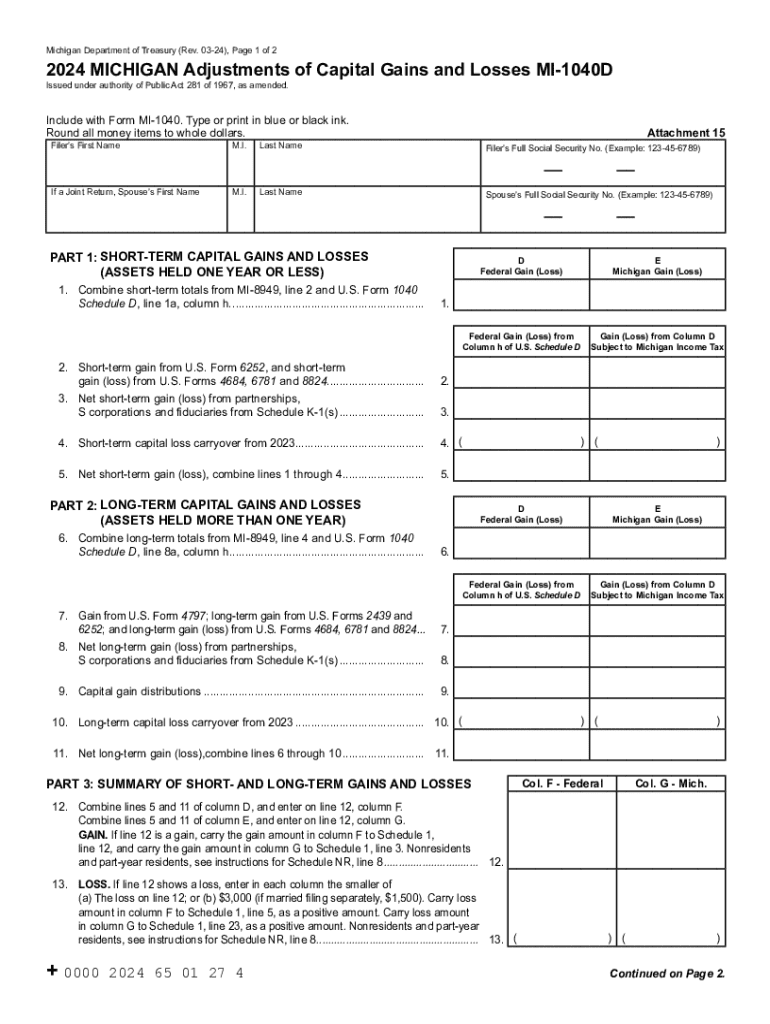

Definition and Purpose of the 2024 Michigan Adjustments of Capital Gains and Losses MI-1040D

The 2024 Michigan Adjustments of Capital Gains and Losses (Form MI-1040D) is an essential document for Michigan taxpayers. It is used to calculate and report short-term and long-term capital gains and losses on state income tax returns. This form necessitates data from both federal and Michigan sources, ensuring precise adjustments specific to Michigan's tax laws. The form's primary goal is to guide taxpayers in modifying their federal figures to comply with Michigan's state-specific regulations, ensuring accurate tax filings and compliance.

The MI-1040D has sections to record various data such as sales price, cost basis, and proceeds of investments. Adjustments might include special provisions for nonresidents or part-year residents and recalculations for assets held over differing periods. Detailed explanations on computation enable taxpayers to apply federal regulations aligned with state-specific directives.

How to Use the 2024 Michigan Adjustments of Capital Gains and Losses MI-1040D

Using the MI-1040D efficiently involves properly understanding each section and entering correct data. Here’s a step-by-step breakdown:

-

Gather Necessary Information:

- Compile all tax documents showcasing capital gains or losses.

- Ensure federal tax return figures are available for reference.

-

Fill the Form Steps:

- On the form, first enter your details like name and Social Security number.

- Proceed to the sections detailing short-term and long-term gains calculations separately.

- Adjust your capital gains or losses from federal to Michigan-specific calculations.

-

Adjust for State Variances:

- Consider nonresident and part-year resident adjustments, if applicable.

- Factor in any state-specific tax credits or exclusions.

-

Submit the Fully Completed Form:

- Once filled, review entries for accuracy.

- Finalize your submission with the Michigan Department of Treasury within stipulated dates.

Required Documents to Complete Form MI-1040D

To accurately complete the form, ensure you have the following documentation:

- Federal tax return forms, specifically Schedule D for capital gains and losses.

- Records of asset transactions, including sales receipts and cost basis documents.

- Any supporting forms for state-specific adjustments, like adjustments for nonresidents.

- Previous year’s MI-1040D, if filing capital loss carryovers.

These documents will provide the figures and basis required for accurate reporting of capital transactions on your Michigan state tax.

State-Specific Rules for Adapting Federal Capital Gains Figures

When adapting federal capital gains data to Michigan’s requirements:

-

Factor in Michigan-specific Deductions:

- Certain municipal bonds or specific employer stock incentive programs might adjust capital gains.

-

Address Residency Status Impacts:

- Full-year residents must adjust all gains regardless of where they occur.

- Nonresidents and part-time residents should carefully adjust gains associated with Michigan sources only.

-

Consider State-Specific Income Offsets:

- Any federal tax breaks not recognized by Michigan will necessitate adjustments, e.g., retirement account sales.

Michigan’s tax laws might slightly diverge from federal ones, and emphasizing these differences ensures compliance and avoids penalties.

Eligibility Criteria for Filing Form MI-1040D

Eligibility to file the MI-1040D primarily involves:

- Residents of Michigan who have reported capital gains or losses on their federal tax returns.

- Nonresidents and part-year residents with income sourced from Michigan investments.

- Taxpayers with capital gains or capital loss carryovers needing to adjust federal returns for state compliance.

Anyone generating taxable income through asset sales or similar transitions must evaluate potential obligations regarding the MI-1040D.

Submission Methods for 2024 Michigan MI-1040D

Michigan taxpayers can opt from the following submission methods for their MI-1040D:

-

Online Submission:

- Using Michigan’s e-file system, part of the Michigan Department of Treasury’s web service, for electronic filing.

-

Mail Submission:

- Print the completed form and mail it to the provided Michigan Department of Treasury address.

-

In-person Submission:

- Drop off at designated Michigan State Treasury offices if available.

Choosing an appropriate submission method facilitates timelines compliance and potentially reduces processing times.

Penalties for Non-Compliance with MI-1040D

Failing to correctly complete the MI-1040D can result in several penalties:

-

Underpayment Penalties:

- Incorrect calculations leading to underpayment can incur interest charges.

-

Late Filing Penalties:

- Not filing by Michigan’s deadlines results in penalties augmented daily until resolved.

-

Inaccurate Filing Consequences:

- Misreporting gains/losses may not only lead to fines but trigger audits requiring considerable time to rectify.

It is imperative for taxpayers to understand compliance requirements to avoid costly penalties and potential legal consequences.