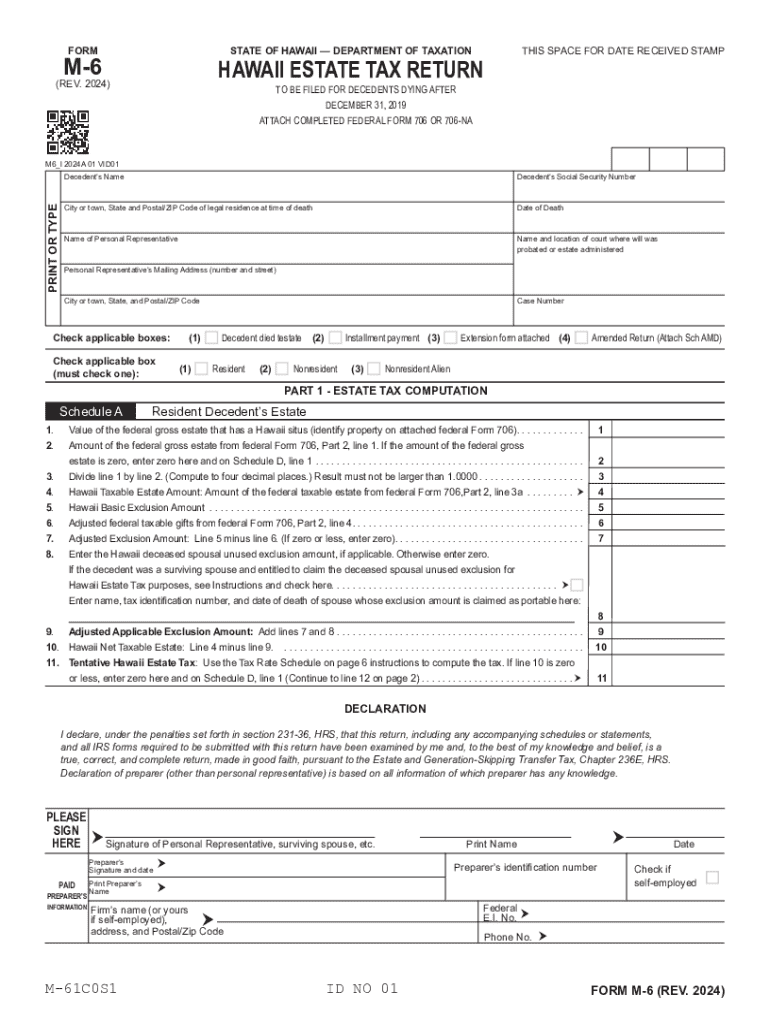

Definition and Purpose of the M-6 (Rev 2024), Hawaii Estate Tax Return

The M-6 (Rev 2024), Hawaii Estate Tax Return, is a mandatory tax document used by estates of decedents who passed away after December 31, 2019, to report estate tax liabilities in Hawaii. This form is essential for estates that meet certain criteria, as it facilitates the calculation and declaration of the Hawaii taxable estate value, determining the estate tax due under state law. Key sections of the form include personal information about the decedent, estate tax computation, and various schedules tailored for residents, nonresidents, and nonresident aliens.

Steps to Complete the M-6 (Rev 2024), Hawaii Estate Tax Return

-

Gather Necessary Information: Collect all relevant documents related to the decedent's estate, including assets, liabilities, and any prior tax filings that might impact the tax return.

-

Complete Personal Identification Data: Fill in the decedent's personal information. This section requires accurate data to ensure the form is processed correctly.

-

Calculate the Taxable Estate: Use the provided schedules to list and calculate the decedent’s assets and allowable deductions. These entries will form the basis for determining the taxable estate value.

-

Apply Applicable Exclusions: Determine applicable tax exclusions and deductions under Hawaii tax law, ensuring accurate computation of the total estate tax liability.

-

Complete Supplemental Schedules: According to the decedent's residency status, complete the appropriate schedules that pertain to residents, nonresidents, or aliens to reflect the correct tax scenario.

-

Sign and Review the Form: Ensure all sections of the form are completed accurately. The executor or personal representative of the estate must sign the document before submission.

-

File and Pay Tax: Submit the completed form and arrange payment of any calculated estate tax by the specified deadline to avoid late penalties.

How to Obtain the M-6 (Rev 2024), Hawaii Estate Tax Return

-

Direct Download: The form can typically be downloaded from the Hawaii Department of Taxation’s official website. Ensure you have the latest version to comply with the most current regulations.

-

Request by Mail: If online access is unavailable, you can request the form by contacting the Hawaii Department of Taxation for a physical copy.

-

Professional Assistance: Licensed tax professionals often have access to required forms and can assist in obtaining and completing them accurately.

Important Terms Related to the M-6 (Rev 2024), Hawaii Estate Tax Return

-

Decedent: The individual whose estate is subject to the tax return.

-

Executor: The person responsible for managing the decedent's estate and ensuring compliance with tax filing requirements.

-

Taxable Estate: The total estate value after applicable deductions and exclusions. This figure determines the estate’s tax liability.

-

Nonresident Alien: An individual who resides outside the United States and holds foreign citizenship, impacting their estate tax treatment in Hawaii.

Filing Deadlines and Important Dates

-

Estate Tax Filing Date: The M-6 (Rev 2024) form must be filed within nine months following the decedent’s date of death. This deadline is critical to avoid penalties.

-

Payment Deadlines: Estate taxes payable based on the filed return are due at the time of filing to prevent accrual of interest and penalties for late payment.

-

Extension Requests: A six-month filing extension may be requested, but it does not extend the time for payment of the estate tax.

Who Typically Uses the M-6 (Rev 2024), Hawaii Estate Tax Return

-

Personal Representatives: Executors or administrators managing estates of decedents are responsible for filing the return.

-

Large Estates: Estates meeting the taxable threshold as defined by Hawaii law are required to file.

-

Tax Advisors and Preparers: These professionals assist taxpayers in understanding estate obligations and completing the required forms accurately.

Penalties for Non-Compliance

-

Late Filing Penalty: A penalty is imposed if the estate tax return is not filed by the due date (including extensions).

-

Interest on Unpaid Tax: Interest accrues on any unpaid estate tax from the original due date until the date of payment.

-

Accuracy-related Penalties: If there are significant inaccuracies in the reported taxable estate or taxes due, additional fines may be levied.

Form Submission Methods: Online and Mail

-

Online Filing: Submit the form electronically through the Hawaii Department of Taxation's secure portal. This method is efficient and provides immediate confirmation of receipt.

-

Mail Submission: Alternatively, the completed form and check for any taxes due can be mailed to the designated address provided by the Hawaii Department of Taxation.

Overall, accurately completing the M-6 (Rev 2024), Hawaii Estate Tax Return, requires careful attention to detail, timely submission, and thorough documentation of the decedent's estate details to ensure compliance and minimize financial liabilities.