Definition and Purpose of the DR-15N

The DR-15N is a comprehensive instructional guide used for filing the Florida Sales and Use Tax Return. This document provides essential guidelines for businesses needing to report their sales activities within Florida. It covers the intricacies of filing, including definitions, reporting requirements, and compliance protocols. Businesses can use the DR-15N to ensure their sales and use tax filings are accurate and in line with state regulations, thereby avoiding potential penalties and ensuring they meet their tax obligations effectively.

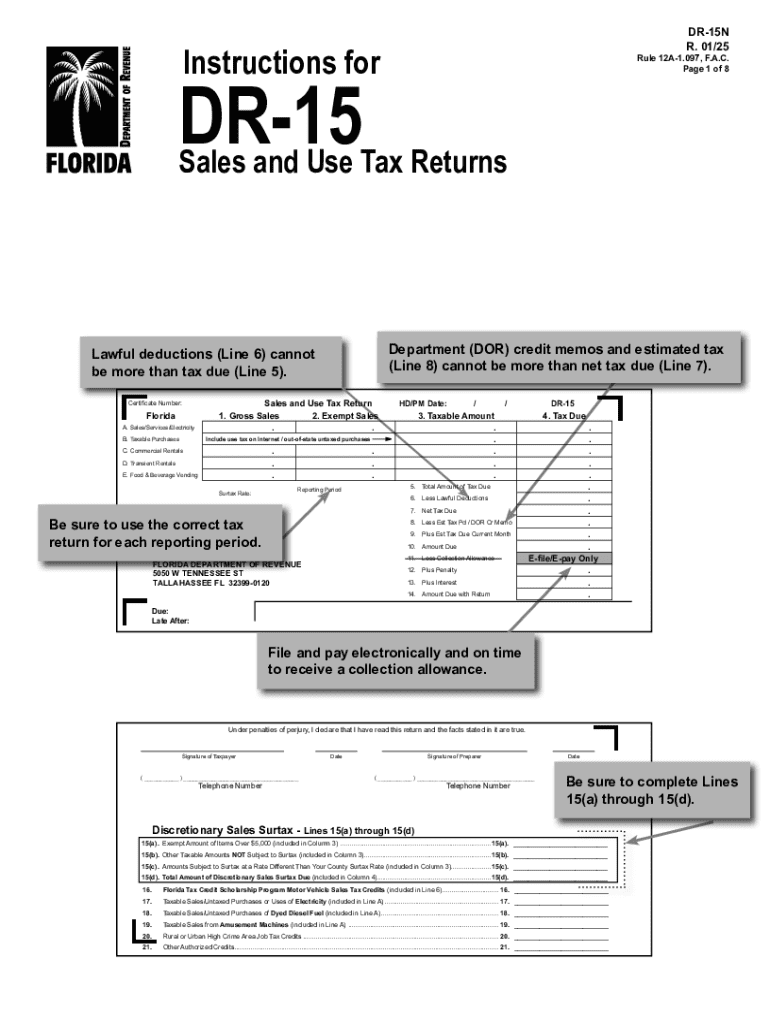

Steps to Complete the DR-15N

Completing the DR-15N involves several steps designed to ensure accurate reporting of sales transactions. The following sections detail the necessary actions:

- Gather Necessary Information: Prepare detailed records of all sales activities, including gross sales, exempt sales, and taxable amounts.

- Calculate Tax Due: Use provided guidelines to determine the correct tax amount owed to the state. This includes assessing applicable discretionary sales surtax.

- Enter Required Information: Fill out the DR-15N, following line-by-line instructions to ensure each section is completed accurately.

- Review for Accuracy: Cross-check all entered data to ensure there are no errors or omissions.

- Finalize and Submit: Submit the completed form through designated methods—either electronically, by mail, or in-person.

Important Terms Related to the DR-15N

Understanding key terminology is crucial for accurate completion of the DR-15N:

- Gross Sales: Total sales revenue before deductions.

- Exempt Sales: Sales that are not subject to tax under specific conditions.

- Discretionary Sales Surtax: Additional local tax applicable in certain Florida counties.

- Estimated Tax Payments: Pre-payments made to cover anticipated tax liabilities.

Key Elements of the DR-15N

The DR-15N form comprises important sections necessary for compliance with Florida's tax laws:

- Gross Sales Reporting: Instructions for reporting total revenue generated.

- Tax Calculation: Details on calculating the accurate tax amount based on reported sales.

- Deductions: Guidelines regarding lawful deductions recognizable by the state.

- Penalties and Compliance: Information about the repercussions of late submissions or non-compliance.

Filing Deadlines and Important Dates

Adhering to filing deadlines is critical to avoid penalties. Typically, businesses must file the DR-15N based on the state's assigned tax periods:

- Monthly Filers: Returns due by the 20th of the following month.

- Quarterly Filers: Returns due by the 20th following the end of each calendar quarter.

- Annual Filers: Returns due by January 20th of the following year.

Understanding these timelines helps ensure timely submissions and avoids unnecessary fines.

Required Documents for DR-15N Submission

Submissions must be accompanied by relevant documents to verify the accuracy of reported data. These typically include:

- Sales Records: Detailed ledgers or receipts documenting all sales transactions.

- Exemption Certificates: Proof for exempt sales claims.

- Prior Tax Returns: Past filings used for reference and verification.

Penalties for Non-Compliance

Failure to comply with the DR-15N requirements can result in significant penalties. These may include:

- Late Filing Penalties: Charges for returns filed past the due date without an approved extension.

- Underpayment Penalties: Levied against taxpayers who do not pay their full tax due by the deadline.

- Interest Charges: Accumulating interest on unpaid tax balances as an additional financial burden.

Who Typically Uses the DR-15N

The DR-15N is primarily used by businesses operating in Florida that engage in the sale of goods or services subject to state tax laws. This includes:

- Retail Businesses: Entities selling physical products directly to consumers.

- Service Providers: Companies offering taxable services under Florida law.

- Commercial Renters: Businesses organizing commercial leases requiring tax submissions.

Understanding the user base helps businesses determine if they fall within the DR-15N's applicability and prepare accordingly.