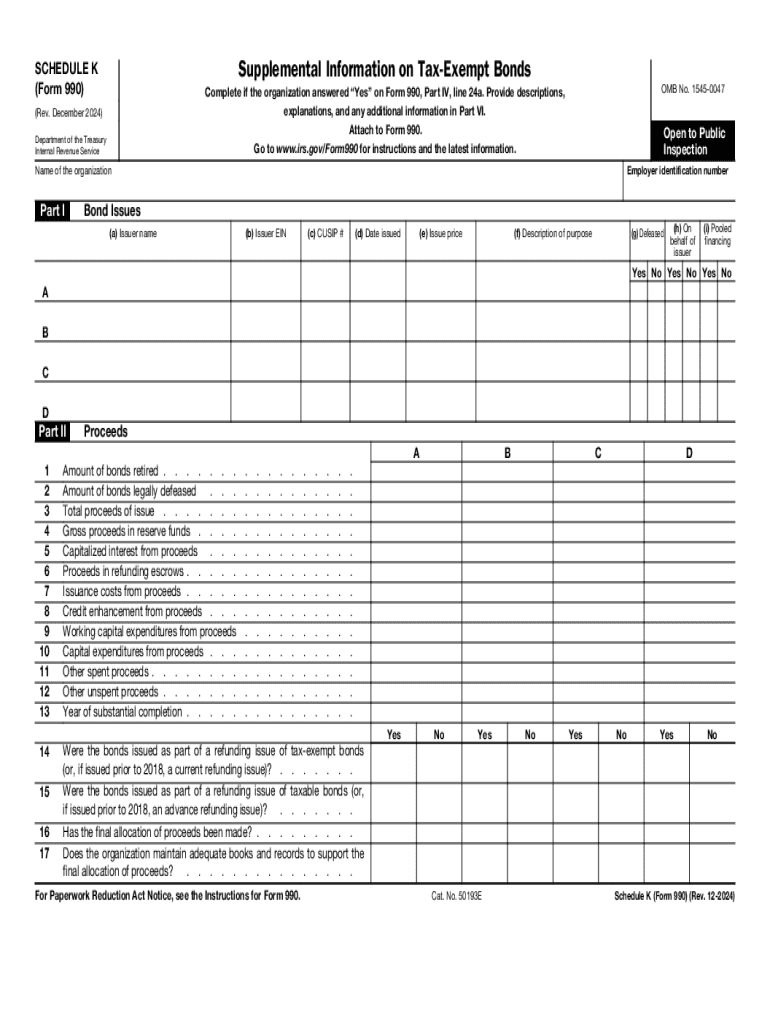

Definition and Purpose of Schedule K (Form 990)

Schedule K (Form 990) is a supplemental tax form used by organizations in the United States to report additional information regarding tax-exempt bonds. These bonds are typically used to raise funds for projects that serve the public interest, such as building schools, hospitals, or other community welfare projects. Organizations that issue tax-exempt bonds must complete Schedule K if they answer "yes" to specified questions regarding their bond activities on Form 990.

How to Use Schedule K (Form 990)

Utilizing Schedule K involves a detailed understanding of tax-exempt bonds and the specific reporting requirements. The form captures information on bond issues, the allocation and use of proceeds, private business use, and arbitrage. Organizations must ensure accurate completion to comply with IRS guidelines and avoid potential penalties. It's essential to gather all necessary documentation and evidence related to the bond activities for precise reporting.

Steps to Complete Schedule K (Form 990)

-

Gather Required Information: Collect detailed data about each bond issue, including the issuance date, the amount issued, and proceeds allocation.

-

Proceed Allocation: Document how the proceeds from the bond were utilized, ensuring they align with the intended public purposes.

-

Identify Private Business Use: Determine if any portion of the proceeds was used by private businesses, as this could affect the bond's tax-exempt status.

-

Arbitrage Compliance: Verify compliance with arbitrage rules, which restrict earning a profit from invested bond proceeds.

-

Corrective Actions: Record any steps taken to correct non-compliance or issues identified in bond usage.

-

Review and Submit: Double-check the form for completeness and accuracy before submission to the IRS.

Key Elements of Schedule K (Form 990)

- Bond Issues: Details about each bond issued, including maturity date and principal amount.

- Proceeds Allocation: Allocation of the initial proceeds received from the bond issuance.

- Private Business Use: Any involvement of private businesses in the usage of bond proceeds.

- Arbitrage Analysis: Evaluation of the bond's compliance with arbitrage earnings regulations.

- Corrective Actions: Documentation of any corrective measures taken to address issues with the use of bond proceeds.

Legal Considerations for Schedule K (Form 990)

Schedule K must be filled with accuracy to maintain an organization's compliance with federal tax laws. Misreporting or failure to report can jeopardize the tax-exempt status of the issued bonds and result in penalties. Organizations should seek legal or financial expertise to ensure that all information provided is accurate and complete. Compliance with arbitrage rules and maintaining less than ten percent private business use are also critical legal benchmarks to satisfy IRS requirements.

Filing Deadlines and Important Dates

Schedule K should be filed annually as part of the Form 990 package. The specific deadline is the 15th day of the fifth month after the end of the organization's accounting period. Extensions may be requested, offering an additional six months to file. It is vital to keep track of these deadlines to maintain compliance and avoid late fees or penalties.

Required Documents for Completion

Organizations must have a comprehensive collection of all relevant documentation to complete Schedule K:

- Copies of bond issuance documents

- Records of proceeds allocation and usage

- Compliance certificates for arbitrage requirements

- Records of any corrective actions for bond issues

- Documentation of private business involvement or usage

Form Submission Methods

Schedule K, as part of Form 990, can be submitted electronically or by mail. The IRS encourages electronic filing for its efficiency and ease of verification. However, organizations should check the latest IRS guidelines to confirm the preferred submission method.

Eligibility Criteria for Schedule K (Form 990)

Organizations that respond affirmatively to certain questions in Form 990 regarding tax-exempt bonds are required to complete Schedule K. Typically, these include nonprofit organizations, educational institutions, and public-benefiting entities that utilize bonds to fund qualifying projects. The main criterion is whether the entity has engaged in bond issuance activity within the fiscal year.

IRS Guidelines for Schedule K (Form 990)

The IRS provides a set of detailed instructions and guidelines on how to properly fill out Schedule K. These include explanations for each section and examples of correct entries. Compliance with these guidelines is essential for maintaining tax-exempt status and avoiding penalties associated with incomplete or incorrect reporting. Regular updates from the IRS necessitate that organizations stay informed on any changes to these guidelines.