Definition & Meaning

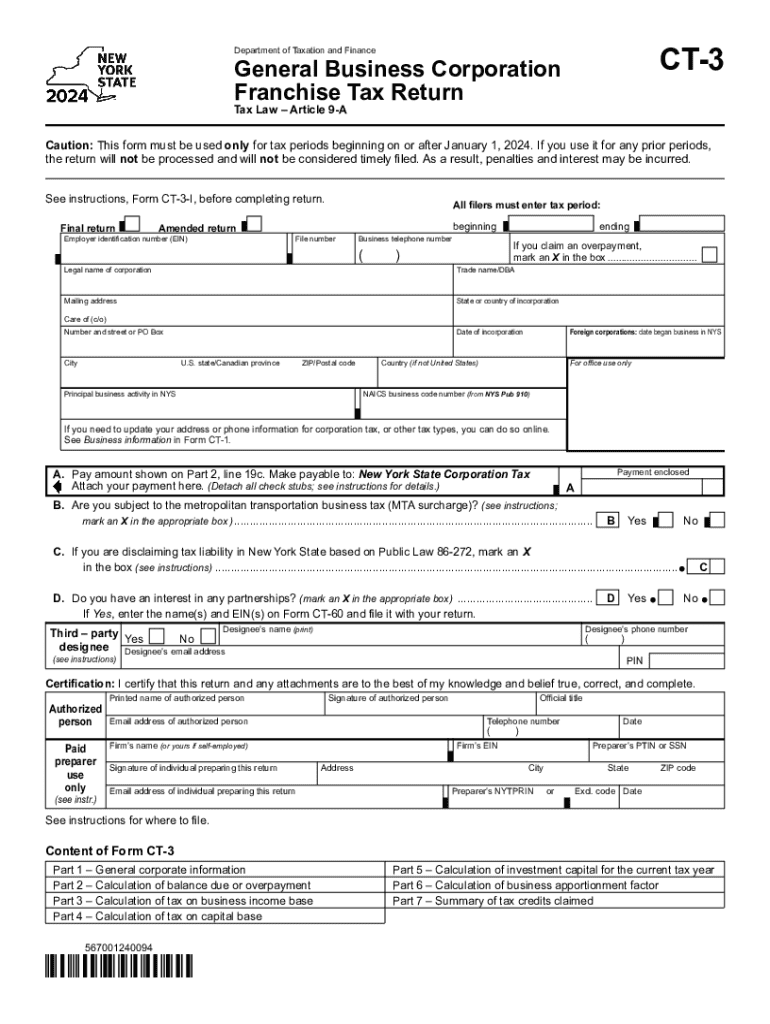

The CT-3 form, officially known as the General Business Corporation Franchise Tax Return, is required for corporations operating in New York State. This form is applicable for tax periods starting on or after January 1, 2024. It enables businesses to report their income, calculate franchise taxes, and claim any applicable credits. It is essential for ensuring compliance with New York State tax laws.

- Purpose: The form calculates the amount of franchise tax due based on a company's income, capital, and any eligible credits.

- Use Case: Corporations provide details on their income and expenditures to accurately account for their tax liabilities and potential credits.

Key Elements of the Form CT-3

The CT-3 form comprises several crucial sections to ensure full disclosure and accurate reporting by businesses.

- General Corporate Information: Includes basic details like the company's name, address, and federal employer identification number.

- Income and Capital Bases: Companies must detail their income and calculate taxes based on business capital.

- Tax Credits: This section allows for the application of applicable tax credits, requiring detailed documentation to support claims.

Steps to Complete the Form CT-3

Compilation of the CT-3 form is a detailed process requiring careful attention to ensure accuracy and compliance.

- Gather Required Documents: Start by organizing all necessary documentation, including financial statements and prior tax returns.

- Fill Out Corporate Information: Input basic corporate details accurately to set the foundation for the rest of the form.

- Calculate Income and Capital Bases: Use company financials to determine the appropriate tax base.

- Apply Relevant Tax Credits: Review applicable credits and ensure supporting documents are attached.

- Review for Accuracy: Check all entries for accuracy to avoid errors that might result in penalties.

- Submit the Form: File the form using the specified online portal, mail, or in-person options.

Important Terms Related to Form CT-3

A comprehensive understanding of the terminologies used in the CT-3 form is necessary for precise reporting.

- Franchise Tax: A tax levied on businesses for the privilege of operating within New York State.

- Capital Base: The total value of the company's assets, utilized in calculating the franchise tax.

- Tax Period: The specific fiscal year for which the tax return is being filed.

Filing Deadlines / Important Dates

Timely filing of the CT-3 form is critical to avoid potential fines and maintain compliance with state regulations.

- Deadline: Typically, the deadline aligns with the federal tax return deadline, often varying each year.

- Extensions: Corporations can request an extension if unable to meet the deadline, but must still pay estimated taxes.

Who Typically Uses Form CT-3

Understanding which entities are required to use the CT-3 form can aid in recognizing its relevance.

- Applicable Entities: All general business corporations operating in New York State must file this form.

- Exceptions: Non-profit organizations and certain small entities may have different reporting requirements.

Penalties for Non-Compliance

Failure to comply with the filing requirements of form CT-3 can result in significant penalties.

- Late Filing Penalties: Corporations face penalties, often calculated as a percentage of the unpaid taxes, for late submissions.

- Inaccurate Information Penalties: Intentional or grossly negligent errors can result in additional fines or legal repercussions.

State-Specific Rules for the Form CT-3

New York State imposes unique requirements on corporations compared to other jurisdictions, captured in the CT-3 form specifics.

- Tax Rates and Bases: This varies and adjustments might be made depending on the corporation’s income and capital.

- Mandatory Credits and Deductions: Businesses must adhere to New York-specific credits and exemptions to prevent errors in filing.

Software Compatibility (TurboTax, QuickBooks, etc.)

Accommodating digital solutions for the CT-3 form can streamline the filing process.

- Software Programs: Businesses commonly use platforms like TurboTax and QuickBooks for seamless integration and calculation of tax obligations.

- Benefits: Integration reduces errors through automated calculations and saves time by minimizing manual entries.

Digital vs. Paper Version

Choosing the right method of filing can impact the overall efficiency of the tax reporting process.

- Digital Advantage: Filing online is faster and offers immediate confirmation of receipt by the New York State Department of Taxation and Finance.

- Paper Filing: Traditional paper filing can be susceptible to delays but may be necessary for corporations preferring physical documentation.

Business Entity Types (LLC, Corp, Partnership)

Different entity types might have varied reporting needs and obligations under the CT-3 form.

- Corporations: The primary focus of the CT-3, requiring full disclosure of income and financial status.

- Others: LLCs and Partnerships might have additional requirements or alternative forms, emphasizing the necessity for consulting legal standards.

IRS Guidelines

While CT-3 is state-specific, understanding its interaction with federal IRS guidelines ensures thorough compliance.

- Alignment with Federal Filing: Maintaining consistency with federal tax filings is vital to mitigate discrepancies between the IRS and New York State taxation authorities.

- Compliance Requirements: Adhering to both state and federal guidelines ensures full compliance and supports accurately calculated tax liabilities.