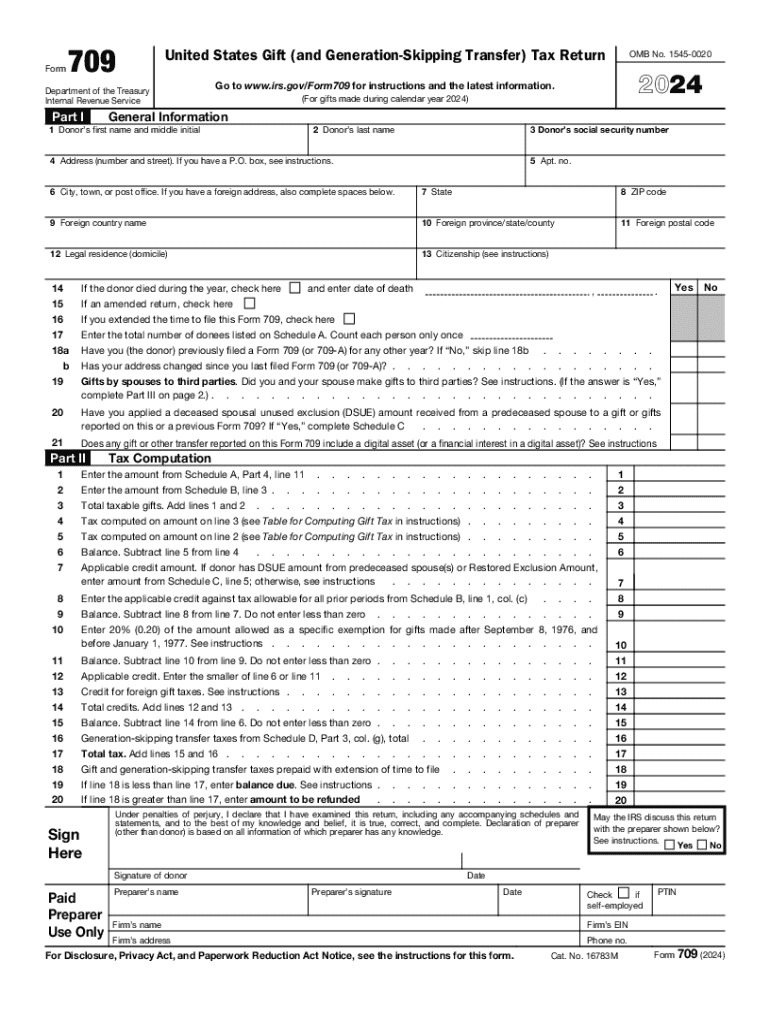

Definition and Meaning of Form 709

Form 709, officially known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is a document used by individuals in the U.S. to report taxable gifts and generation-skipping transfers. It is typically used to disclose gifts that exceed the annual exclusion limit, which is adjusted annually based on inflation. The form is essential for both individuals and legal representatives of estates to ensure compliance with federal tax regulations and avoid unnecessary tax liabilities. Additionally, it captures pertinent information regarding the donor, donee, and the nature of the gifts, ensuring that all parties abide by the legal requirements of the Internal Revenue Service (IRS).

Key Elements of Form 709

Form 709 is comprised of several key sections designed to capture detailed information about gifts and generation-skipping transfers:

- General Information: This section requires details about the donor, including personal and contact information.

- Tax Computation: Here, donors calculate the taxes owed on gifts that exceed the annual exclusion.

- Schedule A: Specifically for listing all gifts made within the tax year, it separates different types of gifts, such as those to individuals and trusts.

- Schedule B: Details prior year gifts and any applicable deductions or cumulative credits.

- Generation-Skipping Transfers: A separate schedule is dedicated to these transactions, reporting any applicable taxes due.

Steps to Complete Form 709

- Gather Information: Collect all necessary documents, including records of gifts, valuations, and prior tax returns.

- Complete General Information: Fill out the introductory section with the donor's details.

- List Gifts in Schedule A: Enter each gift along with its value and the recipient's information.

- Calculate Tax in the Tax Computation Section: Determine any taxes owed after accounting for the annual exclusion and applicable credits.

- Report Generation-Skipping Transfers: Detail these specific transfers and compute any taxes owed.

- Review and Sign: Ensure accuracy and completeness before signing and dating the form.

Filing Deadlines and Important Dates

Form 709 must be filed annually if you exceed the annual gift exclusion limit. The default deadline for submission is April 15, coinciding with the traditional U.S. income tax deadline. Extensions can be requested using IRS Form 4868, providing an additional six months, which extends the deadline to October 15. It is crucial to adhere to these timelines to avoid penalties and interest on any taxes owed.

Required Documents for Submission

To successfully complete Form 709, you will need:

- Records of all gifts given, including descriptions and valuations

- Documentation supporting the determination of fair market values

- Previous years' tax returns if applicable, to evaluate annual exclusions and cumulative credits

- Any statements or legal documents related to generation-skipping transfers

- Tax identification numbers for both donor and recipients

Legal Use and Compliance of Form 709

Using Form 709 correctly is crucial to comply with the IRS regulations concerning gift and generation-skipping transfer taxes. It ensures that donors correctly report and pay taxes on gifts exceeding the annual exclusion. Failure to file or incorrect reporting can result in penalties or additional interest charges. The form also covers legal aspects of gift splitting between spouses, requiring both parties' consent.

IRS Guidelines for Form 709

The IRS provides specific guidelines and instructions for completing Form 709, which detail:

- Annual Exclusion Amount: The allowable per-person gift amount without incurring a tax obligation.

- Lifetime Exemption: An aggregate threshold under which your gifts may avoid taxation.

- Generation-Skipping Transfer Tax: Rules to prevent the avoidance of gift taxes through skipped generational gifts.

- Spousal Gift Splits: Directions on equalizing gift amounts between married couples.

Examples and Scenarios Involving Form 709

Consider the following illustrative scenarios:

- An individual gifts $20,000 to a grandchild. The excess over the annual exclusion is reported using Form 709.

- A couple chooses to split a $60,000 financial gift for tax purposes, which requires the use of Form 709 to reflect the gift accurately.

- An estate administers a generation-skipping transfer to a beneficiary that bypasses immediate offspring, requiring detailed reporting on both the gift and GST tax implications.

Penalties for Non-Compliance with Form 709

Failing to file Form 709 when required can result in significant penalties. These include:

- Late Filing Penalities: Imposed if the form is not filed by the due date or extended date.

- Inaccurate Reporting: Severe penalties can be levied for understated gift values or intentional non-disclosure.

- Interest on Unpaid Taxes: Interest accrues on any unpaid taxes from the original due date of the return until full payment is made.

Understanding and properly completing Form 709 is vital for maintaining compliance and optimizing tax obligations related to gifts and transfers.