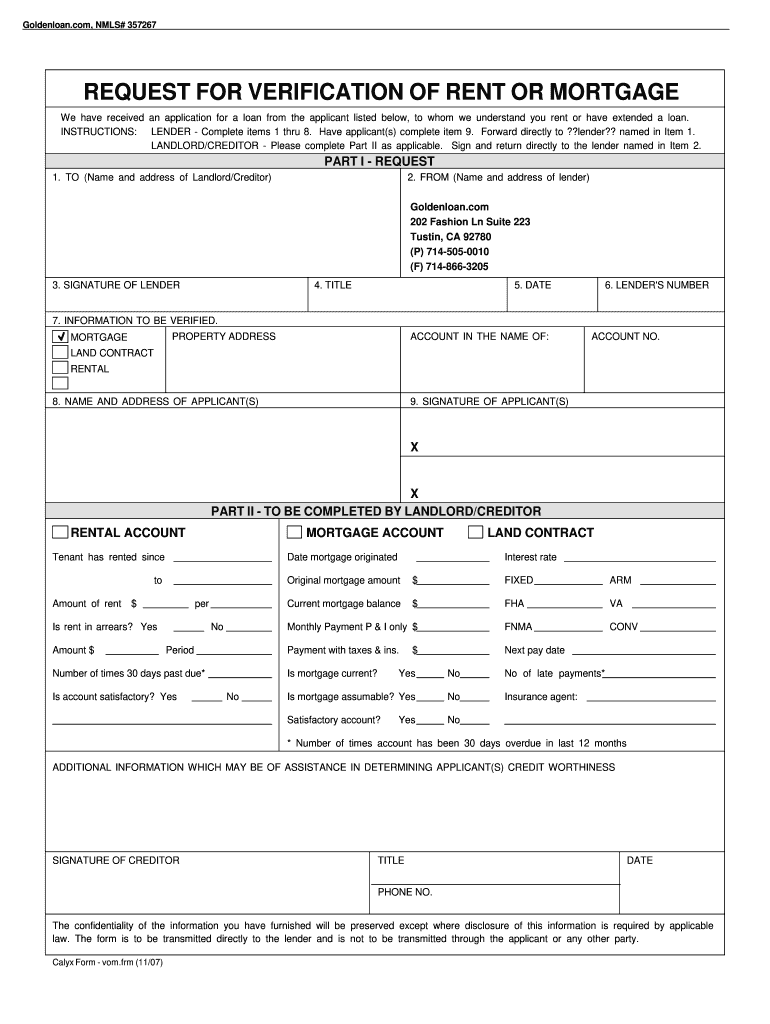

Understanding the Verification of Mortgage Form

The verification of mortgage form serves a crucial purpose in the loan application process. It is typically requested by lenders to confirm the mortgage details of an applicant. This document includes key information such as the applicant's mortgage status, payment history, and lender's contact details. Understanding how to properly utilize this form can significantly impact the overall loan approval process.

Key Components of the Verification of Mortgage Form

- Mortgage Status: This section outlines whether the applicant is current on payments, has any delinquencies, or is in foreclosure.

- Payment History: Details about the applicant's payment history, including frequency of payments made on time, late payments, and any defaults.

- Lender Information: Names and contact details for the mortgage lender or servicer, which enables the verification process.

Each of these components is vital for lenders to assess risk and make informed lending decisions.

The Usage Process for the Verification of Mortgage Form

- Request Submission: The borrower usually requests their lender or servicer to complete the verification of mortgage form.

- Completion by Lender: The lender fills out the necessary sections, confirming the mortgage details and indicating any relevant payment history.

- Return to Borrower: Once completed, the form is returned to the borrower, who then submits it to the potential new lender as part of the loan application package.

It's critical that this process is completed accurately to avoid delays in the loan approval.

Common Scenarios for Using the Verification of Mortgage Form

- Refinancing: Applicants seeking to refinance their mortgage often need to provide a verification of mortgage form to the new lender.

- Purchasing a New Home: When transitioning to a new home, buyers may need to provide this verification to assess their financial standing.

- Loan Servicing Transitions: When a borrower’s mortgage is transferred between servicers, they might be required to provide this form to streamline verification.

Each scenario showcases the verification of mortgage form as an essential document in managing mortgage-related transactions.

Importance of Accurate Information

Providing accurate and complete information on the verification of mortgage form is crucial. Inaccuracies can result in delays, higher interest rates, or even denial of the loan application. Common mistakes to avoid include:

- Omitting payment history details.

- Providing incorrect lender contact information.

- Failing to disclose any late payments or mortgage-related issues.

Ensuring attention to detail will ensure a smoother loan approval process.

Variants and Alternatives of the Verification Form

While the verification of mortgage form commonly follows a standard format, there are other related forms used in similar contexts:

- Fannie Mae VOM Form: Specifically used for verifying mortgage details in accordance with Fannie Mae guidelines.

- Verification of Rent Form: Used to confirm rental payment history, which may also influence mortgage applications for first-time homebuyers.

Each of these forms is tailored for specific purposes and adheres to relevant lending standards.

Final Thoughts on the Verification Process

Understanding and utilizing the verification of mortgage form is a fundamental aspect of the loan application process. By being well-informed and aware of the potential implications of this document, borrowers can enhance their chances of loan approval. It is advisable for applicants to discuss the form and its contents with their lenders to ensure comprehensive completion and submission.