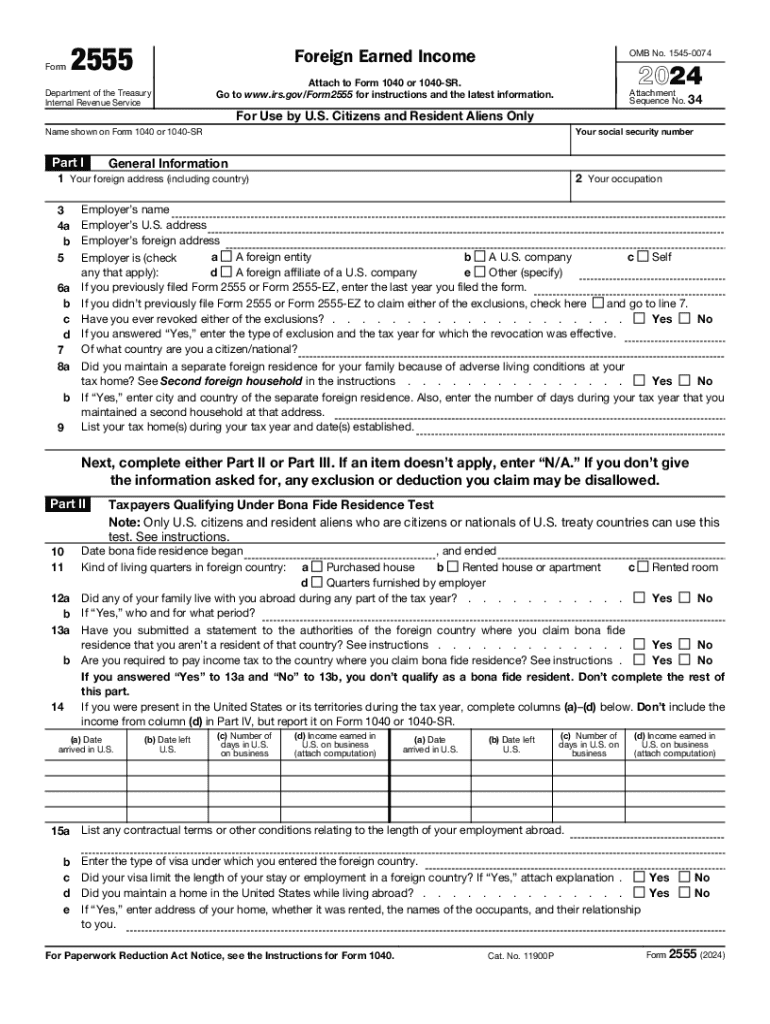

Definition and Meaning

The Foreign Earned Income Exclusion is a tax benefit that allows U.S. citizens and resident aliens to exclude a certain amount of foreign-earned income from their taxable income. This is vital for individuals who work and live abroad, helping them minimize their U.S. tax liability. Form 2555 is used to claim this exclusion, enabling eligible taxpayers to report their foreign income while adhering to U.S. tax obligations. To qualify, individuals must meet criteria under tests like the bona fide residence test or the physical presence test.

Eligibility Criteria

To be eligible for the Foreign Earned Income Exclusion, a taxpayer must satisfy specific conditions. You must be a U.S. citizen or a resident alien and have income earned in a foreign country. Additionally, the person must pass either the bona fide residence test or the physical presence test. The bona fide residence test requires an individual to be a resident of a foreign country for an uninterrupted period that includes an entire tax year. The physical presence test mandates that the taxpayer be physically present in a foreign country for at least 330 full days during any period of 12 consecutive months.

How to Use the Foreign Earned Income Exclusion

Utilizing the Foreign Earned Income Exclusion involves completing Form 2555 accurately and submitting it alongside your regular tax return. You need to calculate the total amount of income earned abroad, ensuring it fits the exclusion limits set by the IRS for the tax year. Understanding the intricacy of foreign income, housing exclusions, and housing deductions is critical. Breaking down these aspects can help optimize the exclusion, providing significant tax relief for eligible expats.

Important Terms Related to the Foreign Earned Income Exclusion

Several key terms relate to the Foreign Earned Income Exclusion that taxpayers must understand:

- Foreign Earned Income: Refers to wages and professional service fees received for work performed in a foreign country.

- Exclusion Limit: The IRS sets a cap on the amount of income that can be excluded, adjusted annually for inflation.

- Housing Exclusion and Deductions: Additional benefits that cover specific housing costs incurred during employment abroad.

Steps to Complete Form 2555

Completing Form 2555 involves a series of detailed steps to ensure eligibility and accurate reporting:

- Personal Information: Complete the sections related to your identity and tax year.

- Determining Residency: Choose between the bona fide residence test or the physical presence test.

- Calculate Exclusion and Deductions: Compute the amount of foreign earned income eligible for exclusion, considering housing cost limits.

- Attach to Tax Return: Ensure Form 2555 is attached to your annual tax return when filing.

IRS Guidelines

The IRS provides specific guidelines on the use of the Foreign Earned Income Exclusion. These guidelines dictate eligibility criteria, including detailed instructions for completing Form 2555. The IRS updates these guidelines annually to reflect changes in inflation-adjusted limits and to clarify any procedural updates. Taxpayers must stay informed about these updates to maintain compliance and maximize their exclusion benefits.

Filing Deadlines and Important Dates

Understanding filing deadlines is crucial for form submission and avoiding penalties. Typically, the due date for submitting Form 2555 is the same as the income tax return, usually April 15. However, expatriate taxpayers may qualify for an automatic two-month extension if they are outside the U.S. on the original due date. It is critical to note these dates to ensure timely filing and avoid unnecessary fines.

Penalties for Non-Compliance

Failure to comply with IRS regulations concerning the Foreign Earned Income Exclusion can result in significant penalties. These include fines for late filing or not paying tuition taxes, as well as potential disqualifications from future exclusion eligibility. Taxpayers are urged to understand the implications of non-compliance and make every effort to meet all reporting and payment deadlines.