Definition & Meaning

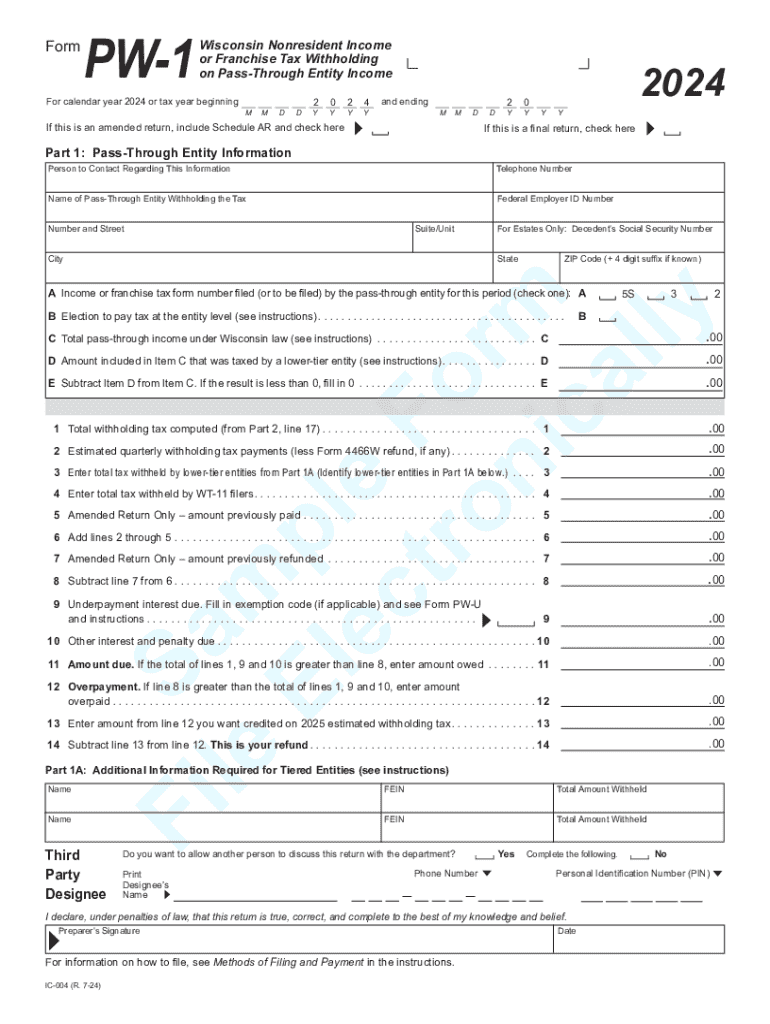

The Wisconsin Withholding Form PW-1 is a crucial document for pass-through entities in Wisconsin, aimed at ensuring proper withholding of income taxes for nonresident shareholders, partners, members, or beneficiaries. This form is essential for reporting income, withholding tax amounts, and applicable credits. It serves as a declaration for entities to comply with state laws by outlining the necessary financial details related to nonresident taxation.

Entities such as limited liability companies (LLCs), partnerships, and S corporations are typically involved in this process. The form helps maintain the integrity of the tax system by ensuring that entities with ties to Wisconsin are accountable for the income generated from within the state. Accurate reporting on this form is vital to prevent potential legal issues and ensure compliance with tax regulations.

How to Obtain the Wisconsin Withholding Form

The Wisconsin PW-1 form can be easily downloaded from the official Wisconsin Department of Revenue website. Digital availability ensures that entities can conveniently access the form whenever needed, without waiting for physical copies. Additionally, tax preparation software may support the download and completion of this form.

Once obtained, the form should be filled out carefully, considering the specific financial circumstances of the entity and its nonresident stakeholders. It is advisable to prepare any required financial documentation in advance to facilitate accurate entries on the form. If assistance is needed, entities may consult tax professionals who specialize in state-specific withholding requirements.

Steps to Complete the Wisconsin Withholding Form

-

Gather Required Information:

- Collect details on nonresident shareholders, partners, or beneficiaries.

- Prepare income statements and tax credit documentation relevant to the tax year.

-

Calculate Withholding Amounts:

- Determine the correct tax withholding based on Wisconsin's tax guidelines.

- Consider any applicable tax credits that can be claimed by the entity.

-

Complete the Form:

- Enter the entity's information, including name and federal employer identification number (FEIN).

- Provide income and tax withholding details for each nonresident participant.

-

Review Entries:

- Double-check all data for accuracy to prevent any discrepancies that may result in penalties.

- Ensure calculations are in line with the state-mandated rates and rules.

-

Submit the Form:

- Choose the appropriate submission method, either online through the Department of Revenue portal or via mail.

- Retain a copy of the completed form for the entity's records and future reference.

Legal Use of the Wisconsin Withholding Form

The legal use of the Wisconsin Withholding Form PW-1 focuses on compliance with state taxation laws for income sourced from Wisconsin but allocated to nonresidents. By filing this form, entities declare adherence to Wisconsin's income tax withholding statutes, thus fulfilling legal obligations.

The form also aids in preventing tax evasion by ensuring that taxes attributable to nonresident stakeholders are duly withheld and reported. Legal repercussions for non-compliance can include fines, interest on unpaid taxes, and increased scrutiny from tax authorities.

In addition to filing the form, entities must be aware of deadlines and maintain transparency in reporting to align with state requirements. Consulting legal experts who are well-versed in Wisconsin's tax laws can also help navigate complex situations and ensure compliance.

Key Elements of the Wisconsin Withholding Form

-

Entity Information: Accurate entry of entity details, including name, address, and FEIN, ensures proper identification by tax authorities.

-

Income Reporting: Detailed accounting of all income earned that is attributable to Wisconsin sources.

-

Withholding Computation: Inclusion of calculated withholding amounts alongside applicable tax credits, providing a comprehensive view of the tax stance.

-

Participant Details: Specification of information for all nonresident shareholders or beneficiaries, highlighting their share of income and corresponding withholding.

-

Signatory Agreement: An authorized representative must sign the form, confirming the accuracy and truthfulness of the information provided.

State-Specific Rules for the Wisconsin Withholding

Wisconsin mandates specific rules for utilizing the Withholding Form PW-1, primarily targeting pass-through entities. This form bridges the gap between state tax obligations and nonresident stakeholders, ensuring that income is fairly taxed.

Entities must be cognizant of variations in withholding percentages, which may depend on factors such as entity classification or the extent of business conducted within the state. Understanding these nuances is crucial for accurate tax reporting.

Furthermore, Wisconsin's policies may differ from federal guidelines, requiring distinct computation of taxes owed and credits applicable under state law. Engaging with state tax professionals or directly consulting the Department of Revenue can aid in adhering to these distinct rules.

Penalties for Non-Compliance

Failing to file the Wisconsin Withholding Form PW-1 or submitting inaccurate information can result in significant penalties. Non-compliance can draw interest on unpaid taxes, financial penalties, and potential legal action from the state.

The severity of penalties often correlates with the degree of oversight or misrepresentation identified. To mitigate risks, entities should prioritize accurate and timely compliance with all withholding requirements and deadlines.

Understanding the detailed requirements and potential consequences can significantly reduce the likelihood of non-compliance. Seeking advice from tax compliance experts is always a recommended approach to navigate these challenges effectively.

Form Submission Methods (Online / Mail / In-Person)

Entities can submit the Wisconsin Withholding Form PW-1 through several methods, enhancing flexibility and accessibility:

-

Online Submission: Via the Wisconsin Department of Revenue's e-file system, which provides an efficient and immediate way to submit forms.

-

Mail: Traditional submission option, allowing physical copies to be sent to the designated Department of Revenue address. Ensure that mailed forms are postmarked by the deadline to avoid penalties.

-

In-Person: While less common, direct submissions at Department offices may be possible for individuals requiring assistance or unable to use other methods.

Each submission method comes with its own set of guidelines to follow, ensuring completed forms reach the appropriate destination for processing. Selecting the best-suited option is crucial for timely and accurate compliance.