Important Terms Related to Rhode Island State Taxes

Understanding the terminology used in Rhode Island state taxes is crucial for retirees. Terms such as "taxable income," "adjusted gross income," and "itemized deductions" play significant roles in determining your tax liability.

- Taxable Income: The amount of income subject to taxes after accounting for deductions and exemptions.

- Adjusted Gross Income (AGI): Your total income minus specific deductions, crucial for determining your eligibility for additional tax credits.

- Itemized Deductions: Deductions for specific expenses, such as medical and dental expenses, which reduce taxable income.

Key Elements of Rhode Island State Taxes for Retirees

Retirees in Rhode Island need to be aware of specific tax elements that might affect their finances:

- Social Security Benefits: Rhode Island does not tax Social Security benefits for individuals with federal AGI below a certain threshold.

- Pension Income: Certain pension types may be partially taxable.

- Property Tax Relief: Eligible retirees may qualify for property tax relief under specific conditions.

Eligibility Criteria

Retirees should ensure that they meet the criteria for filing taxes in Rhode Island. Eligibility generally hinges on income levels, filing status, and residency status.

- Residency Status: Full-time residents must report all income, while part-time and nonresidents report only income earned within the state.

- Income Thresholds: Income above Rhode Island’s minimum threshold requires filing a tax return.

Steps to Complete Rhode Island Tax Forms

Filing your taxes involves a series of logical steps, ensuring accuracy and compliance with state laws.

- Collect Required Documents: Gather W-2s, 1099s, and any relevant documentation of income.

- Calculate Income: Use your federal return as a reference for income reporting.

- Determine Deductions: Evaluate whether standard or itemized deductions offer better benefits.

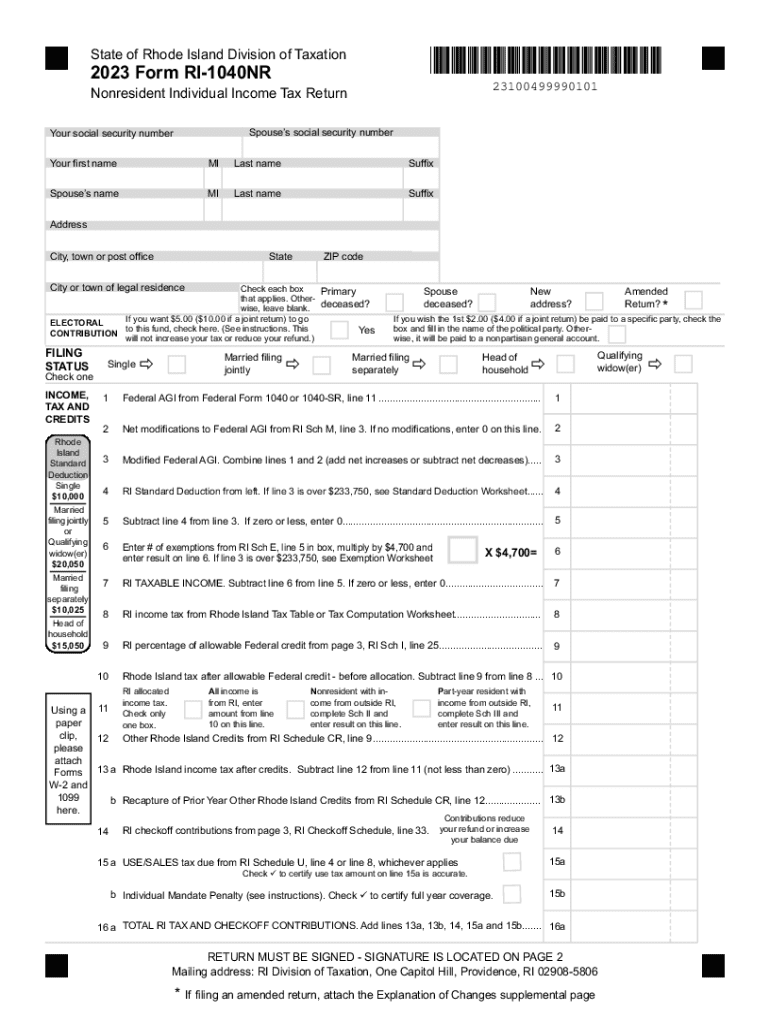

- Complete Form RI-1040: Fill out the state-specific form for nonresident or resident returns.

- Review and File: Double-check all information for accuracy before submitting.

Filing Deadlines and Important Dates

Retirees must adhere to specific deadlines to avoid penalties. Typically, tax returns are due by April 15, unless extensions are requested.

- April 15: Standard filing deadline for state taxes.

- October 15: Deadline for extensions.

Who Typically Uses Rhode Island State Taxes Forms

Rhode Island state tax forms are essential for the following groups:

- Retirees: Specifically those with diverse sources of retirement income.

- Part-Time Residents: Individuals who split time between states must file based on the income earned in Rhode Island.

Penalties for Non-Compliance

Failing to file or pay taxes on time can result in penalties and interest charges. It is important for retirees to understand:

- Late Filing Penalty: Generally a percentage of taxes owed for failing to file a return on time.

- Interest Charges: Applied on unpaid taxes until full payment is made.

Examples of Using Rhode Island State Taxes Forms

Consider a retiree, John, who receives pension and Social Security income:

- John’s Income Profile: With an AGI below the threshold, his Social Security benefits are non-taxable in Rhode Island.

- Pension Consideration: Part of his pension may be taxable, requiring careful reporting.

- Property Tax Credit: If eligible, John can reduce his effective property tax through state relief programs.

State-Specific Rules for Rhode Island Taxes

Rhode Island follows guidelines that vary from federal tax policies, which retirees should know:

- Inheritance Tax Exclusion: Check current value exclusions as these can impact estate planning.

- Credit Programs: Look into the statewide tax credit initiatives that may be available for seniors.